Markets:

- S&P 500 down 3.4%

- Gold down $21 to $1737

- US 10-year yield up 1 bps to 3.03%

- WTI crude oil up $0.34 to $92.86

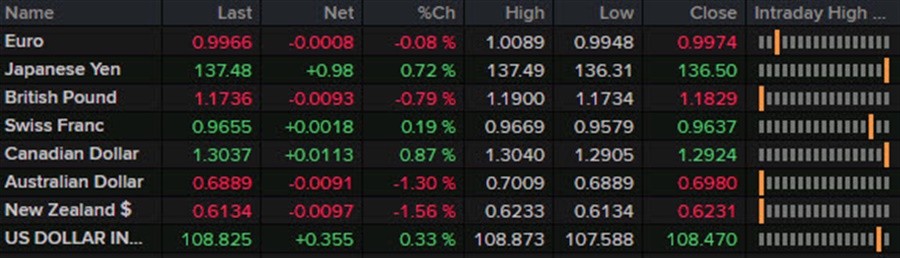

- USD leads, NZD lags

There was a dovish lean in the market before Powell as the PCE inflation report came in soft. That was validated by Bostic as he said it made him lean more slightly towards 50 bps in September.

However it all came undone with Powell. He delivered a crisp 8-minute speech that included strong language on holding rates higher for longer and taking ‘forceful’ action, which is a tool he hasn’t used before. In terms of clear signals, he said Sept was still undecided as they wait for data.

There was no big red flag in the speech that argued for buying the dollar and selling stocks. Instead it was the collective tone of the speech along with it’s brevity. It alluded to a clear parallel with the 1970s and the importance of keeping rates higher for longer rather than easing at the first sign of economic weakness or a retreat in inflation. Powell also emphasized that the Fed was prepared to tolerate economic pain to achieve its objectives.

I’d argue the Fed doesn’t have credibility on staying hawkish if the economy turns but the market certainly argued against that today. The initial reaction snowballed and the dollar bid hardly gave up a pip with virtually everything finishing at the extremes of the day.

The moves argue that equities were looking for some kind of dovish hint from Powell but couldn’t find it. Curiously though, the rates market didn’t move much on Powell. In bonds, the flight to safety bid would have helped that but even in Fed funds futures, the pricing was largely unchanged.

The euro had tried to stage a rally earlier and accelerated on the PCE data but was reeled in on Powell to finish unchanged and at the lowest weekly close since 2003.

Cable also suffered in a big outside day to finish 90 pips lower.

Oil managed to finish slightly higher but that was little help for the commodity currencies as they all fell, though the loonie was the best of the bunch.

Most importantly might have been USD/JPY as even in a brutal day for stocks, it added 100 pips. The yen has truly lost its safe haven status and that’s a big change. It reflects rate differentials at the moment and today’s move comes with hawkish Fed connotations so there’s a fundamental backing but long-term rates were lower today and this isn’t the first time. Beware of further dollar gains from here.