Dollar remains the worst performing major currency for the week, but the dynamics are shifting. Yen is giving up much of its gain, following the strong rebound in benchmark treasury yields, but Swiss Franc is still firm. Euro and Sterling are somewhat under pressure too, while smaller than expected GDP contraction gives the Pound little help. Commodity currencies are staying the strongest ones, as led by Kiwi and Aussie.

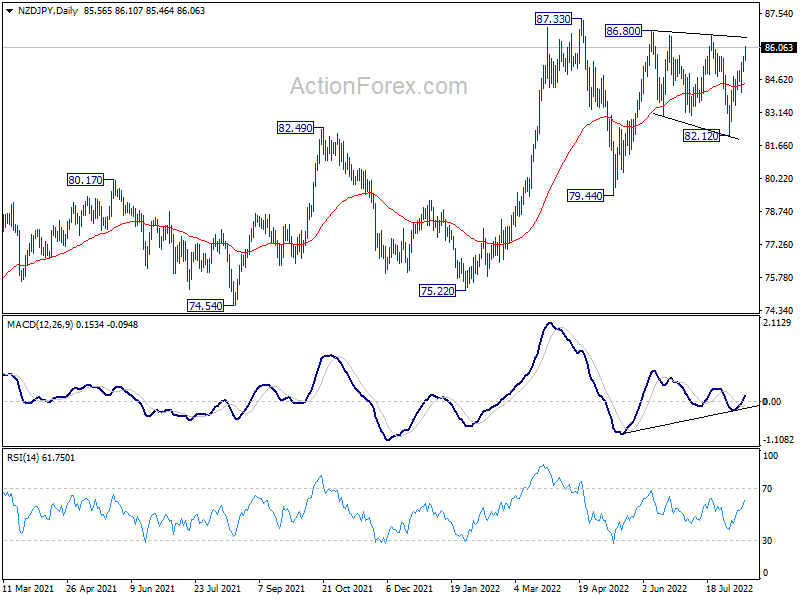

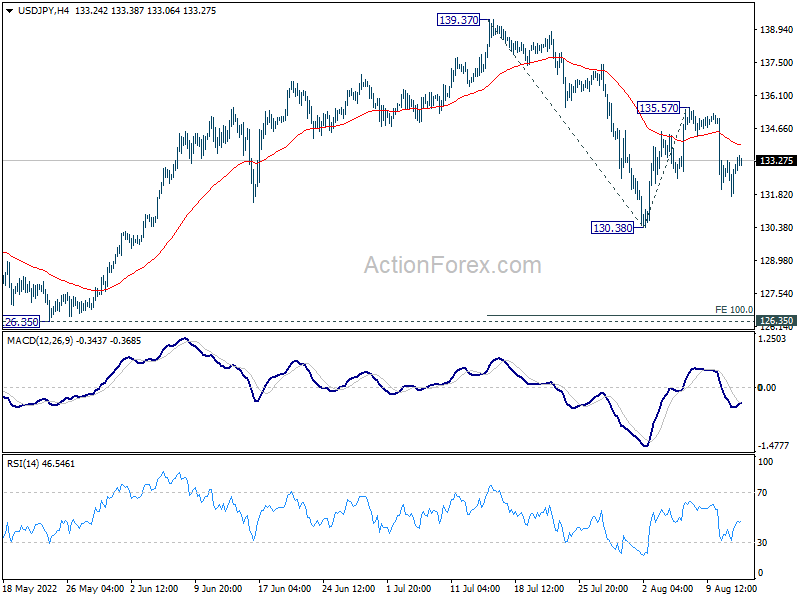

Technically, NZD/JPY looks set to take on 86.80/87.33 resistance zone with current strong rally. Decisive break there will resume larger up trend. If that happens, attention would also be on USD/JPY at the same time, on whether it would break through 135.57 minor resistance to resume the rebound from 130.38, towards 139.37 high.

{kind=link}

In Asia, Nikkei rose 2.62%. Hong Kong HSI is up 0.39%. China Shanghai SSE is up 0.04%. Singapore Strait Times is down -0.92%. Japan 10-year JGB yield is up 0.0046 at 0.198. Overnight, DOW rose 0.08%. S&P 500 dropped -0.07%. NASDAQ dropped -0.58%. 10-year yield rose 0.102 to 2.888.

UK GDP down -0.6% mom in Jun, -0.1% qoq in Q2

UK GDP contracted -0.6% mom in June, better than expectation of -1.3% mom. All main sectors contributed negatively to the monthly GDP estimate. Services was the main contributor, down -0.5%. Production dropped -0.9% mom. while construction also fell by -1.4% mom. Monthly GDP was still 0.9% above its pre-coronavirus levels in February 2020.

For the whole of Q2, GDP contracted -0.1% qoq, above expectation of -0.2% qoq. The level of GDP was 2.9% yoy higher than Q2 2021. Also, compared with the same quarter a year ago, the implied GDP deflator rose by 6.0%, primarily reflecting the 7.3% increase in the price of household consumption expenditure, which is the fastest annual household deflator growth rate since 1991.

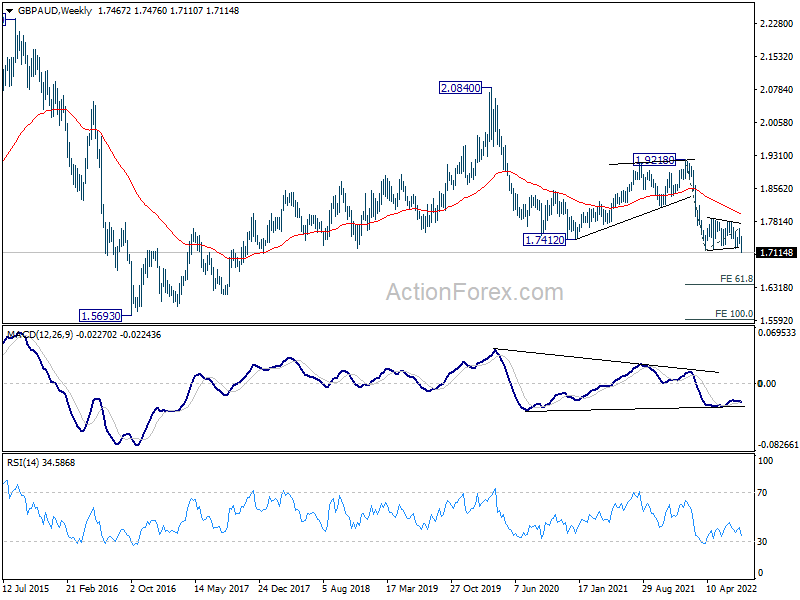

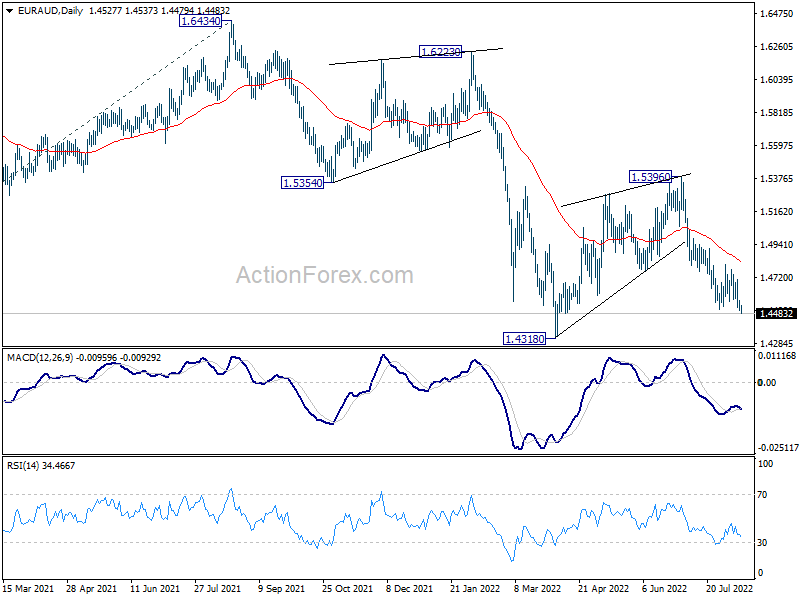

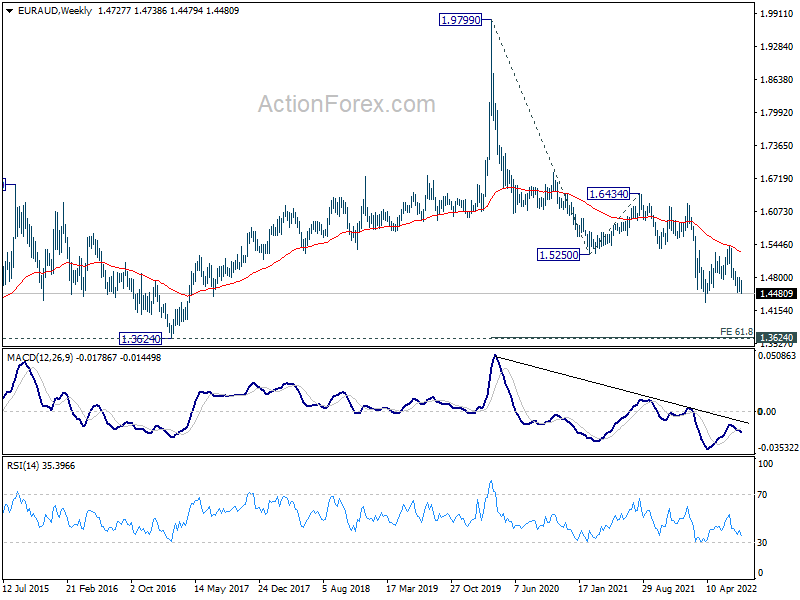

GBP/AUD breaks out from medium term range, EUR/AUD to follow

GBP/AUD finally broke out from medium term consolidation and resume down trend this week. EUR/AUD is also following and look ready for down trend resumption too. The development came as commodity currencies generally responded better to receding expectation of another 75bps Fed hike, than European majors.

GBP/AUD’s fall is seen as part of the down trend from 1.9218, as well as that from 2.0840 (2020 high). Both near term and medium term bearishness are maintained well with the cross capped by falling 55 day and 55 week EMA. Next target is 61.8% projection of 1.9218 to 1.7171 from 1.7649 at 1.6384.

{kind=link}

{kind=link}

EUR/AUD also resumed the fall from 1.5396 through 1.4580 support. It’s now targeting 1.4318 low (corresponding to GBP/AUD’s 1.7171 support). Firm break there will resume whole down trend from 1.9799 (2020 high), and target 61.8% projection of 1.9799 to 1.5250 from 1.6434 at 1.3623, which is close to 1.3624 long term support (2017 low).

{kind=link}

{kind=link}

USD/JPY Daily Outlook

Daily Pivots: (S1) 132.04; (P) 132.67; (R1) 133.62; More…

Intraday bias in USD/JPY is turned neutral first, as it recovered well ahead of 130.38 support. Overall outlook is unchanged that price actions from 139.37 are developing into a corrective pattern to larger up trend. Below 130.38 will target 100% projection of 139.37 to 130.38 from 135.57 at 126.58. But downside should be contained by 126.35 structure support. On the upside, above 135.57 will resume the rebound form 130.38 to retest 139.37, but firm break there is not expected even in this case.

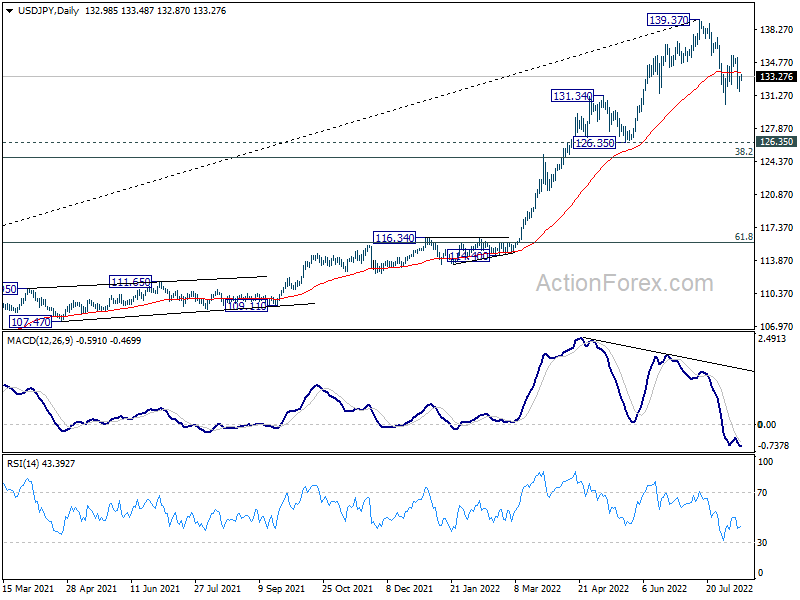

In the bigger picture, fall from 139.37 medium term top is seen as correcting whole up trend from 101.18 (2020 low). While deeper decline cannot be ruled out, outlook will stays bullish as long as 55 week EMA (now at 121.84) holds. Long term up trend is expected to resume through 139.37 at a later stage, after the correction finishes.

{kind=link}

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Jul | 52.7 | 49.7 | ||

| 06:00 | GBP | GDP M/M Jun | -0.60% | -1.30% | 0.50% | |

| 06:00 | GBP | GDP Q/Q Q2 P | -0.10% | -0.20% | 0.80% | |

| 06:00 | GBP | Industrial Production M/M Jun | -0.90% | -0.80% | 0.90% | 1.30% |

| 06:00 | GBP | Industrial Production Y/Y Jun | 2.40% | 1.60% | 1.40% | 1.80% |

| 06:00 | GBP | Manufacturing Production M/M Jun | -1.60% | -1.70% | 1.40% | 1.70% |

| 06:00 | GBP | Manufacturing Production Y/Y Jun | 1.30% | 1.30% | 2.30% | 2.60% |

| 06:00 | GBP | Index of Services 3M/3M Jun | -0.40% | -0.40% | 0.10% | 0.00% |

| 06:00 | GBP | Goods Trade Balance (GBP) Jun | -22.8B | -22.3B | -21.4B | |

| 08:00 | EUR | Italy Trade Balance (EUR) Jun | 0.35B | -0.01B | ||

| 09:00 | EUR | Eurozone Industrial Production M/M Jun | 0.00% | 0.80% | ||

| 12:30 | USD | Import Price Index M/M Jul | -0.50% | 0.20% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Aug P | 52.3 | 51.5 |