Dollar is extending its broad-based rally today. But other positions are somewhat changing. Sterling is now recovering as traders take profit, while awaiting an unconfirmed statement from BoE. Euro is also paring some recent losses. Meanwhile, Swiss Franc, Yen and Canadian soften in general. Australian and New Zealand Dollar are mixed.

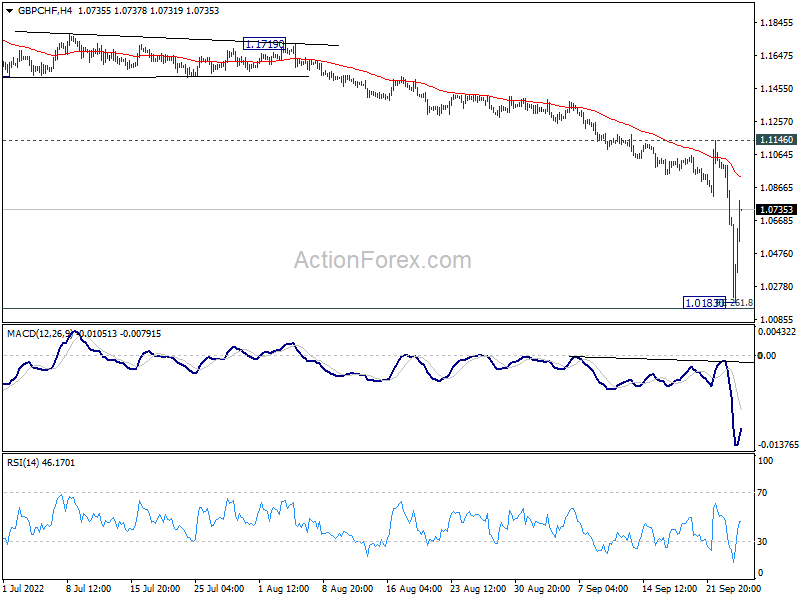

Technically, while Sterling recovers, it’s too soon to call for bottoming. The levels to watch included 1.1404 support turned resistance in GBP/USD, and 0.8720 resistance turned support in EUR/GBP. As for GBP/CHF, break of 1.1146 resistance is needed to confirm bottoming at 1.0183. Otherwise, price actions from there are viewed as part of a corrective pattern only. Down trend would resume for another low after the correction completes.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.89%. DAX is down -0.05%. CAC is down -0.11%. Germany 10-year yield if up 0.059 at 2.084. Earlier in Asia, Nikkei dropped -2.66%. Hong Kong HSI dropped -0.44%. China Shanghai SSE dropped -1.20%. Singapore Strait Times dropped -1.40%. Japan 10-year JGB yield rose 0.0082 to 0.253.

ECB Lagarde expects to raise interest rates further over next several meetings

In the hearing of a European Parliament committee, ECB President Christine Lagarde said, “most measures of longer-term inflation expectations currently stand at around two per cent. However, signs of recent above-target revisions to some indicators warrant continued monitoring.”

“The risks to the inflation outlook are primarily on the upside, mainly reflecting the possibility of further major disruptions in energy supplies,” she said. “While these risk factors are the same for growth, their effect would be the opposite: they would increase inflation but reduce growth.”

“We expect to raise interest rates further over the next several meetings to dampen demand and guard against the risk of a persistent upward shift in inflation expectations… Our future policy rate decisions will continue to be data-dependent and follow a meeting-by-meeting approach,” she said.

ECB de Guindos sees significant slowdown in Q3 and Q4

ECB Vice President Luis de Guindos said in a conference today, “we are seeing that in the third and fourth quarters there is a significant slowdown and we may find ourselves with growth rates close to zero.” He also noted that inflation in becoming increasingly broad and further rate hike will depend on incoming data.

Separately, Governing Council member Boris Vujcic said this months’ 75bps hike was “the right way to go”. “Inflation, if it’s persistently strong, has to be the clearly dominant goal,” he added. “Paying much attention to lower growth now, at the expense of fighting inflation, is often luring. But letting inflation become entrenched always has a higher cost than a temporary decline in GDP.”

Germany Ifo dropped to 84.3, slipping into recession

Germany Ifo Business Climate dropped from 88.6 to 84.3 in September, below expectation of 87.1. That’s the lowest level since May 2020. Current Assessment index dropped form 97.5 to 94.5, below expectation of 96.0. Expectations index dropped from 80.3 to 75.2, below expectation of 78.6.

Ifo said: “Companies assessed their current business as clearly worse. Pessimism regarding the coming months has grown decidedly; in retail, expectations have fallen to a record low. The German economy is slipping into recession.”

By sector, manufacturing dropped from -6.8 to -14.2. Services dropped from 1.4 to -8.9. Trade dropped from -25.8 to -32.3. Construction dropped from -14.8 to -21.6.

BoJ Kuroda: It’s highly likely for economic recovery to continue

BoJ Governor Haruhiko Kuroda said today that rapid currency moves were undesirable as they would have a negative impact on the economy. He added that intervention to address exchange volatility was the appropriate move.

Also, he pledged in a speech that BoJ will “continue with monetary easing so as to firmly support Japan’s economy from wage increases.”

Kuroda also noted, it’s “highly likely” for the economy to continue recovering following three factors. The first is improvement in exports, production, and business fixed investment. The second factor is solid private consumption. he third factor is that, with the government relaxing entry restrictions, inbound tourism demand is expected to recover. But he also pointed out risks from COVID-19, and developments in overseas economic activity and prices.

Japan FM Suzuki: Will take action against speculations on Yen if needed

Japanese Finance Minister Shunichi Suzuki reiterated that the government is “strongly concerned” about one-sided, rapid yen moves.

“We took appropriate action against excessive volatility driven by speculators. The intervention has had a certain effect,” he said, referring to last week’s intervention to support Yen. “There is no change in our stance that we will take (further) action if needed.”

“Governor Kuroda expressed Thursday in his remarks his strong concerns about the rapid depreciation of the yen. We have a shared view on this with the BOJ,” Suzuki added.

Former top currency diplomat Naoyuki Shinohara, however, said, “it’s unlikely Japan will continue intervening to defend a certain line, such as 145 yen to the dollar… It’s impossible to reverse the market’s broad trend with intervention alone.” Shinohara oversaw Japan’s currency policy during the global financial crisis in 2008.

Japan PMI manufacturing dipped to 51.0, services rose to 51.9

Japan PMI Manufacturing dropped slightly from 51.5 to 51.0 in September, below expectation of 51.1. That’s the lowest reading since January 2021. Manufacturing Output Index dropped from 49.2 to 48.9. PMI Services, on the other hand, rose from 49.5 to 51.9. PMI Composite rose from 49.4 to 50.9.

Joe Hayes, Senior Economist at S&P Global Market Intelligence, said: “Business are reporting concerns around the economic outlook amid steep cost pressures and the rising likelihood of a global economic downturn. The remarkable weakness we’ve seen in the year-to-date in the yen continues to push up price pressures, with companies struggling to fully pass on these higher costs burdens to clients. Subsequently business confidence slumped to a 13-month low”.

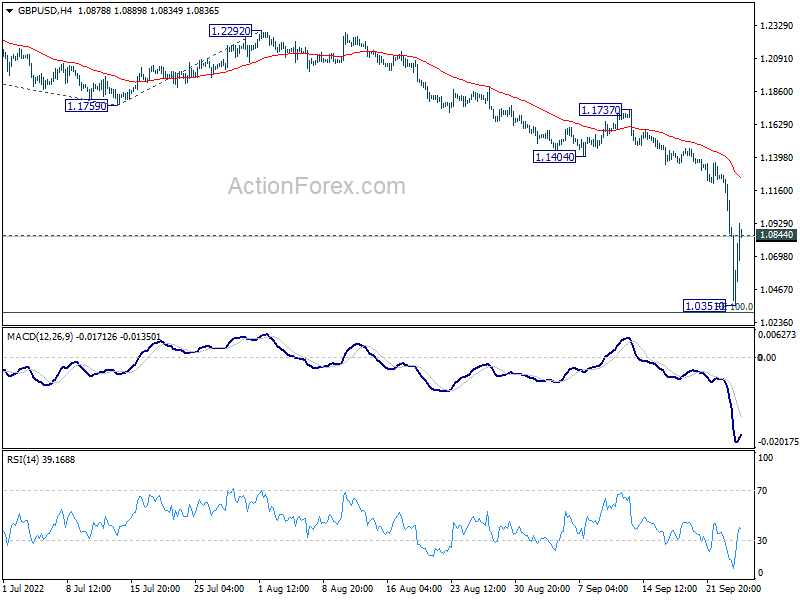

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0706; (P) 1.0990; (R1) 1.1140; More…

Break of 1.0844 minor resistance suggests that a temporary low is formed at 1.0351, ahead of 100% projection of 1.3748 to 1.1759 from 1.2292 at 1.0303. Intraday bias in GBP/USD is turned neutral for some consolidations. But risk will stay on the downside as long as 1.1404 support turned resistance holds. Sustained break of 1.0303 will pave the way to parity.

{kind=link}

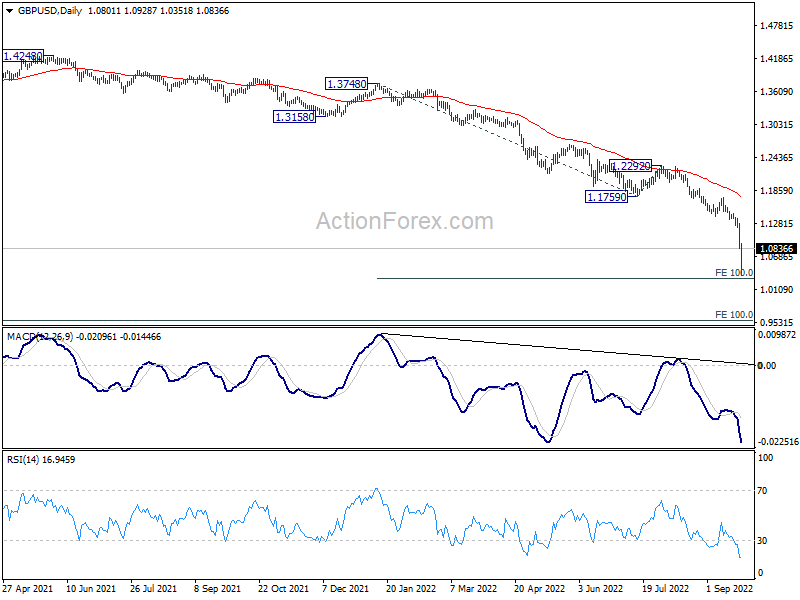

In the bigger picture, fall from 1.4248 (2018 high) is resuming long term down trend from 2.1161 (2007 high). Next target is 100% projection of 2.1161 to 1.3503 from 1.7190 at 0.9532. There is no scope of a medium term rebound as long as 1.1759 support turned resistance holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Sep P | 51 | 51.1 | 51.5 | |

| 08:00 | EUR | Germany IFO Business Climate Sep | 84.3 | 87.1 | 88.5 | |

| 08:00 | EUR | Germany IFO Current Assessment Sep | 94.5 | 96 | 97.5 | |

| 08:00 | EUR | Germany IFO Expectations Sep | 75.2 | 78.6 | 80.3 |