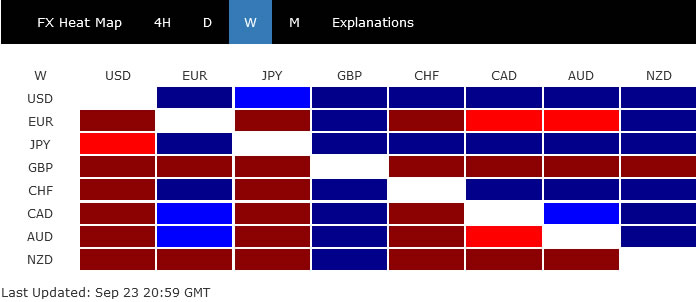

It’s such a week of surprises. The biggest one was probably the free fall in Sterling, as markets reaction to the “mini-budget” of the new UK government was overwhelmingly negative. Commodity currencies and Euro were also pressured on risk aversion.

Dollar emerged as the strongest one after hawkish Fed hike, selloff in risk assets, and surging treasury yields. Yen just eked out a second place, with Japan’s first intervention of the same kind since 1998 being unable to over turn the tide with the greenback. Swiss Franc was the third strongest, additionally supported by its rally against Euro and Sterling.

With a relatively light calendar ahead, and quarter end approaching, the markets might have a breather this week. But… never say never.

{kind=link}

GBP/USD free falling to parity after radial mini-budget

Sterling was already under some pressure after Fed’s hawkish rate hike. BoE’s decision to raise Bank Rate by 50bps was not unanimous, with three MPC members voted for a 75bps and one voted for just 25bps. But the free fall only took off after Finance Minister Kwasi Kwateng’s mini-budget, which was perceived by some as the most radical since 1972.

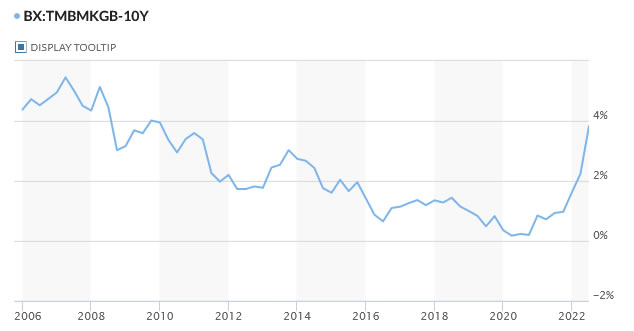

Market reactions were overwhelmingly negative to the plan. FTSE lost -1.97% on Friday and could barely defend 7000 handle. 10-year Gilt yield surged 0.3292 to 3.827, the biggest one-day jump on record since 1989, and hit the highest level since 2010. GBP/USD fell below 1.09 for the first time since 1985.

{kind=link}

Investors believed the plan would push inflation even higher and BoE would be forced to raise interest rate further to 5.50% in the currency cycle, which adds additional weight to the economy. The combined reaction suggests the lack of confidence in the government’s ability managing the ballooning debt.

While the decline in FTSE was deep, it’s not the end of the world for the UK yet. The key medium term level to defend is 38.2% retracement of 4898.79 to 7687.27 at 6622.07. As long as this level holds, any ups-and-downs, while large, are seen as part of a medium term sideway pattern only.

{kind=link}

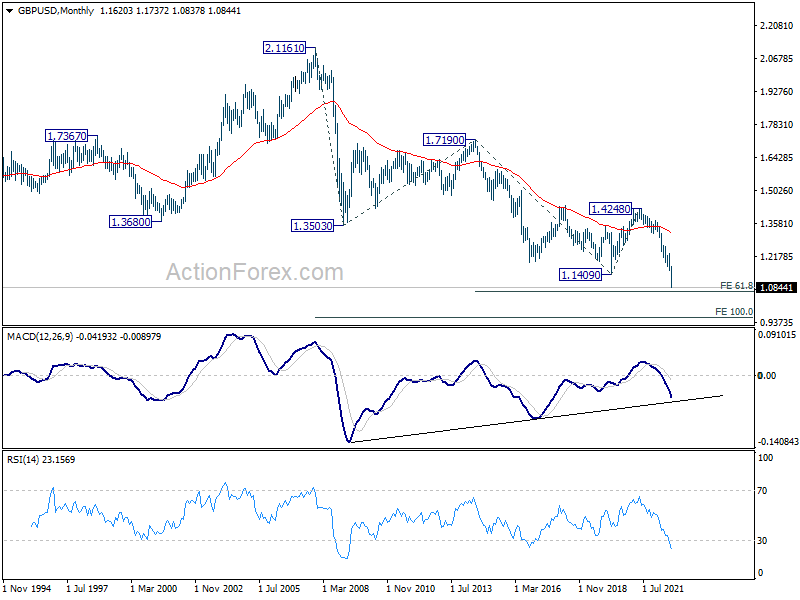

As for GBP/USD, it would hope to get some support between parity and 61.8% projection of 1.7190 (2014 high) to 1.1409 (2020 low) from 1.4248 (2021 high) at 1.0675. to stabilize, as least for the first attempt. It’s way too early to judge how deep the current down trend would extend to. But if parity is taken out firmly, the next target could be 100% projection of 2.116 to 1.3503 from 1.7190 at 0.9532.

{kind=link}

Japan intervened finally, but USD/JPY just range bound

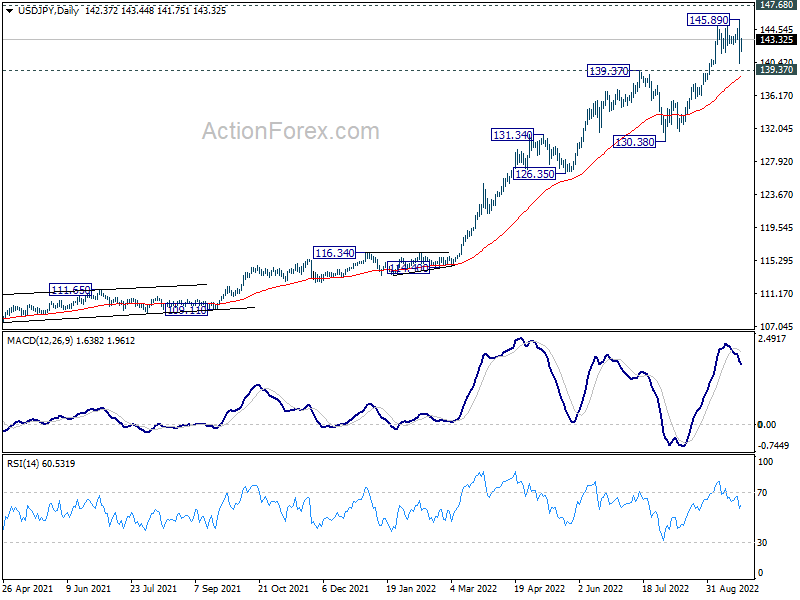

Another significant development last week was Japan’s intervention in the currency markets, the first act to support Yen since 1997-98 Asian Financial crisis. Japan did intervene in the markets in between but those actions were for slowing the currency’s advances. The move came after USD/JPY hit 24 year high and threatened to approach 1998 high at 147.68.

While Yen did rebound after intervention, there was no follow through buying against Dollar so far. The up trend in USD/JPY remains intact with 139.37 resistance turned support intact. That is, USD/JPY could still have another attempt on 147.68 to test Japan’s determination.

Firm break of 139.37 will be an indication of medium term topping. But based on current market sentiment, and policy divergence between Fed and BoJ, there is little chance of breaking next support level at 130.38 in the foreseeable future.

{kind=link}

Dollar and yields up, stocks down after FOMC

Moving on to the US, Fed raised interest rate by 75bps to 3.00-3.25% as widely expected. The bigger surprise was found in the new economic projections, which expect interest rate to hit 4.4% by the end of this year, and peak at 4.6% in 2023. But then, there is still room for further upward revision in the policy path in December’s projection if high inflation persists.

DOW break through prior low at 29653.29 to resume the medium term correction from 36952.65 high. For now, near term outlook will stay bearish as long as 31026.89 resistance holds, even in case of strong recovery. The correction could target 100% projection of 36952.65 to 26953.29 from 34281.36 at 26982.00, or even further to 61.8% retracement of 18213.65 to 36952.65 at 25371.94, before completion.

{kind=link}

{kind=link}

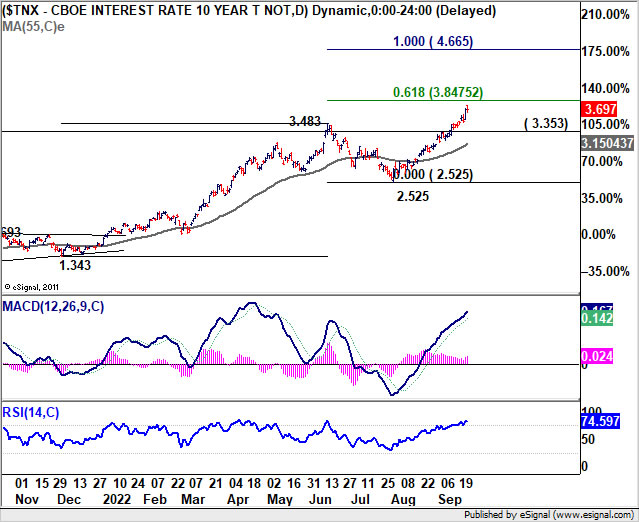

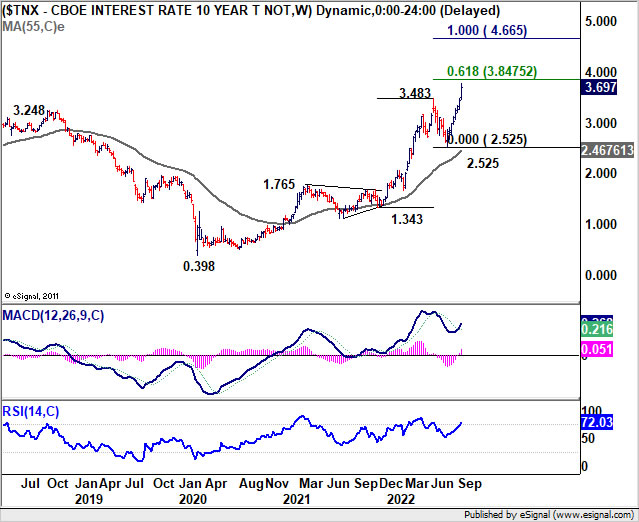

10-year yield surged through 3.483 to resume the long term up trend last week, and hit as high as 3.773. TNX is now in proximity to 61.8% projection of 1.343 to 3.483 from 2.525 at 3.847. There might be some consolidations below this projection level first. But in any case, further rally is in favor as long as 3.353 support holds. Firm break of 3.847 could prompt further up side acceleration to 100% projection at 4.665.

{kind=link}

{kind=link}

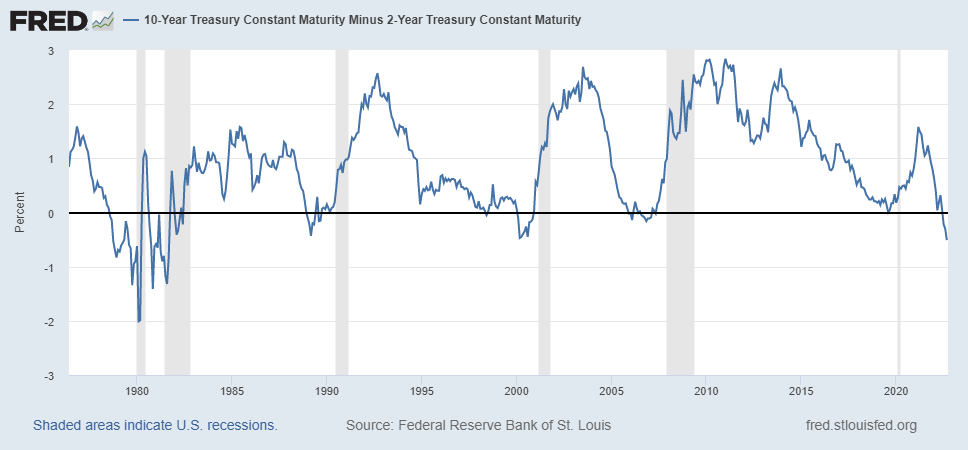

At same time, it should also be noted that 2-year yield rose 0.345 over the week to close at 4.212, hitting the highest level since 2007. Inversion of 2-yr and 10-yr yield, at -0.51, is now the deepest since 1981, surpassing -0.43 in 1989.

{kind=link}

As for Dollar index, it accelerated to to close strongly at 113.19 as up trend resumed. DXY is now pressing a medium-term channel resistance, and the two-decade channel resistance. It’s also in proximity to 61.8% projection of 94.62 to 109.29 from 104.63 at 113.69. Thus, there is prospect of further loss of upside momentum, and some consolidations.

But still, break of 109.29 resistance turned support is needed to confirm topping. Otherwise, further rally will remain in favor. Sustained break of 113.69 will pave the way to 100% projection of 119.30, which is close to 120 psychological level, and 2001 high.

{kind=link}

{kind=link}

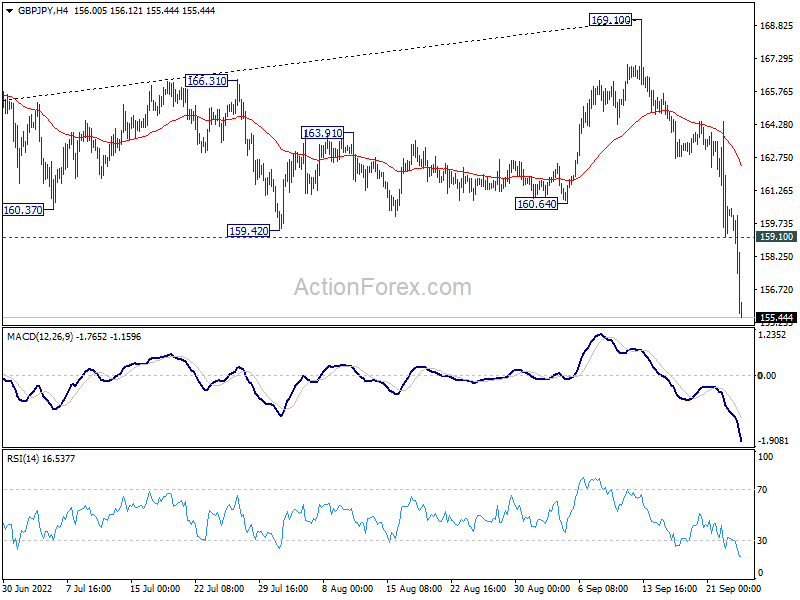

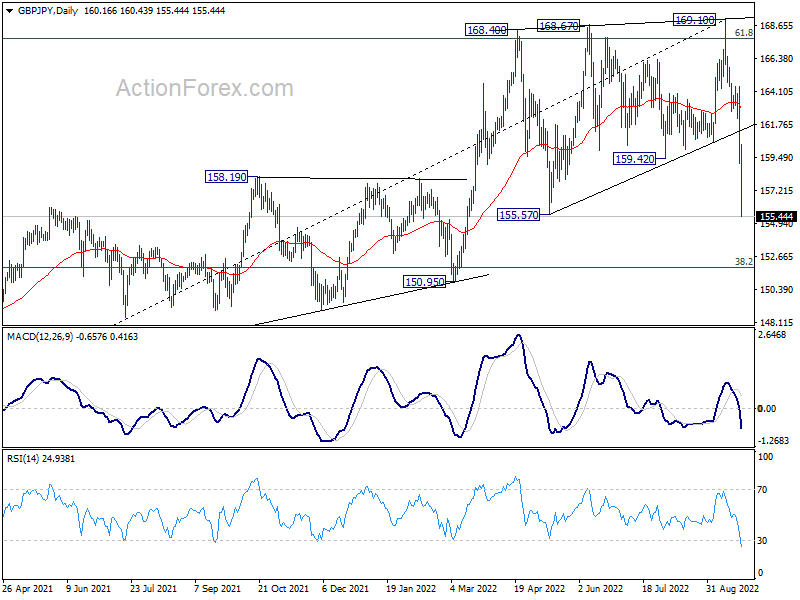

GBP/JPY Weekly Outlook

GBP/JPY’s sharp decline and break of 155.57 support suggests medium term topping at 169.10. That came after multiple rejection by long term fibonacci level at 167.93. Initial bias remains on the downside this week for 150.95 support next. On the upside, above 159.10 minor resistance will turn intraday bias neutral and bring consolidations, before staging another fall.

{kind=link}

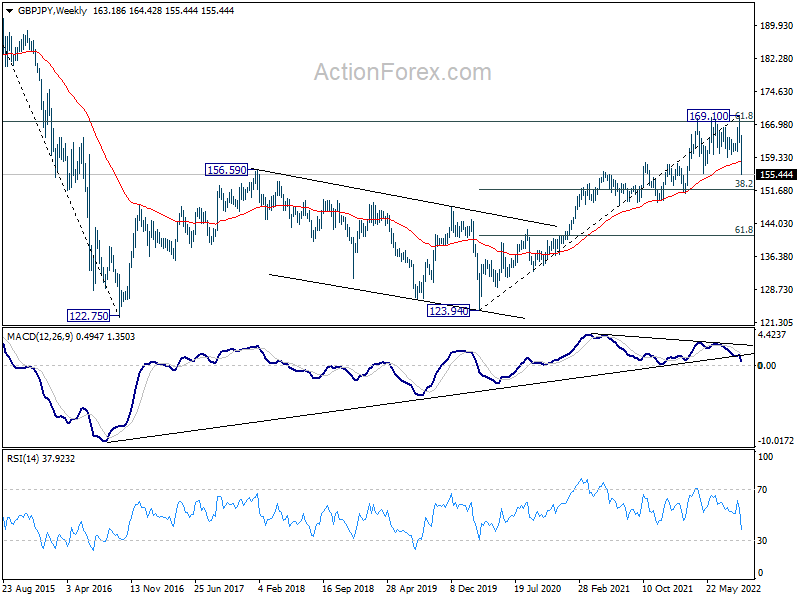

In the bigger picture, rejection by 61.8% retracement of 195.86 (2015 high) to 122.75 (2016 low) at 167.93 suggests that rise from 123.94 (2020 low) has completed. Deeper fall would be seen to 38.2% retracement of 123.94 to 169.10 at 151.84. Some support could be seen there to bring rebound. But risk will now stay on the downside as long as 169.10 resistance holds. Sustained trading below 151.84 will target 61.8% retracement at 141.19.

{kind=link}

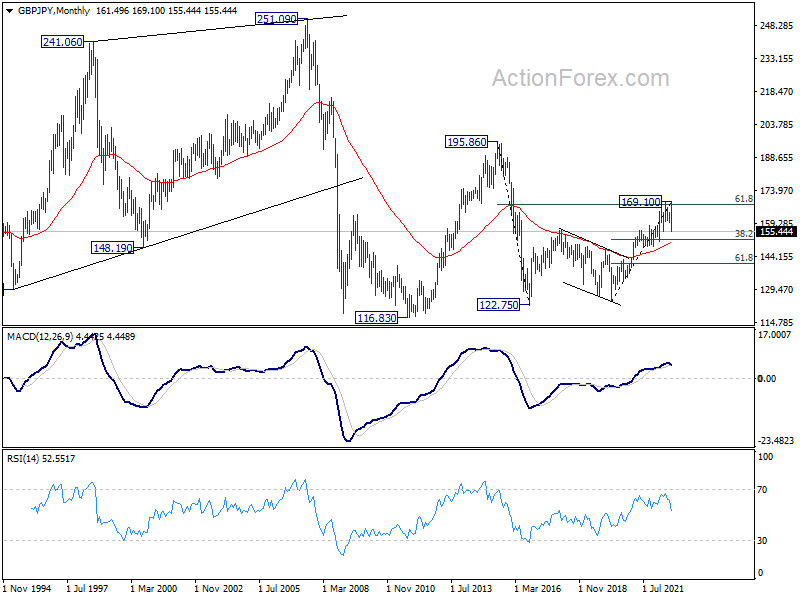

In the longer term picture, as long as 55 month EMA (now at 150.40) holds, rise from 122.75 could still extend higher at a later stage. However, sustained break of 55 month EMA will ague that whole rise has completed, and open up deeper fall back to 116.83/122.75 support zone.

{kind=link}

{kind=link}