Canadian Dollar falls broadly in early US session after weaker than expected inflation reading. Yet, it’s still undecided on which currency is worst. Dollar is current in the driving seat, as lifted by extended rally in treasury yield. 10-year yield is trading up above 3.5 handle for the first time in more than a decade. Swiss Franc and Yen are steady on risk aversion. But Sterling is more resilient with help from buying against Euro.

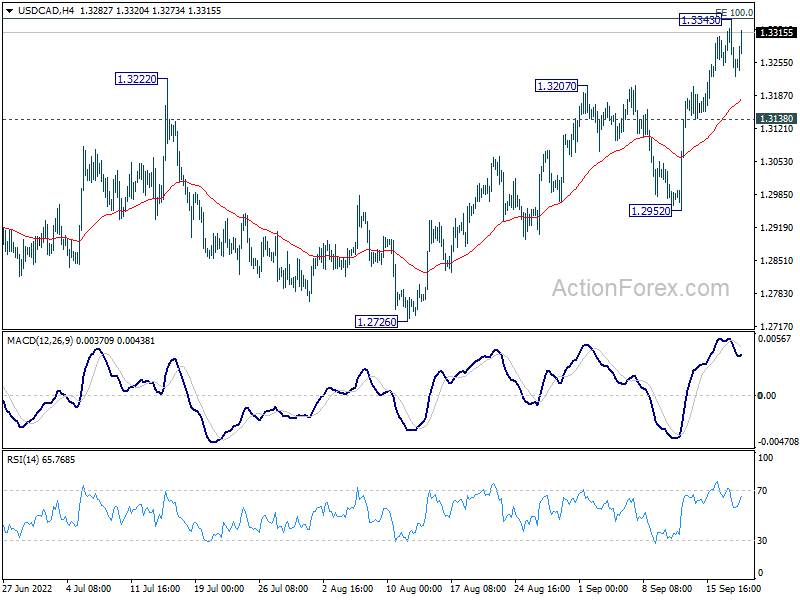

Technically, immediate focus in on 1.3343 temporary top in USD/CAD. Firm break there will resume larger up trend to medium term fibonacci level at 1.3650. That would be a leading signal of more rally in Dollar elsewhere.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.37%. DAX is down -0.88%. CAC is down -1.14%. Germany 10-year yield is up 0.115 at 1.919. Earlier in Asia, Nikkei rose 0.44%. Hong Kong rose 1.16%. China Shanghai SSE rose 0.22%. Singapore Strait Times rose 0.33%. Japan 10-year JGB yield rose 0.0028 to 0.260.

Canada CPI slowed to 7% yoy in Aug

Canada CPI dropped -0.3% mom in August, below expectation of -0.1% mom. That’s the largest monthly decline since early months of the pandemic.

For the 12-month period, CPI slowed from 7.6% yoy to 7.0% yoy, below expectation of 7.3% yoy. That’s also the second consecutive slowdown in the year-over-year rate, largely driven by lower gasoline prices. CPI excluding gasoline slowed from 6.6% yoy to 6.3% yoy, first deceleration since June 2021.

CPI common rose from 5.5% yoy to 5.7% yoy, above expectation of 5.6% yoy. CPI median dropped from 5.0% yoy to 4.8% yoy, below expectation of 5.1% yoy. CPI trimmed dropped from 5.4% yoy to 5.2% yoy, below expectation of 5.5% yoy.

From the US, building permits dropped to 1.52m annualized rate in August, below expectation of 1.62m. Housing starts rose to 1.58m, above expectation of 1.46m.

SECO downgrades Swiss GDP forecasts, upgrades CPI

SECO downgraded Swiss GDP growth forecasts for 2022 from 2.6% to 2.0%. For 2023, GDP growth projection was also lowered from 1.9% to 1.1%. CPI forecasts for 2022 was raised from 2.5% to 3.0%, and for 2023 up from 1.4% to 2.3%.

It said, “after a positive first half of the year 2022, the Swiss economy now faces a deteriorating outlook. A tense energy situation and sharp price increases are weighing on economic prospects, especially in Europe.”

It also warned of risks from “serious gas or electricity shortages” in Europe, and “large-scale production stoppages and a marked downturn”. Such a negative scenario would likely lead to “high domestic price pressures” and “downward trend in the economy economy. With rising interest rates, ” risks associated with the surge in global debt are intensifying.

Japan CPI core rose to 3% yoy in Aug, highest in 31 years

Japan CPI accelerated from 2.6% yoy to 3.0% yoy in August, above expectation of 2.6% yoy. CPI core (ex-fresh food), rose from 2.4% yoy to 2.8% yoy, above expectation of 2.7% yoy. CPI core-core (ex-fresh food, energy), also rose from 1.2% yoy to 1.6% yoy, but missed expectation of 1.7% yoy.

CPI core, the BoJ watched reading, hit the highest level in 31 years since 1991, excluding the effect of sales tax hike. Even including the impact of sales tax, the reading was still the highest in nearly 8 years.

BoJ is widely expected to continue to stand pat, and maintain negative interest rate later this week. But there are expectations that core inflation could hit 3% later in the year, and stay above the 2% target in the near term. That might start to change BoJ’s view on prices and policy at a later stage.

RBA minutes: Slower tightening comes with higher rates

Minutes of RBA’s September 6 meeting revealed that there were discussions on whether to hike by 25bps or 50bps. But, “given the importance of returning inflation to target, the potential damage to the economy from persistent high inflation and the still relatively low level of the cash rate, the Board decided to increase the cash rate by a further 50 basis points.”

RBA reiterated that there will be further interest rate hikes “over the months ahead”, but it’s it “not on a pre-set path”. The full effects of higher interest rates were “yet to be felt” on mortgages, activity and inflation.

The board was “mindful” that the path to bring inflation back to target “needed to account for the risks to growth and employment. RBA is seeking to return inflation to target “while keeping the economy on an even keel”.

Size of timing of future rate hikes will be “guided by the incoming data” and outlook for inflation and job market, and risks. “All else equal, members saw the case for a slower pace of increase in interest rates as becoming stronger as the level of the cash rate rises”.

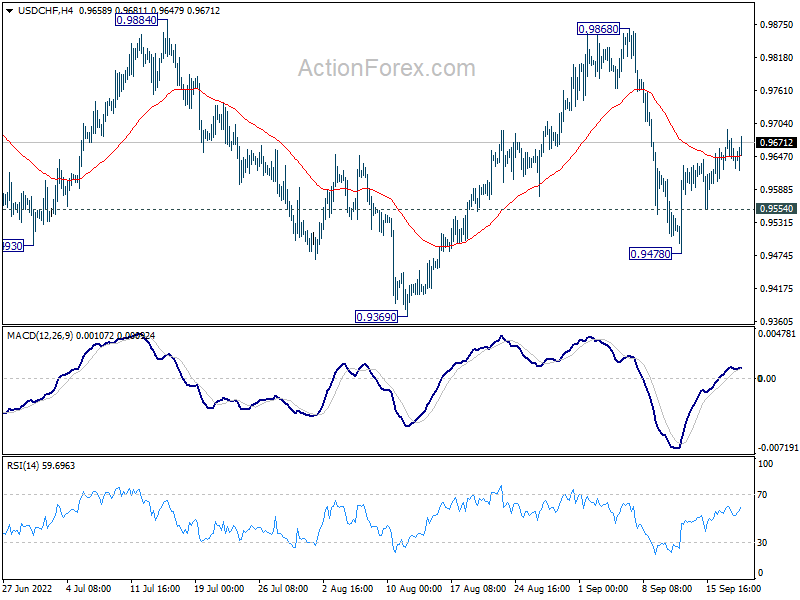

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9615; (P) 0.9655; (R1) 0.9684; More

No change in USD/CHF’s outlook and intraday bias stays mildly on the upside. Rise from 0.9478 would target 0.9868 resistance. Break there will argue that larger up trend is ready to resume through 1.0063. Overall, the corrective pattern from 1.0063 high could still extend. Below 0.9554 minor support will turn bias back to the downside for 0.9478 and below.

{kind=link}

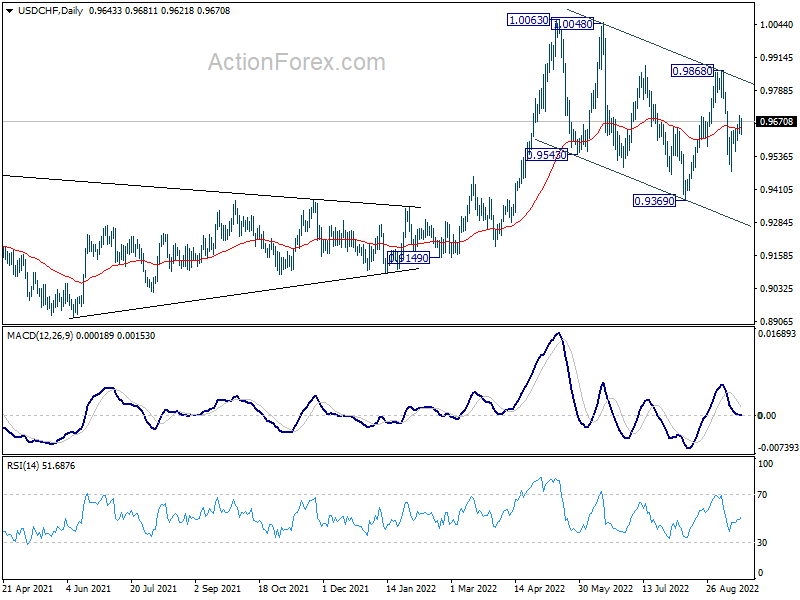

In the bigger picture, current development suggests that up trend from 0.8756 (2021 low) is still in progress. Sustained break of 1.0063 will target 100% projection of 0.9149 to 1.0063 from 0.9369 at 1.0283, and then 1.0342 (2016 high). For now, this will remain the favored case as long as 0.9369 support holds, even in case of deep pull back.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Aug | 2.80% | 2.70% | 2.40% | |

| 01:30 | AUD | RBA Minutes | ||||

| 06:00 | EUR | Germany PPI M/M Aug | 7.90% | 1.50% | 5.30% | |

| 06:00 | EUR | Germany PPI Y/Y Aug | 45.80% | 37.50% | 37.20% | |

| 07:00 | CHF | SECO Economic Forecasts | ||||

| 08:00 | EUR | Current Account (EUR) Jul | -19.9B | 5.3B | 4.2B | |

| 12:30 | USD | Building Permits Aug | 1.52M | 1.62M | 1.69M | |

| 12:30 | USD | Housing Starts Aug | 1.575M | 1.46M | 1.45M | |

| 12:30 | CAD | CPI M/M Aug | -0.30% | -0.10% | 0.10% | |

| 12:30 | CAD | CPI Y/Y Aug | 7.00% | 7.30% | 7.60% | |

| 12:30 | CAD | CPI Common Y/Y Aug | 5.70% | 5.60% | 5.50% | |

| 12:30 | CAD | CPI Median Y/Y Aug | 4.80% | 5.10% | 5.00% | |

| 12:30 | CAD | CPI Trimmed Y/Y Aug | 5.20% | 5.50% | 5.40% |