Dollar’s correction continues today and falls broadly. US stocks point to stronger extended rebound. Yen is also weak. Kiwi is currently the strongest, followed by Australian. Euro and Swiss Franc are next. In particular, Euro is lifted by reports that ECB would consider both a 25bps and 50bps hike this Thursday. Sterling also follows Euro higher.

Technically, AUD/USD’s break of 0.6873 minor resistance confirms short term bottoming at 0.6680 and further rise would be seen to 55 day EMA (now at 0.6973). Now, it’s GBP/USD’s turn and break of 1.2055 will also confirm short term bottoming at 1.1759. However, if EUR/GBP could break through 0.8552 minor resistance, such development could cap Sterling’s rally.

In Europe, at the time of writing, FTSE is up 0.47%. DAX is up 0.44%. CAC is up 0.40%. Germany 10-year yield is up 0.048 at 1.263. Earlier in Asia, Nikkei rose 0.65%. Hong Kong HSI dropped -0.89%. China Shanghai SSE rose 0.04%. Singapore Strait Times dropped -0.13%. Japan 10-year JGB yield rose 0.0077 to 0.242.

Eurozone CPI finalized at 8.6% yoy in Jun, core CPI at 3.7% yoy

Eurozone CPI was finalized at 8.6% yoy in June up from May’s 8.1% yoy. Excluding energy, food, alcohol & tobacco, CPI was finalized at 3.7% yoy, down form May’s 3.8% yoy. The highest contribution to the annual Eurozone inflation rate came from energy (+4.19%), followed by food, alcohol & tobacco (+1.88%), services (+1.42%) and non-energy industrial goods (+1.15%).

EU CPI was finalized at 9.6% yoy, up from May’s 8.8% yoy. The lowest annual rates were registered in Malta (6.1%), France (6.5%) and Finland (8.1%). The highest annual rates were recorded in Estonia (22.0%), Lithuania (20.5%) and Latvia (19.2%). Compared with May, annual inflation fell in two Member States and rose in twenty-five.

UK payrolled employees rose 31k in Jun, unemployment rate unchanged at 3.8% in May

UK number of payrolled employees rose 31k in the month of June to a record 29.6m. Comparing with June 2021, payrolled employees rose 3.0% or 874k. Claimant count dropped -20k in the month, versus expectation of -41.2k.

Unemployment rate in the three months to May dropped was unchanged at 3.8%, matched expectations. Over the previous quarter, unemployment rate was down -0.1%, employment rate rose 0.4%, economic inactivity rate dropped -0.4%, hours worked rose 6.5m.

Average earnings including bonus rose 6.2% 3moy in may, below expectation of 6.8%. Average earnings excluding bonus rose 4.3% 3moy, matched expectations.

RBA minutes: Arguments for 50bps hike stronger than 25bps in Jul

In the minutes of the July 5 meeting, RBA noted that members considered raising interest rates by 25bps or 50bps. The arguments for a 50bps hike were “stronger”.

“The level of interest rates was still very low for an economy with a tight labour market and facing a period of higher inflation,” the minutes noted. “Members viewed it as important that inflation expectations remained well anchored and that the period of higher inflation be temporary.”

Also, board members agreed that “further steps would need to be taken to normalise monetary conditions in Australia over the months ahead,” The “size and timing” of future hikes will be guided by “incoming data” and assessment of the outlook for “inflation and labor market”.

RBA Bullock: Households in fairly good position for rate hikes

In a speech, RBA Deputy Governor Michelle Bullock said households are in a “fairly good position” for interest rate increases. It’s “unlikely” that there will be substantial financial stability arising from the household sector, but risks are “a little elevated”.

The household sector has “large liquidity buffers”, with “substantial equity” in housing assets. Much of the debt is held by “high-income households” while low fixed rate loans have give time for preparation for high rates. But rate hikes could impact households’ debt servicing burden and cash flow. Risk play out will also be included by future path of employment growth.

“This, along with the Board’s assessment of the outlook for inflation, will be important considerations in deciding the size and timing of future interest rate increases,” she concluded.

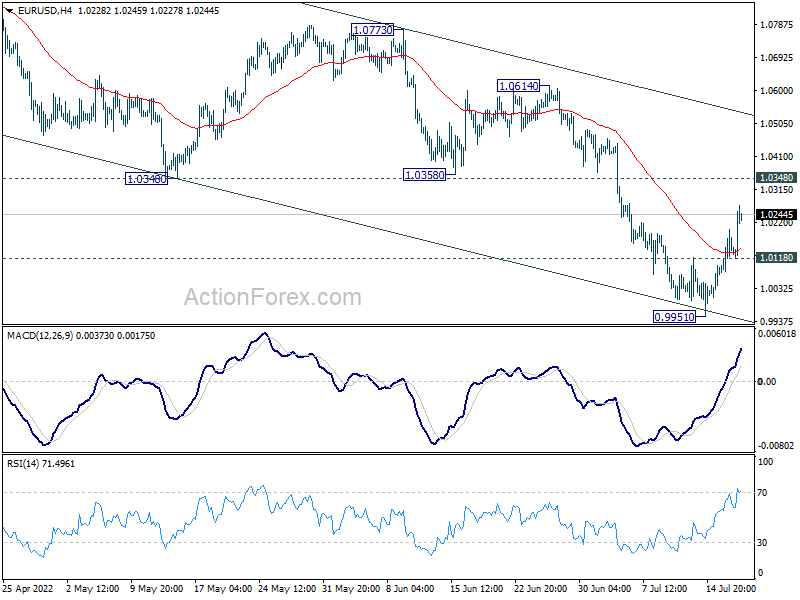

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0082; (P) 1.0141; (R1) 1.0204; More…

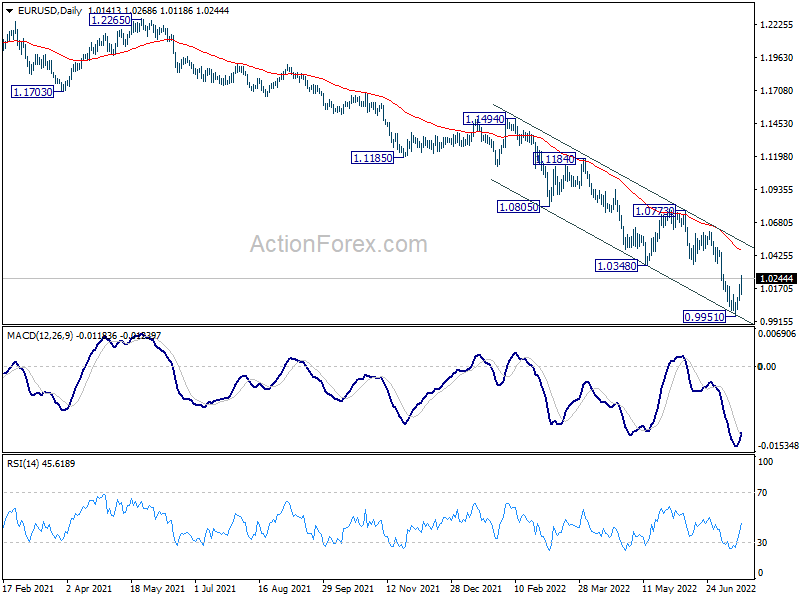

EUR/USD’s rebound from 0.9951 is still in progress and intraday bias stays on the upside for 1.0348 support turned resistance. Break there will target channel resistance at 1.0514. On the downside, below 1.0118 minor support will bring retest of 0.9951 low instead.

{kind=link}

In the bigger picture, down trend from 1.6039 (2008 high) is still in progress. Next target is 100% projection of 1.3993 to 1.0339 from 1.2348 at 0.8694. In any case, outlook will stay bearish as long as 1.0773 resistance holds, in case of rebound.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 06:00 | CHF | Trade Balance (CHF) Jun | 3.80B | 3.05B | 3.12B | |

| 06:00 | GBP | Claimant Count Change Jun | -20.0K | -41.2K | -19.7K | -34.7K |

| 06:00 | GBP | ILO Unemployment Rate (3M) May | 3.80% | 3.80% | 3.80% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y May | 6.20% | 6.80% | 6.80% | |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y May | 4.30% | 4.30% | 4.20% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | 8.60% | 8.60% | 8.60% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun F | 3.70% | 3.70% | 3.70% | |

| 12:30 | USD | Housing Starts Jun | 1.56M | 1.60M | 1.55M | 1.59M |

| 12:30 | USD | Building Permits Jun | 1.69M | 1.69M | 1.70M |