Australian Dollar is trading mixed, slightly to the soft side, after RBA’s expected 50bps rate hike. There is basically no surprise out of the statement. Dollar is paring back some of recent gains while Yen is also soft. On the other hand, Sterling is leading Euro for a rebound while Canadian Dollar is also a touch firmer.

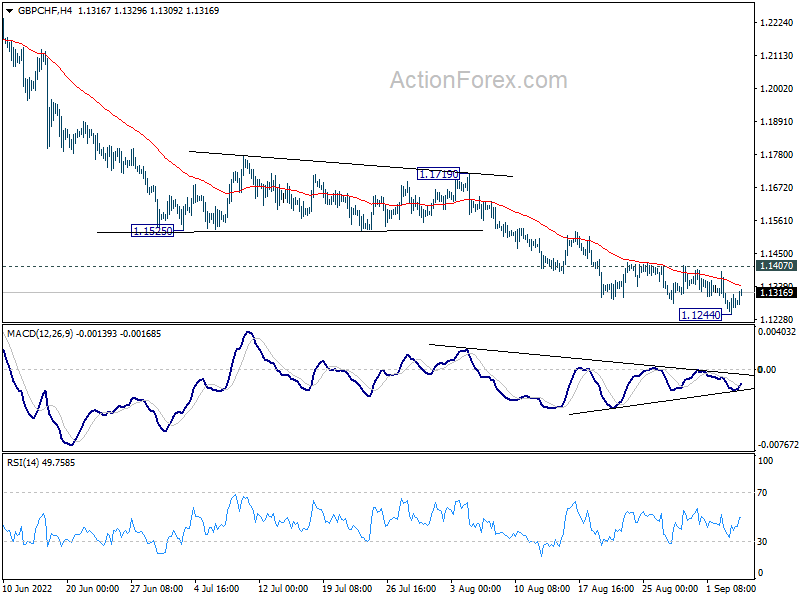

Technically, while Sterling is recovering, upside momentum is hardly convincing so far. GBP/CHF will need to break through 1.1407 minor resistance to indicate short term bottoming first, before having the prospect of stronger rebound. Otherwise, outlook in GBP/CHF will stay bearish, and upside of the Pound could also be capped elsewhere.

{kind=link}

In Asia, at the time of writing, Nikkei is up 0.09%. Hong Kong HSI is down -0.42%. China Shanghai SSE is up 1.01%. Singapore Strait Times is up 0.33%. Japan 10-year JGB yield is up 0.004 at 0.239.

RBA hikes 50bps to 2.35%, more over the months ahead

RBA raises cash rate target by 50bps to 2.35% as widely expected. The Board “expects to increase interest rates further over the months ahead”, but it’s “not on a pre-set path”. The size and timing of future hikes will be “guided by the income data and the Board’s assessment of the outlook for inflation and the labour market.”

Regarding inflation, RBA expects it to peak “later this year”. The central forecasts is for CPI to be around 7.75% over 2022, a little above 4% over 2023, and then around 3% over 2024.

The economy is “continuing to grow solidly” as boosted by a “record level of the terms of trade”. Labor market is “very tight” while wages growth “has picked up”.

It maintained that an important source of uncertainty is household spending, which is facing pressure from higher inflation and higher interest rates.

BoE Mann: Fast and forceful monetary tightening superior to gradualist approach

In a speech, BoE MPC member Catherine Mann said, “inflation today does not simply depend on past inflation but depends as well on markets, firms, and household’s expectations, and crucially, how these expectations react to each other, are formed over time, and interact with our and others’ policy choices. ”

“In this more complex and arguably more realistic and relevant version of the inflation model, a fast and forceful monetary tightening, potentially followed by a hold or reversal, is superior to the gradualist approach.”

“This policy strategy would reduce the risks of a more extended and costly tightening cycle later that depends primarily on shrinking aggregate demand.”

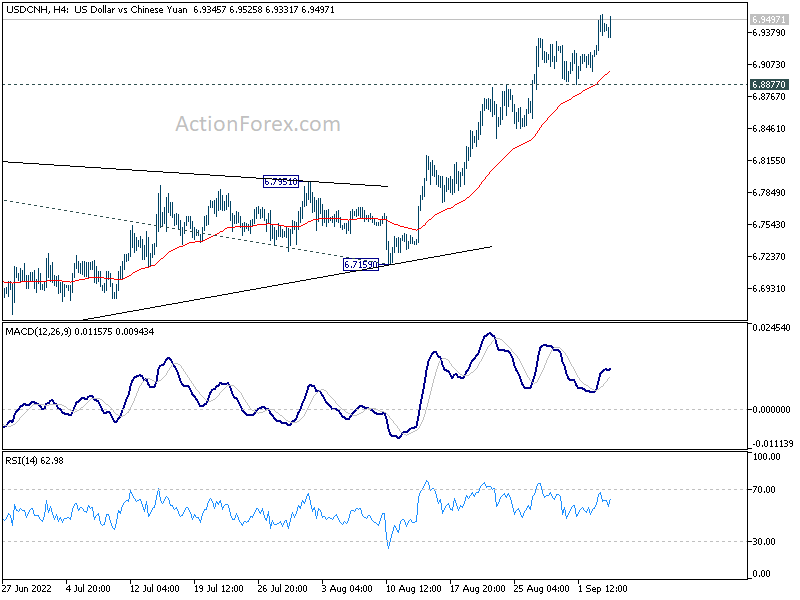

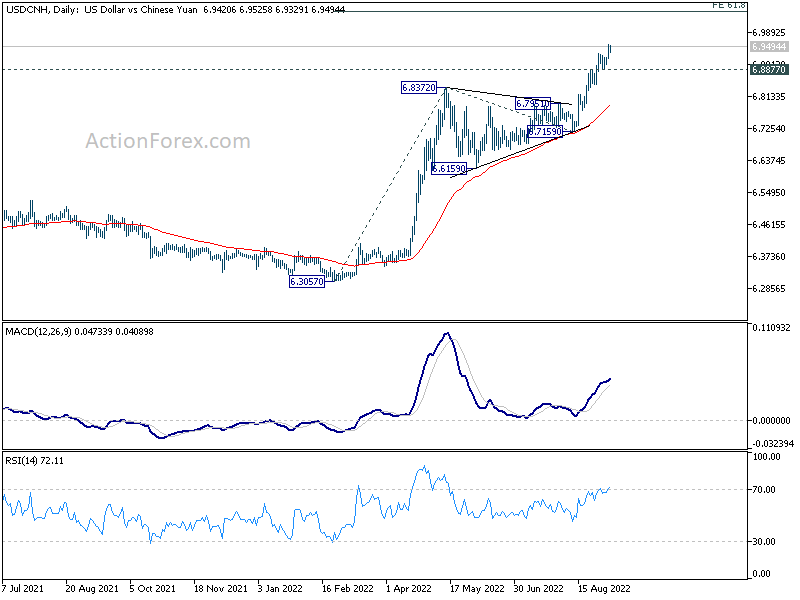

Yuan hit fresh 2-yr low, shrugging PBoC actions

The People’s Bank of China announced yesterday to cut the foreign exchange reserve requirement ratio (RRR) to 6% from 8% beginning September 15. That is, the amount of foreign-exchange deposits banks need to set aside as reserves will be lowered, freeing up funds to buy Yuan.

The move, together with a string of stronger-than expected exchange rate fixings, are seen as a strong signal on PBoC’s stance to at least slow Yuan’s depreciation. That came when Yuan hit fresh two-year low and with USD/CNH approaching psychological important 7 handle.

But USD/CNH’s rally (Yuan’s depreciation) is continuing. There is no sign of topping in USD/CNH as long as 6.8877 support holds, technically. It’s still on track to 61.8% projection of 6.3057 to 6.8372 from 6.7159 at 7.0444.

{kind=link}

{kind=link}

Looking ahead

Germany will release factory orders in European session. UK will publish PMI construction. Later in the day, US will release ISM services.

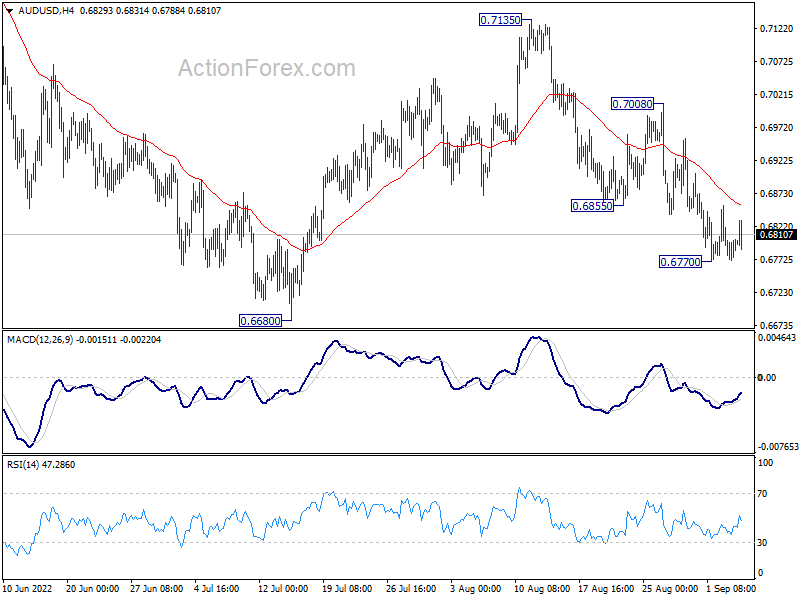

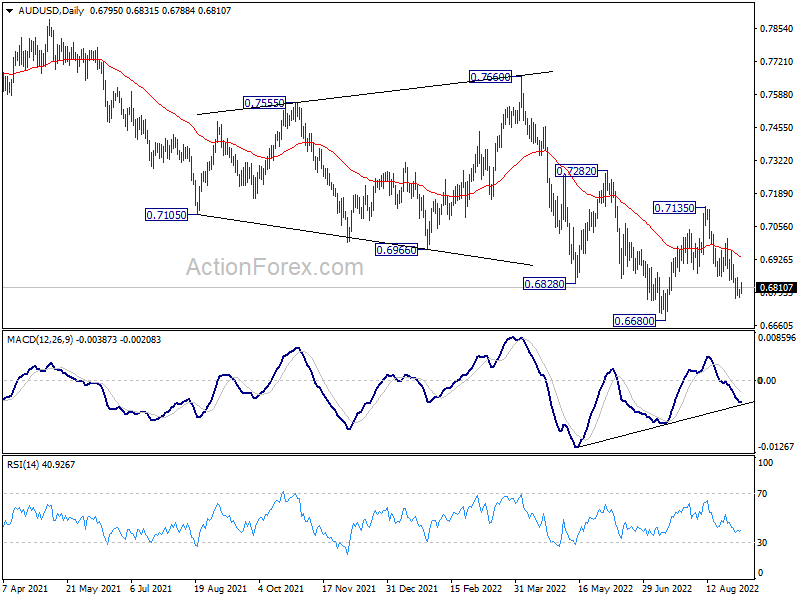

AUD/USD Daily Report

Daily Pivots: (S1) 0.6779; (P) 0.6792; (R1) 0.6810; More…

Intraday bias in AUD/USD is turned neutral with a temporary low formed at 0.6770. Further decline is expected as long as 0.7008 resistance holds. Break of 0.6770 will resume the decline from 0.7135 to retest 0.6680 low. Decisive break there will resume larger down trend.

{kind=link}

In the bigger picture, price actions from 0.8006 (2021 high) is seen more as a corrective pattern to rise from 0.5506 (2020 low). Or it could also be a bearish impulsive move. In either case, outlook will remain bearish as long as 0.7282 resistance holds. Next target is 61.8% retracement of 0.5506 to 0.8006 at 0.6461.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Aug | 0.50% | 1.60% | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Jul | 1.80% | 1.90% | 2.20% | |

| 23:30 | JPY | Overall Household Spending Y/Y Jul | 3.40% | 4.20% | 3.50% | |

| 01:30 | AUD | Current Account Balance (AUD) Q2 | 18.3B | 21.5B | 7.5B | |

| 04:30 | AUD | RBA Interest Rate Decision | 2.35% | 2.35% | 1.85% | |

| 06:00 | EUR | Germany Factory Orders M/M Jul | -0.20% | -0.40% | ||

| 08:30 | GBP | Construction PMI Aug | 48 | 48.9 | ||

| 13:45 | USD | Services PMI Aug F | 44.1 | 44.1 | ||

| 14:00 | USD | ISM Services PMI Aug | 55.4 | 56.7 |