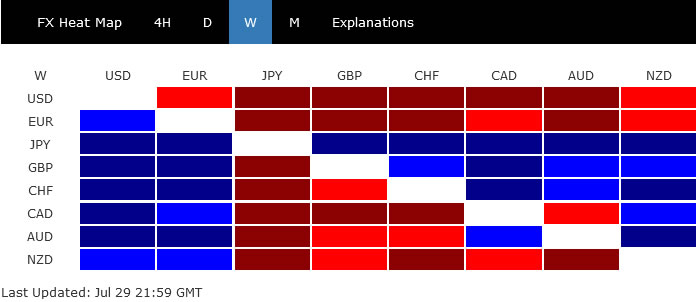

Dollar ended broadly lower last week, as the worst performer, as hammered by the events of FOMC meeting and GDP release. In short, Fed chair has signalled slower tightening pace ahead and the message was reinforced by another quarterly GDP contraction print. Whether the US was already in recession or not, Fed is turning from an auto-pilot mode to a data-dependent mode, after interest rate reached neutral range.

Euro hasn’t been able to capitalize on Dollar’s selloff, and ended as the second worst. Europe has it own problem of continuing war in Ukraine, inflation, and additional threat of Russia gas supply crunch. Yen was the winner responding to fall of major global benchmark yield. Sterling and Swiss Franc were the next strongest, as supported by buying against Euro. Commodity currencies were mixed, as partly supported by risk-on sentiment.

{kind=link}

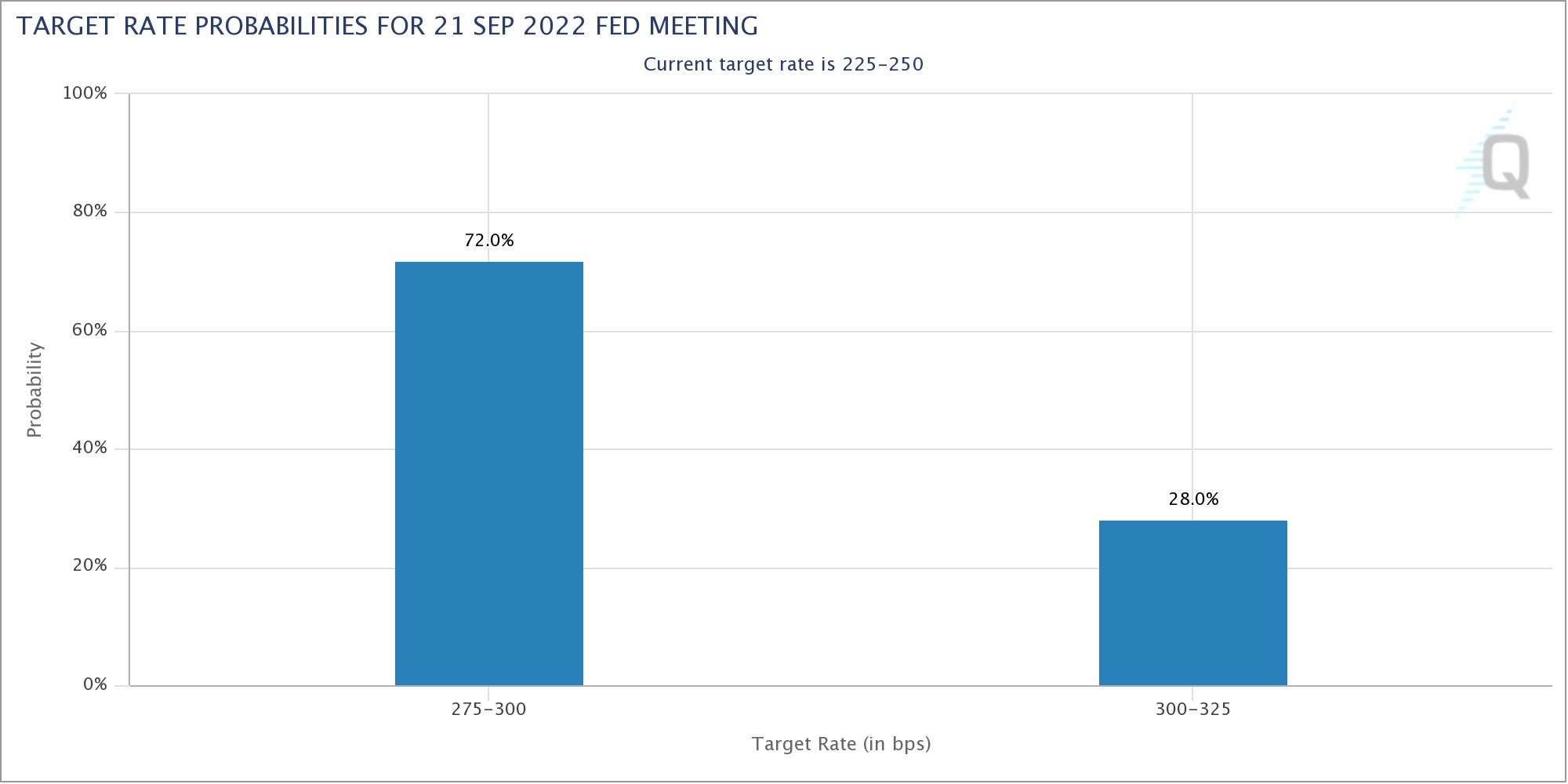

Market expecting Fed to slow tightening pace

Fed delivered another 75bps rate hike to bring the federal funds rate to 2.25-250% last week, which should now be in neutral range. Chair Jerome Powell then indicate that “as the stance of monetary policy tightens further, it likely will become appropriate to slow the pace of increases while we assess how our cumulative policy adjustments are affecting the economy and inflation.”

Just a day later, US GDP data showed the second consecutive quarter of contraction, at -0.9% annualized in Q2. There were debates on whether the US economy was already in recession, as a number of other data remained strong, including jobs. But the figure did affirm that case for, at least, slowing down the tightening pace as rates will be entering into restrictive zone.

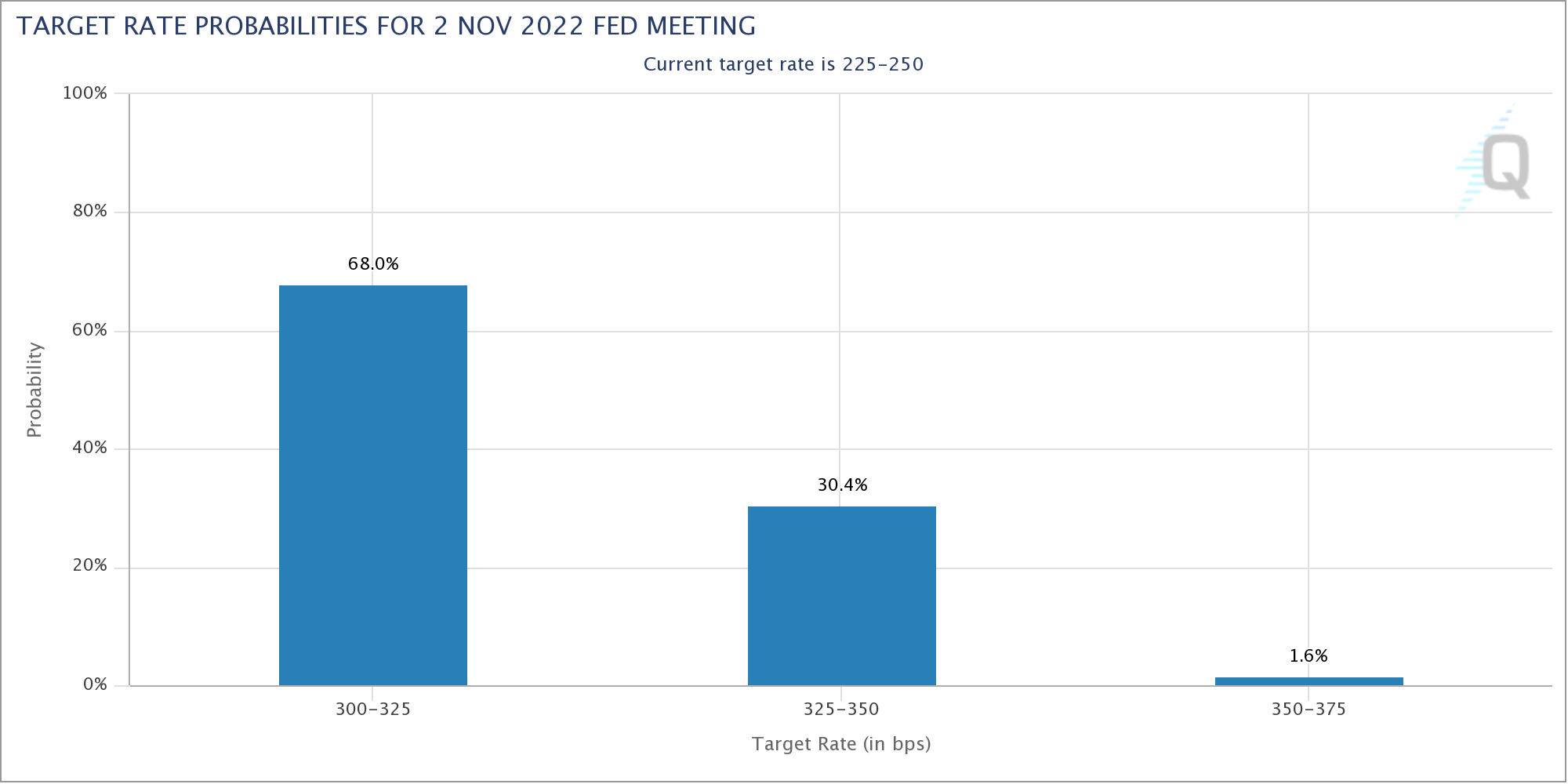

Markets are now pricing in 72% chance of a 50bps hike at the September FOMC meeting, and 68% chance of another 25bps hike in November.

{kind=link}

{kind=link}

S&P 500 now facing critical resistance zone after strong rebound

Stocks responded positive to both the FOMC and GDP events. S&P 500 extended the rebound from 3636.87 and closed strongly at 4130.29. The development affirms the case that correction from 4818.62 high is already complete at 3636.87. But SPX still needs to overcome and important resistance at around current level.

The cluster resistance zone include channel resistance at around 4142, 4177.51 resistance, and 55 week EMA at 4186.02. Sustained break of these levels will add more credence to this bullish case, and should set the stage for further rally back towards 4818.62 high, probably by the end of the year. In any case, further rise is in favor now as long as 3910.74 support holds, in case of retreat.

{kind=link}

{kind=link}

US 10-year yield to target 2.41 next as correction extends

US treasury yields fell notably last week. 10-year yield even broke through key structural support at 2.709. It’s clearly in correction to the whole up trend from 1.343. Deeper fall should be seen as long as 2.845 resistance holds, to 50% retracement of 1.343 to 3.483 at 2.413 and possibly below. The correction might extend to 55 week EMA (now at 2.222) before completion.

{kind=link}

{kind=link}

Dollar index to face important support at 55 day EMA

As a result of falling yield and risk-on sentiment, as well as expectation of slower Fed tightening, Dollar ended the week broadly lower. Dollar index’s correction from 109.29 extended lower last week and further decline is expected as long as 107.42 resistance holds, to 55 day EMA (now at 105.01).

It’s still a bit early to declare that DXY is already in a medium term correction. Rebound from 55 day EMA would keep outlook bullish for another rally through 109.29 sooner rather than later.

However, sustained break of 55 day EMA will raise the chance that it’s already correcting the up trend from 89.20. In that case, deeper decline would be seen to 38.2% retracement of 89.20 to 109.29 at 101.61, which is close to 101.29 structural support, before completing the correction. That could happen is the stock rally and yield decline gather more momentum.

{kind=link}

{kind=link}

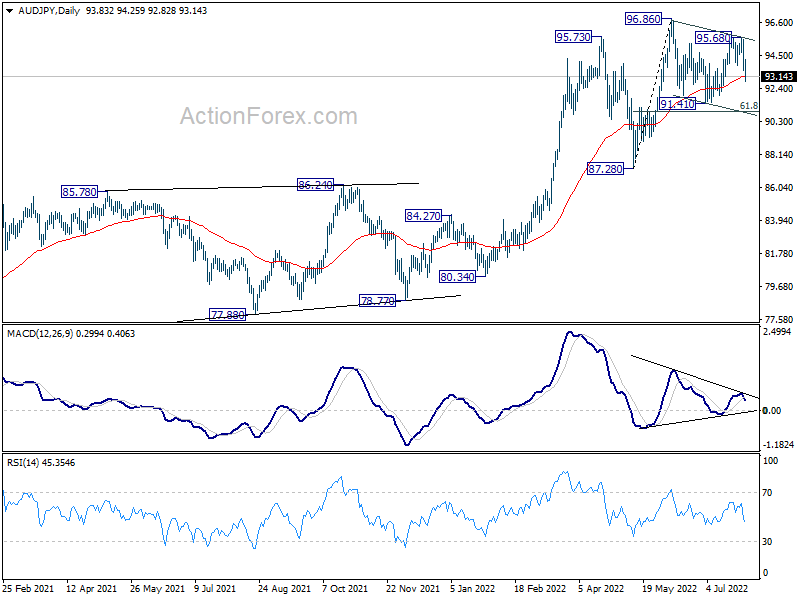

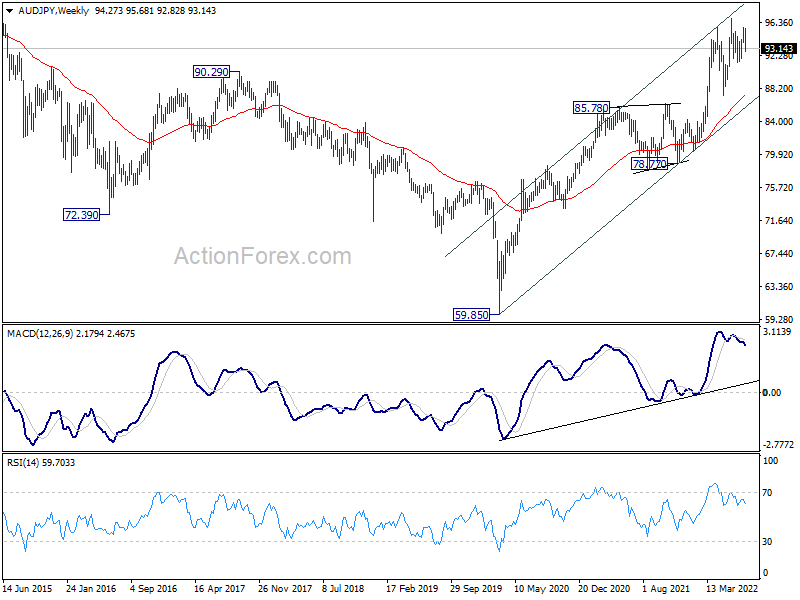

Outlook of AUD/JPY and CAD/JPY not too bearish yet despite Yen rally

Yen clearly reacted more to falling major benchmark yield then to risk-on sentiment. Germany 10-year yield closed down at 0.814, comparing to 1.937 high made just back on June 16. UK 10-year yield also closed down at 1.861, comparing to 2.738 high, also made on June 16. Japan 10-year yield was also down at 0.183, but the yield gaps had clearly narrowed.

But Yen’s strength was relatively less apparent against commodity currencies. AUD/JPY’s price actions from 96.86 could still be considered a corrective pattern to rise from 87.28 only, instead of the larger up trend from 78.77. While deeper fall could be seen to 91.41 support, strong support might be seen from 61.8% retracement of 87.28 to 96.86 at 90.93 to bring rebound. That would keep favor on the less bearish case. Nevertheless, sustained break of 90.93 will open up deeper decline to 55 week EMA (now at 87.36), which is close to 87.28 support.

{kind=link}

{kind=link}

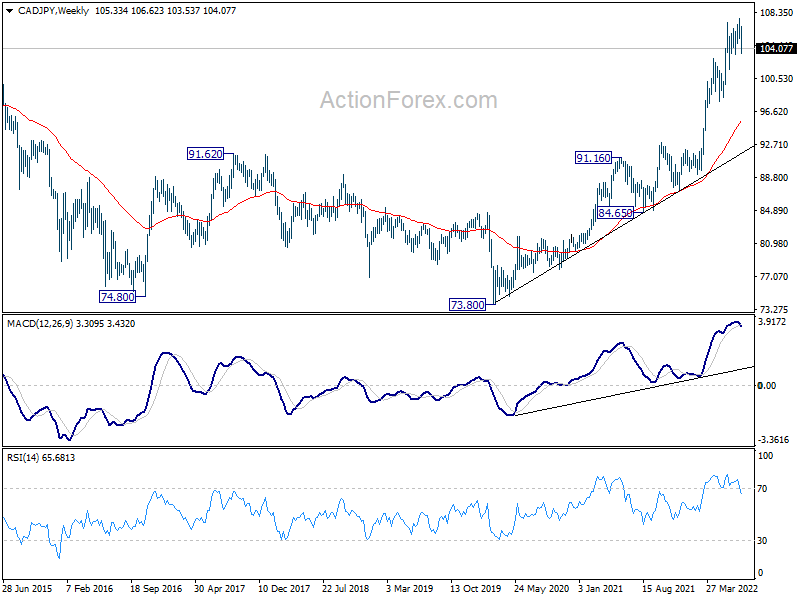

CAD/JPY could also still be seen as in a near term correction only, as long as 101.64 cluster support holds (61.8% retracement of 97.78 to 107.62 at 101.53). However, sustained break there will argue that it’s already correcting the whole up trend from 84.65. In this case, deeper decline could be seen through 97.78 support.

{kind=link}

{kind=link}

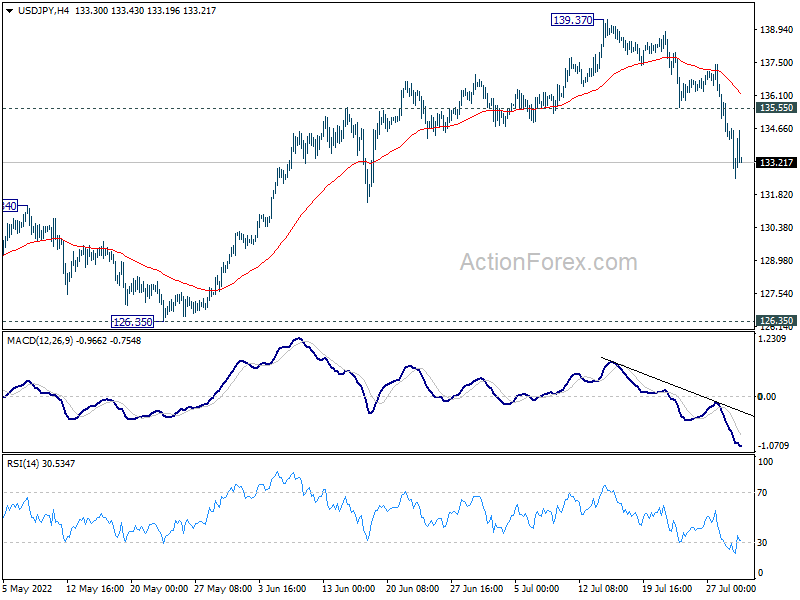

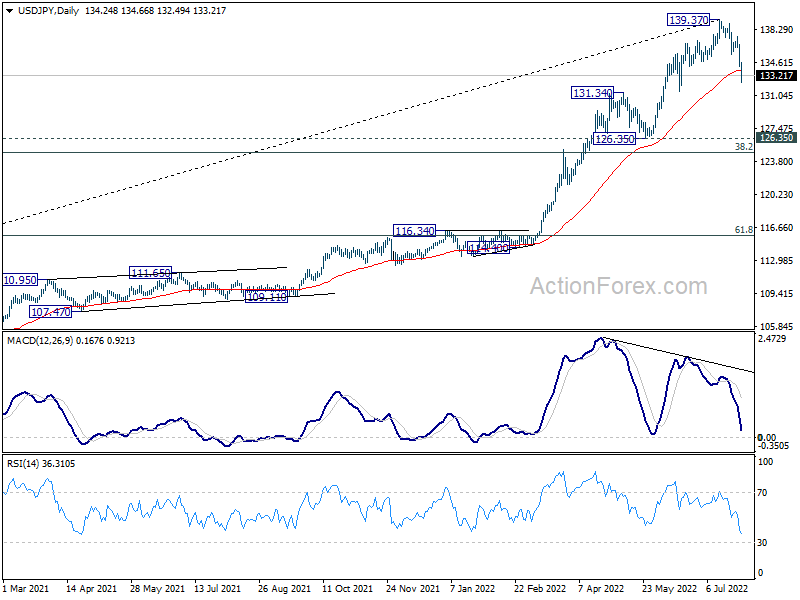

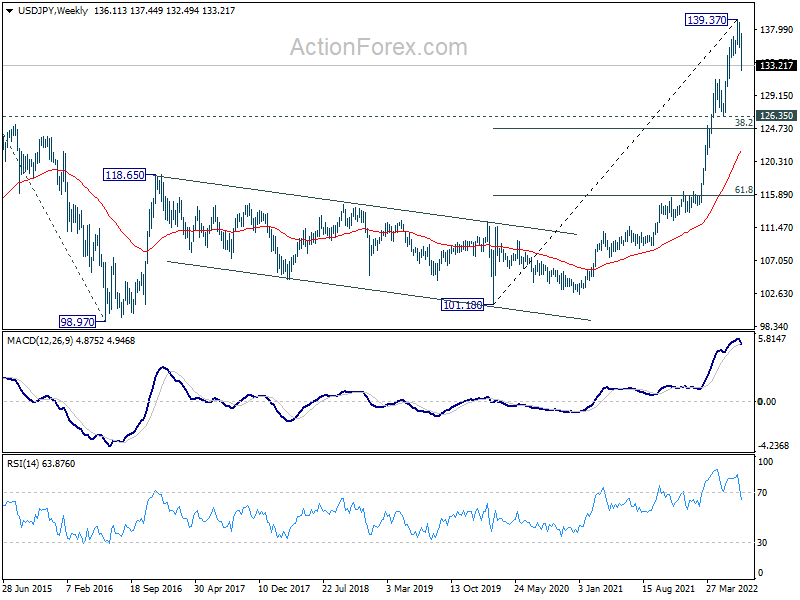

USD/JPY Weekly Outlook

USD/JPY’s decline from 139.37 accelerated lower last week. The development suggest that a medium term was already formed on bearish divergence condition in daily MACD. Initial bias stays on the downside this week for 131.34 resistance turned and below. But strong support is expected above 126.35 to contain downside, at least on first attempt, to bring rebound. On the upside, firm break of 135.55 will bring stronger rise back to retest 139.37 high instead.

{kind=link}

In the bigger picture, a medium term top should be in place at 139.37, on bearish divergence condition in daily MACD. Fall from there could be correcting whole up trend from 101.18 (2020 low). While deeper decline cannot be ruled out, outlook will stays bullish as long as 55 week EMA (now at 121.84) holds. Long term up trend is expected to resume through 139.37 at a later stage, after the correction finishes.

{kind=link}

In the long term picture, rise 101.18 is seen as part of the up trend from 75.56 (2011 low). Further rally is expected to 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 149.26, which is close to 147.68 (1998 high). This will remain the favored case as long as 55 week EMA holds.

{kind=link}

{kind=link}