Overall, Dollar remains the strongest one for the week, followed by Swiss Franc and then Yen. Risk aversion support these currencies, on the expectation of another jumbo rate hike by Fed next week. Commodity currencies are the worst performers with Kiwi having an underhand. Euro and Sterling are mixed for now, with Euro having a slight advantage, but that could easily flip.

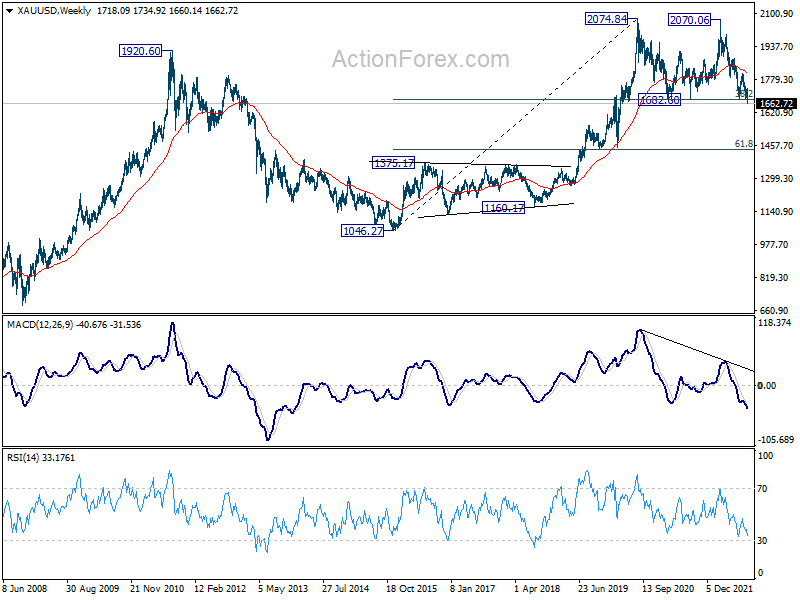

Technically, a big move came yesterday as Gold dived through key cluster support at around 1680 (which coincides with 38.% retracement of 1046.27 to 2074.84). A long term double top pattern should be formed with tops at 2074.84 and 2070.06. A weekly close below 1680 will affirm this bearish case. The stage would then be set for deeper fall to 61.8% retracement at 1439.18 in Q4. Downside momentum could intensify if US 10-year yield could break through 3.483 high decisively to resume medium term up trend.

{kind=link}

In Asia, at the time of writing, Nikkei is down -1.07%. Hong Kong HSI is down -0.52%. China Shanghai SSE is down -1.38%. Singapore Strait Times is down -0.06%. Japan 10-year JGB yield is up 0.0028 at 0.260. Overnight, DOW dropped -0.56%. S&P 500 fell -1.13%. NASDAQ lost -1.43%. 10-year yield rose 0.047 to 3.459.

RBA Lowe: Rate at 2.35% is still too low

RBA Governor Philip Lowe told the House of Representatives Standing Committee on Economics, interest rate at 2.35% is “still too low”. He added that over the longer term, the cash rate “should at least average the mid point of the inflation target”, which is 2.5%, if not a bit higher. Also, an average interest rate of about 3% was “possible”, and we’ll cycle around some number between 2.5 and 3.5.”

Lowe also warned that the longer inflation stays above 3%, “the more difficult it’s going to become” for Australians. If that. happens “then we have higher interest rates and a recession, which is damaging. “So we’ve got two difficult kind of positions at the moment: some pain now and hopefully real wages start rising again next year against the risk of not doing anything, just sitting on our hands and having inflation stay higher.”

NZ BusinessNZ manufacturing rose to 54.9, improving tone around underlying growth

New Zealand BusinessNZ Performance of Manufacturing Index rose slightly from 53.5 to 54.9 in August. Production rose from 50.8 to 54.6. Employment rose from 52.9 to 53.6. New orders rose from 50.8 to 59.2. Finished stocks rose from 48.7 to 50.8. Deliveries rose from 50.1 to 53.7.

BNZ Senior Economist, Craig Ebert stated ” that manufacturing production, in general, was holding its own in Q2, rather than drooping, was portrayed in the PMI readings for April May and June. And in July and August the PMI has moved on to suggest an improving tone around underlying growth.”

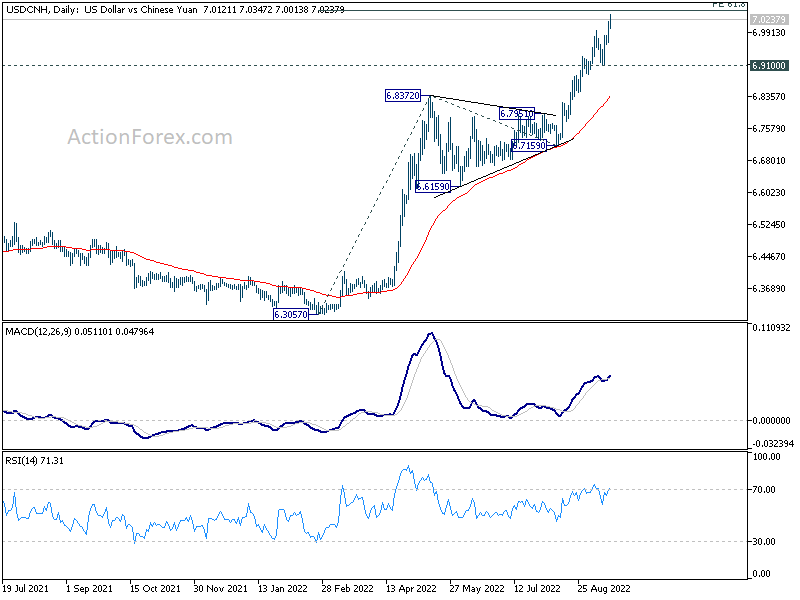

China data beat, but USD/CNH stays above 7

China industrial production rose 4.2% yoy in August, above expectation of 4.0% yoy. Retail sales rose 5.4% yoy, above expectation of 3.2% yoy. That’s the fastest pace since January-February period this year. Fixed asset investment rose 5.8% ytd yoy, above expectation of 5.6%.

“The economy held out against multiple unexpected headwinds in August and showed a positive recovery with the help of more additional supportive policies,” the NBS said in a statement. “The manufacturing needs are steady and rising, employment and prices are stable, most indices are better than last month.”

The set of better than expected data provided little support to the decline Yuan, with USD/CNH breaking through 7 psychological resistance this week. There is no sign of topping in the pair yet. USD/CNH is on track to 61.8% projection of 6.3057 to 6.8372 from 6.7159 at 7.0444. Firm break there will set the stage for pandemic high at 7.1961.

{kind=link}

{kind=link}

Elsewhere

UK retail sales dropped -1.6% mom in August, versus expectation of -0.6% mom. Ex-fuel sales dropped -1.6% mom, below expectation of -0.7% mom.

Looking ahead, Italy trade balance and Eurozone CPI final will be released in European session. Later in the day, Canada will release wholesales sales. US will release U of Michigan consumer sentiment.

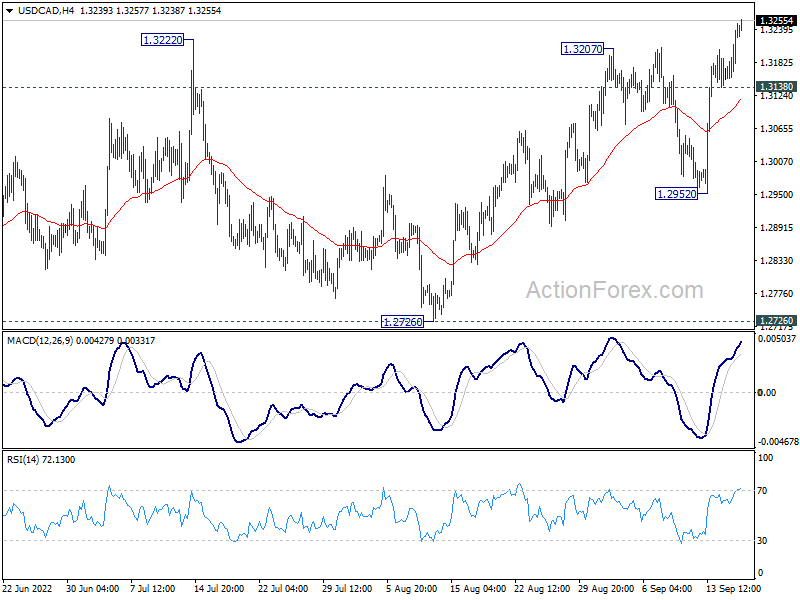

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3175; (P) 1.3208; (R1) 1.3261; More…

USD/CAD’s break of 1.3222 resistance confirms resumption of up trend from 1.2005. Intraday bias is back on the upside. Next target is 100% projection of 1.2005 to 1.2947 from 1.2401 at 1.3343. On the downside, below 1.3238 minor support will turn intraday bias neutral first. But retreat should be contained well above 1.2952 support to bring another rally.

In the bigger picture, down trend from 1.4667 (2020 high) should have completed at 1.2005, after defending 1.2061 long term cluster support. Rise from there should target 61.8% retracement of 1.4667 to 1.2005 (2021 low) at 1.3650. This will remain the favored case now as long as 1.2726 support holds.

{kind=link}

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Aug | 54.9 | 52.7 | ||

| 02:00 | CNY | Retail Sales Y/Y Aug | 5.40% | 3.20% | 2.70% | |

| 02:00 | CNY | Industrial Production Y/Y Aug | 4.20% | 4.00% | 3.80% | |

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Aug | 5.80% | 5.60% | 5.70% | |

| 06:00 | GBP | Retail Sales M/M Aug | -1.60% | -0.60% | 0.30% | |

| 06:00 | GBP | Retail Sales Y/Y Aug | -5.40% | -4.20% | -3.40% | -3.20% |

| 06:00 | GBP | Retail Sales ex-Fuel M/M Aug | -1.60% | -0.70% | 0.40% | |

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Aug | -5.00% | -3.40% | -3.00% | |

| 08:00 | EUR | Italy Trade Balance (EUR) Jul | -1.50B | -2.17B | ||

| 09:00 | EUR | Eurozone CPI Y/Y Aug F | 9.10% | 9.10% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Aug F | 4.30% | 4.30% | ||

| 12:30 | CAD | Wholesale Sales M/M Jul | 0.30% | 0.10% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Sep P | 59.8 | 58.2 |