Dollar selling is back today while Yen’s strength continues. Euro is also soft as the second worst after the greenback. On other hand hand, Sterling is strengthening with help from buying against Euro. Commodity currencies are mixed for now, with Canadian Dollar turning softer while Kiwi leads Aussie higher. Stock market sentiment is mixed, and will probably need some guidance from this week’s important data releases, starting from ISM manufacturing today.

Technically, one interesting development to note is the interplay between Dollar and Euro. EUR/USD is still range bound while both are being pressured elsewhere. GBP/USD and AUD/USD are already resuming near term rebound, after very brief retreat. At the same time, EUR/GBP and EUR/AUD look on the verge of decline resumption. Let’s see if the developments in GBP/USD, AUD/USD, EUR/GBP and EUR/AUD would help squeeze EUR/USD out of range, or keep it inside.

In Europe, at the time of writing, FTSE is up 0.20%. DAX is up 0.08%. CAC is up 0.05%. Germany 10-year yield is down -0.009 at 0.805. Earlier in Asia, Nikkei rose 0.69%. Hong Kong HSI rose 0.50%. China Shanghai SSE rose 0.21%. Singapore Strait Times rose 0.85%. Japan 10-year JGB yield rose 0.0026 to 0.186.

UK PMI manufacturing finalized at 52.1, shifted into reverse gear

UK PMI Manufacturing was finalized at 52.1 in July, down from 52.8 in June. That’s also the lowest level in 25 months. S&P Global said that output fell in consumer and intermediate goods industries. Job created accelerated as companies addressed staff shortages.

Rob Dobson, Director at S&P Global Market Intelligence, said:

“The UK manufacturing sector shifted into reverse gear at the start of the third quarter. Output contracted for the first time since May 2020, as new order intakes suffered the first back-to-back monthly decreases for two years.

“Rising market uncertainty, the cost of living crisis, war in Ukraine, ongoing supply issues and inflationary pressures are all hitting demand for goods at the same time, while lingering post-Brexit issues and the darkening global economic backdrop are hampering exports.

“With the Bank of England implementing further interest rate hikes to combat inflation, the outlook is beset with downside risks. With this in mind, the continued low degree of optimism among manufacturers is of little surprise.”

Eurozone unemployment rate unchanged at 6.6% in Jun, EU at 7.2%

Eurozone unemployment rate was unchanged at 6.6% in June, matched expectations. EU unemployment rate was also stable at 7.2%.

Eurostat estimates that 12.931 million men and women in the EU, of whom 10.925 million in the euro area, were unemployed in June 2022. Compared with June 2021, unemployment decreased by 2.311 million in the EU and by 1.957 million in the euro area.

Eurozone PMI manufacturing finalized at 49.8, sinking into increasingly steep downturn

Eurozone PMI Manufacturing was finalized at 49.8 in July, down from 52.1. That’s also a 25-month low. PMI Manufacturing Output Index was finalized at 46.3, down from June’s 49.3, a 26-month low.

Looking at some member states, PMI manufacturing in the Netherlands dropped to 20-month low at 54.5. Austria recovered to 2-month high at 51.7. France (49.6, 26-month low), Germany (49.3, 25-month low), Greece (49.1, 19-month low), Spain (48.7, 26-month low), and Italy (48.5, 25-month low) were all in contraction.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “Eurozone manufacturing is sinking into an increasingly steep downturn, adding to the region’s recession risks….

“Production is falling at especially worrying rates in Germany, Italy and France, but is also now in decline in all other surveyed countries except the Netherlands, and even here the rate of growth has slowed sharply…

“The energy crisis adds to the risks that not only will weaker demand and destocking cause manufacturing production to decline at an increased rate in the coming months, but reduced energy supply will act as an additional drag on the sector.”

China Caixin PMI manufacturing dropped to 50.4, continued recovery

China Caixin PMI Manufacturing dropped from 51.7 to 50.4 in July, below expectation of 51.5. Caixin said there were softer increases in output and new orders. Employment fell at quicker pace. Input cost inflation slowed notably while prices charged fell again.

Wang Zhe, Senior Economist at Caixin Insight Group said: “In general, the eased Covid situation and restrictions facilitated a continuous recovery in the manufacturing sector in July. Supply and demand continued to improve, with supply stronger than demand. Employment lagged, remaining in contractionary territory. Costs gradually rose, with output prices on the decline, posing challenges for company profits. The market held on to positive sentiment, along with concerns about the economic outlook.

Released yesterday, the official PMI manufacturing dropped from 50.2 to 49.0, back in contraction. PMI non-manufacturing dropped form 54.7 to 53.8.

Japan PMI manufacturing finalized at 52.1, headline masked worrying trends

Japan PMI Manufacturing was finalized at 52.1 in July, down from June’s 52.7. That’s the lowest level since September 2021. S&P Global said there were renewed reductions in output and new orders. The softest rise in outstanding business 17 months was due to weaker demand. Rising prices and delivery delays led to accelerated stock building.

Usamah Bhatti, Economist at S&P Global Market Intelligence, said: “The headline PMI masked some worrying trends when looking at the underlying sub-indices, which add downside risks for the sector. New order inflows fell for the first time in ten months and at the fastest pace since November 2020, which contributed to a renewed contraction in production levels – the first since February.

“Weaker demand conditions also contributed to reduced pressure on operating capacity. Backlogs of work increased at the softest rate in 17 months… Anecdotal evidence also pointed to an acceleration in stock building activity among Japanese goods producers.”

Australia AiG manufacturing dropped to 52.5, manufacturers simply can’t meet demand

Australia AiG Performance of Manufacturing Index dropped -1.5 to 52.5 in July. Looking at some details, production dropped sharply by -7.2 to 47.5. Employment dropped -0.9 to 50.1. New orders rose 4.2 to 59.9. Supplier deliveries dropped -4.1 to 47.4. Exports dropped -1.8 to 51.2. Input prices dropped -9.6 to 79.7. Selling prices dropped -3.3 to 64.5.

Innes Willox, Chief Executive of Ai Group said: “The supply and labour constraints afflicting the Australian economy are weighing heavily on the manufacturing sector. Production and employment both fell in July, as manufacturers struggle with chronic labour shortages and supply chain interruptions. New orders rose this month, but our manufacturers simply can’t meet this demand without more workers.”

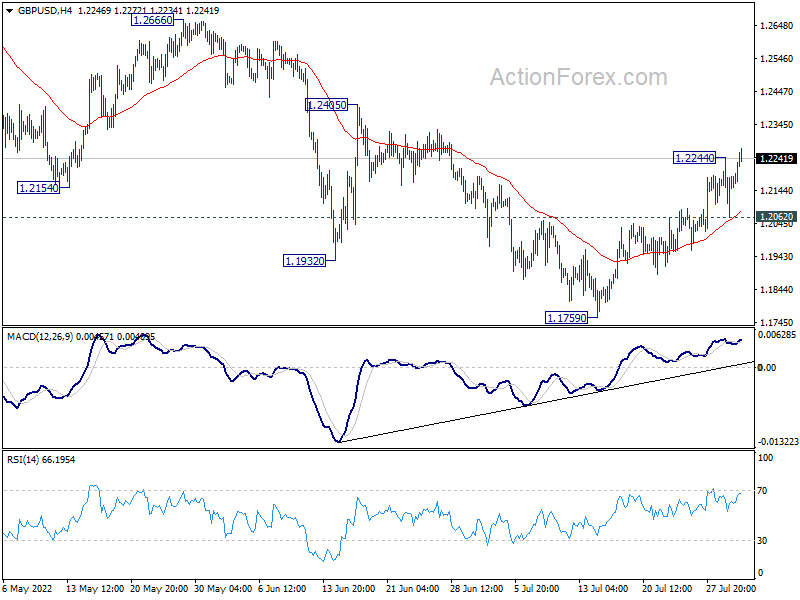

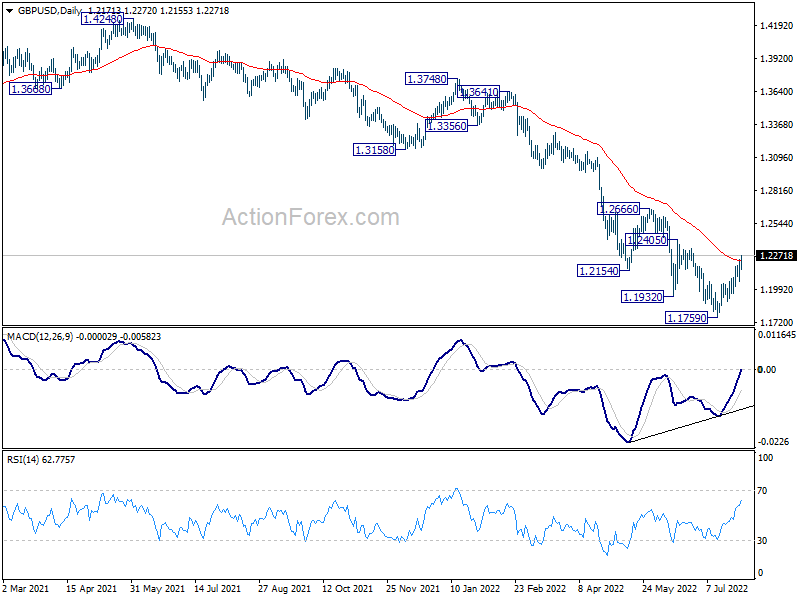

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2078; (P) 1.2162; (R1) 1.2261; More…

Intraday bias in GBP/USD is back on the upside as rebound form 1.1759 resumed after brief retreat. Further rally should be seen to 1.2405 resistance first. Firm break there will target 1.2666 key resistance next. On the downside, however, break of 1.2062 minor support will argue that the rebound is over, and turn bias back to the downside for retesting 1.1759 low instead.

{kind=link}

In the bigger picture, fall from 1.4248 (2018 high) could be a leg inside the pattern from 1.1409 (2020 low), or resuming the longer term down trend. Deeper decline is expected as long as 1.2666 resistance holds. Next target is 1.1409 low. However, firm break of 1.2666 will bring stronger rise back to 55 week EMA (now at 1.2957).

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Mfg Index Jul | 52.5 | 54 | ||

| 22:45 | NZD | Building Permits M/M Jun | -2.30% | -0.50% | ||

| 00:30 | JPY | Manufacturing PMI Jul F | 52.1 | 52.2 | 52.2 | |

| 01:00 | AUD | TD Securities Inflation M/M Jul | 1.20% | 0.30% | ||

| 01:45 | CNY | Caixin Manufacturing PMI Jul | 50.4 | 51.5 | 51.7 | |

| 06:00 | EUR | Germany Retail Sales M/M Jun | -1.60% | 0.60% | ||

| 07:45 | EUR | Italy Manufacturing PMI Jul | 48.5 | 49.1 | 50.9 | |

| 07:50 | EUR | France Manufacturing PMI Jul F | 49.5 | 49.6 | 49.6 | |

| 07:55 | EUR | Germany Manufacturing PMI Jul F | 49.3 | 49.2 | 49.2 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jul F | 49.8 | 49.6 | 49.6 | |

| 08:00 | EUR | Italy Unemployment Jun | 8.10% | 8.10% | 8.10% | 8.20% |

| 08:30 | GBP | Manufacturing PMI Jul F | 52.1 | 52.2 | 52.2 | |

| 09:00 | EUR | Eurozone Unemployment Rate Jun | 6.60% | 6.60% | 6.60% | |

| 13:45 | USD | Manufacturing PMI Jul F | 52.3 | 52.3 | ||

| 14:00 | USD | ISM Manufacturing PMI Jul | 52 | 53 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jul | 73.5 | 78.5 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Jul | 47.3 | |||

| 14:00 | USD | Construction Spending M/M Jun | 0.20% | -0.10% |