Dollar broke out to the upside overnight following hawkish Fed hike. At the same time, it’s closely trailed by Swiss Franc for now, on geopolitical risks. Risk aversion is also keeping Yen afloat in crosses, despite strong rally in treasury yields. For now, Kiwi is the worst performer for the performer among the weak commodity currencies. But Euro is not too far behind as Ukraine war could drag on further with Russian’s military mobilization.

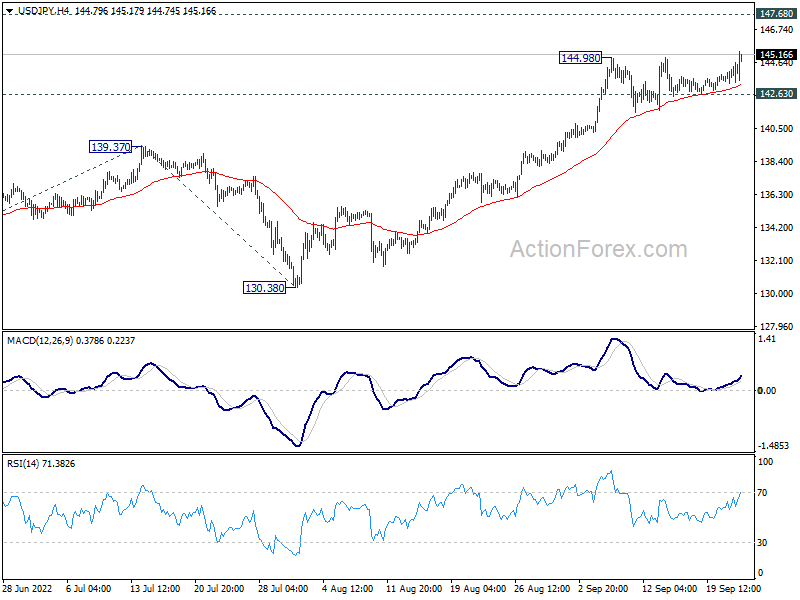

Technically, USD/JPY is resuming recent up trend with a break of 144.98 resistance today, follow BoJ rate decision. Near term outlook will stays bullish as long as 142.63 support holds. Next target is 1998 high at 147.68. Momentum towards the level, and reactions from there are worth a watch, on hint on whether Japan is ready for taking actual actions on intervention.

{kind=link}

In Asia, Nikkei closed down -0.53%. Hong Kong HSI is down -1.93%. China Shanghai SSE is down -0.34%. Singapore Strait Times is down -0.25%. Japan 10-year JGB yield is down notably by -0.0256 at 0.236. Overnight, DOW dropped -1.70%. S&P 500 dropped -1.71%. NASDAQ dropped -1.79%. 10-year yield rose dropped -0.061 to 3.510.

Fed hikes 75bps, rate to reach 4.4% by year end

Fed raised interest rate by 75bps to 3.00-3.25% as widely expected, by unanimous vote. In the accompanying statement, Fed said job gains have been “robust” with unemployment rate “remained low”. Inflation remains “elevated”. FOMC would be ” prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals.”

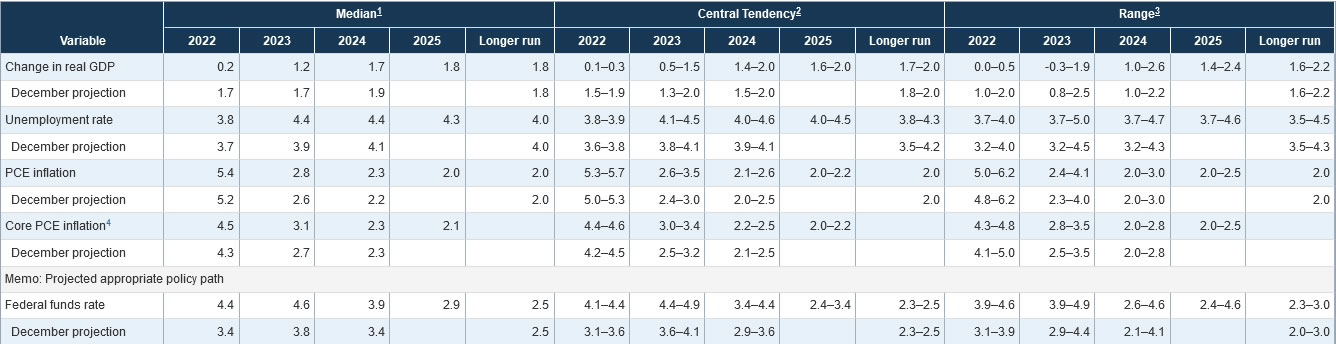

In the new economic projections, Fed projects (median) interest rates to reach 4.4% in 2022, 4.6% in 2023, before falling back to 3.9% in 2024, and then 2.9% in 2025. GDP growth is projected to be at 0.2% in 2022, 1.2% in 2023, 1.7% in 2024, and then 1.8% in 2025. Unemployment rate is projected to be at 3.8% in 2022, 4.4% in 2023, 4.4% in 2024, and then 4.3% in 2025. Core PCE inflation is projected to be at 4.5% in 2022, 3.1% in 2023, 2.3% in 2024, and then 2.1% in 2025.

{kind=link}

More on FOMC:

DOW to break 30k soon on hawkish Fed

US stocks tumbled broadly after Fed raised interest rate by 75bps overnight, and indicated that rate could reach 4.4% by year end. Chair Jerome Powell reiterated that pledge that “the FOMC is strongly resolved to bring inflation down to 2%, and we will keep at it until the job is done.” Meanwhile, against members’ expectations, “we have seen some supply side healing but inflation has not really come down,” he noted.

DOW’s -1.70% decline indicates that fall from 34281.36 is extending and break of 30k handle would be seen soon. Such fall is seen as part of the whole medium term corrective pattern from 36952.65. Near term outlook will stay bearish as long as 31026.89 resistance holds. Next target is a retest of 29653.29 low. Firm break there will target 100% projection of 36952.65 to 29653.29 from 34281.36 at 26982.00. There’s where the correction would probably end.

{kind=link}

{kind=link}

BoJ stands part, interest rate to remain at present or lower levels

BoJ kept monetary policy unchanged as widely expected. Under the yield curve control framework, short-term policy interest rate is held at -0.10%. BoJ will continue to purchase Japanese government bonds, without setting an upper limit, to keep 10-year JGB yield at around 0%. Also, BoJ will offer to purchase 10-year JGBs at 0.25% every business day through fixed -rate purchase operations, to cap the upside. These decisions were made by unanimous vote.

BoJ also pledge to continue with Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control to achieve 2% price target, “as long as it is necessary for maintaining that target in a stable manner”. The bank will not hesitate to take additional easing measures if necessary”. It expects short- and long-term policy interest rates to “remain at their present or lower levels”.

SNB and BoE next, GBP/CHF accelerating down

SNB and BoE rate decisions are the remaining focuses of the day. SNB is widely expected to rise interest rate by 75bps to 0.50%, back in positive region. There are some speculations of a larger hike, but it’s unlikely. The central would also repeat that appreciation of the Swiss Franc is welcome for now, as it helps curb imported inflation.

Meanwhile, BoE is expected to deliver another 50bps hike to 2.25%. The UK economy is stuck between a rock and a hard place. While inflation appeared to be slowing, “slightly”, it remained close to multi-decade high. On the other hand, weakness has been seen in spending while the economy is already in recession. The voting of today’s decision could contain some surprises.

Some previews on SNB and BoE:

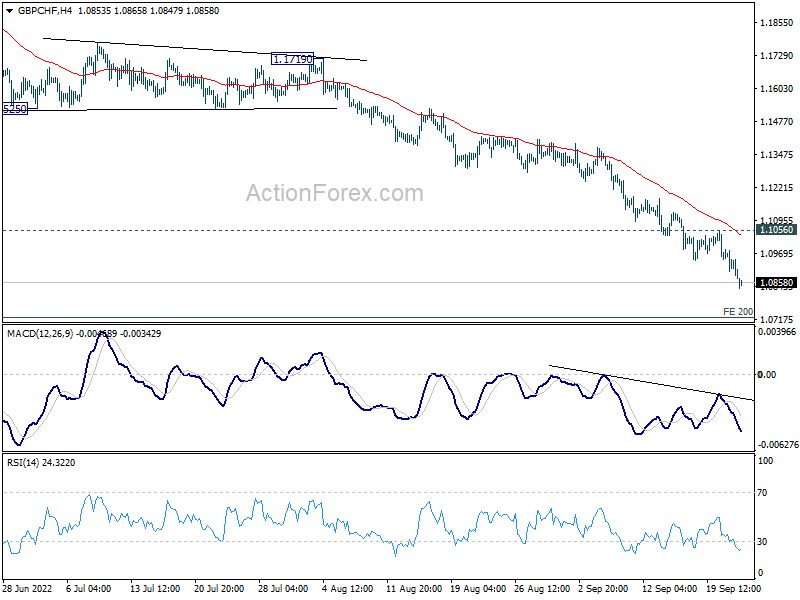

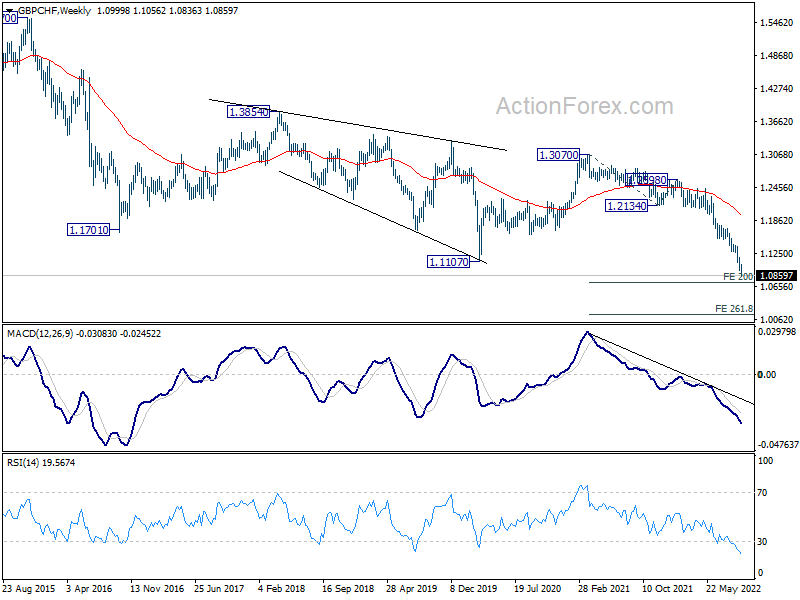

GBP/CHF broke through pandemic low at 1.1107 earlier this month, and the down trend is still in acceleration mode. Near term outlook will stay bearish as long as 1.1056 resistance holds. Next target is 200% projection of 1.3070 to 1.2134 from 1.2598 at 1.0726.

There is risk of further downside acceleration, either on dovish BoE or deterioration in geopolitical risks. In that case, break of 1.0726 could pave the way to 1.0148.

{kind=link}

{kind=link}

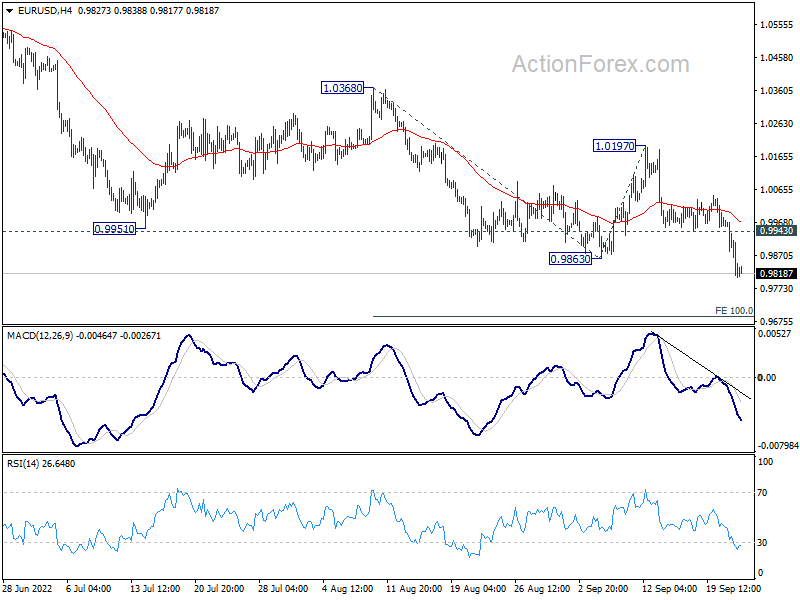

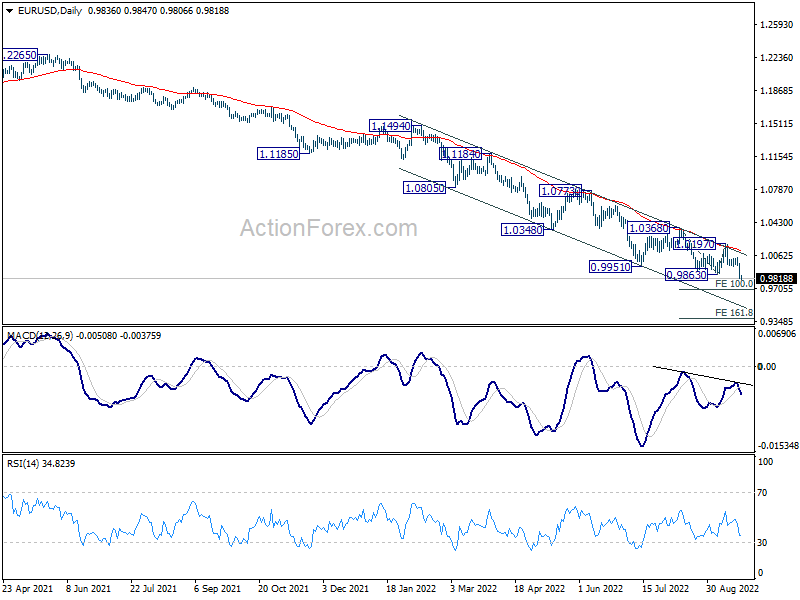

EUR/USD Daily Outlook

Daily Pivots: (S1) 0.9774; (P) 0.9876; (R1) 0.9940; More…

EUR/USD’s break of 0.9863 support confirms down trend resumption. Intraday bias is back on the downside for 100% projection of 1.0368 to 0.9863 from 1.0197 at 0.9692. Firm break there could prompt downside acceleration and target 161.8% projection at 0.9380. On the upside, above 0.9943 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 1.0197 resistance holds, in case of recovery.

{kind=link}

In the bigger picture, down trend from 1.6039 (2008 high) is still in progress. Next target is 100% projection of 1.3993 to 1.0339 from 1.2348 at 0.8694. In any case, break of 1.0197 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish even with strong rebound.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Aug | -2447M | -500M | -1092M | |

| 03:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 07:30 | CHF | SNB Interest Rate Decision | 0.50% | -0.25% | ||

| 08:00 | ECB | Eurozone Economic Bulletin | ||||

| 11:00 | GBP | BoE Interest Rate Decision | 2.25% | 1.75% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | 9–0–0 | 9–0–0 | ||

| 12:30 | USD | Initial Jobless Claims (Sep 16) | 220K | 213K | ||

| 12:30 | USD | Current Account (USD) Q2 | -258B | -291B | ||

| 12:30 | CAD | New Housing Price Index M/M Aug | 0.10% | 0.10% | ||

| 14:00 | EUR | Eurozone Consumer Confidence Sep P | -26 | -24.9 | ||

| 14:30 | USD | Natural Gas Storage | 97B | 77B |