Sterling is in recovery today, and it’s supported by better than expected monthly GDP data. Yen is currently the softer one. But overall trading is quiet in the currency markets. RBNZ’s rate hike doesn’t give any lift to Kiwi. Canadian Dollar is range bound, awaiting BoC rate decision. Meanwhile, Dollar is consolidating recent gains, awaiting US CPI data.

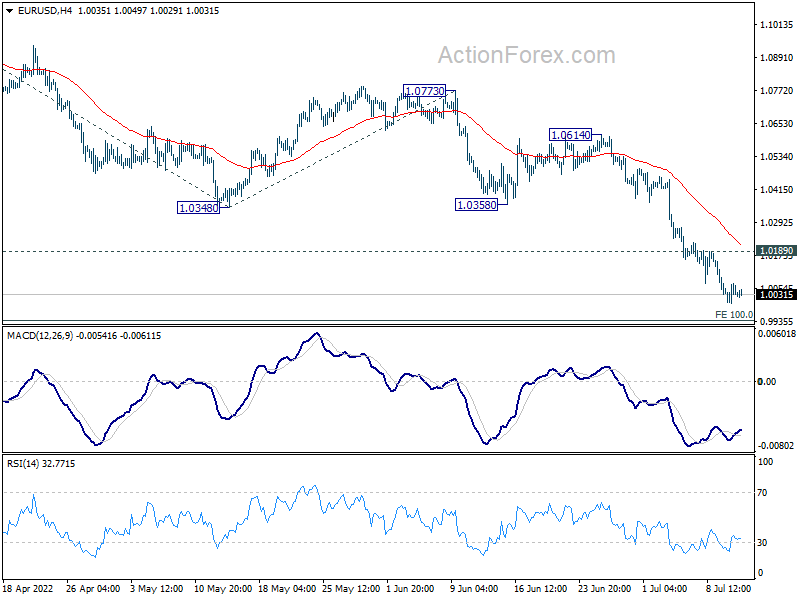

Technically, Dollar is losing some upside momentum, but there is no clear sign of topping yet. Near term levels to monitor include 1.0189 minor resistance in EUR/USD, 1.2055 minor resistance in GBP/USD, 0.6873 minor resistance in AUD/USD, 0.9721 minor support in USD/CHF, 134.74 minor support in USD/JPY. Buying dips in Dollar is still the way to go as long as these levels hold.

{kind=link}

In Asia, Nikkei rose 0.48%. Hong Kong HSI is up 0.03%. China Shanghai SSE is up 0.07%. Singapore Strait Times is down -0.67%. Japan 10-year JGB yield is down -0.0049 at 0.239. Overnight, DOW dropped -0.62%. S&P 500 dropped -0.92%. NASDAQ dropped -0.95%. 10-year yield dropped -0.033 to 2.958.

UK GDP grew 0.5% mom in May, much better than expectations

UK GDP grew 0.5% mom in May, much better than expectation of 0.0%. Services rose 0.4% mom. Production rose 0.9% mom. Construction also rose 1.5% mom. Monthly GDP is estimated to be 1.7% above its pre-pandemic levels in February 2020. In the three months to May, GDP grew 0.4%. Annual growth in monthly GDP was 3.5% yoy.

Also published, industrial production was up 0.9% mom, 1.4% yoy, versus expectation of 0.0% mom, 1.7% yoy. Manufacturing production was up 1.4% mom, 2.3% yoy, versus expectation of 0.1% mom, 0.3% yoy. Goods trade deficit was little changed at GBP -21.4B, versus expectation of GBP -18.3B.

RBNZ lifts OCR by 50bps to 2.5%, maintains approach of brisk rate hikes

RBNZ raised Official Cash Rate by 50bps to 2.50% as widely expected. The central bank also indicated that it will follow the projected path to raise interest to nearing 3.5% by the end of 2022, and then around 4% in mid-2023.

“The Committee is comfortable that the projected path of the OCR outlined in the recent May Monetary Policy Statement remains broadly consistent with achieving its primary inflation and employment objectives – without causing unnecessary instability in output, interest rates and the exchange rate,” RBNZ said in the statement.

Also, as noted in the summary records of meeting, “The Committee agreed to maintain its approach of briskly lifting the OCR until it is confident that monetary conditions are sufficient to constrain inflation expectations and bring consumer price inflation to within the target range.”

Fed Barkin expects inflation to come down, but not immediately, not suddenly, and not predictably

Richmond Fed President Thomas Barkin said yesterday, “I definitely see signs of softening” in the economy, with evidence “most pronounced in lower income households”.

“I expect inflation to come down but not immediately, not suddenly, and not predictably,” he said. “My expectations are it will be a slower path rather than an immediate path down to 2%.”

Barkin also said he’s open to a 50bps or 75bps hike in July. “I am one of the guys who like the option value of deciding the week of the meeting as opposed to two weeks before the meeting. But I thought Jay’s (Fed Chair Jerome Powell) guidance the last time was very sound,” he added.

IMF projects US inflation to slow to 1.9% by end of 2023

IMF cut US 2022 GDP growth forecasts from 2.9% to 2.3% in the latest report. For 2023, GDP growth was was also lowered from 1.7% to 1.0%. Inflation is forecast to come down to 6.6% in Q4 2022, then slow further to 1.9% by Q4 2023.

IMF Managing Director Kristalina Georgieva said: “In sum, we are confident the Fed will be effective in bringing inflation down, will remain data dependent and, as conditions change, will telegraph clearly where policy is likely to go. This is important not just for the U.S. but also for the global economy.

Looking ahead

Eurozone industrial production will be released today. But major focuses will firstly be on US CPI. Then, BoC is expected to raise interest rate again, probably by a jumbo 75bps. Fed will also publish Beige Book economic report.

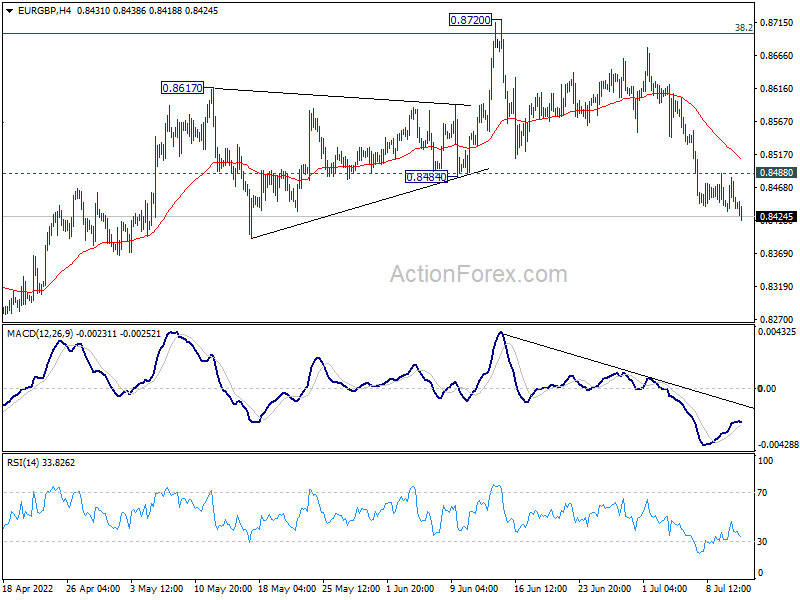

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8423; (P) 0.8453; (R1) 0.8474; More…

EUR/GBP’s decline is continuing today and intraday bias remains on the downside. Rebound from 0.8201 should have completed at 0.8720, after rejection by 0.8697 medium term fibonacci level. Further fall would be seen to retest 0.8201/48 support zone next. On the upside, above 0.8488 minor resistance will turn intraday bias neutral first.

{kind=link}

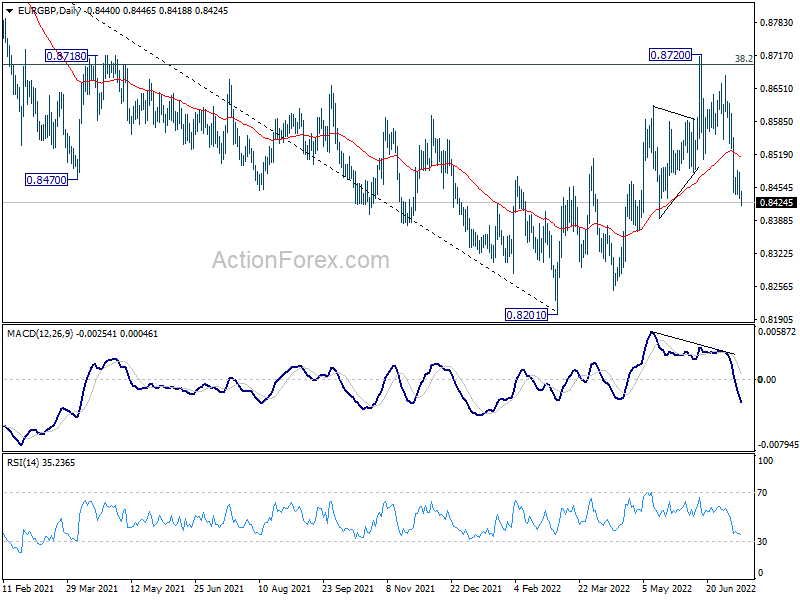

In the bigger picture, rejection by 38.2% retracement of 0.9499 to 0.8201 at 0.8697 argues that rebound from 0.8201 is merely a corrective move. That is, down trend from 0.9499 (2020 high) is now over. Sustained break of 0.8201 will resume such decline and target 61.8% retracement of 0.6935 to 0.9499 at 0.7917. This will now remain the favored case as long as 0.8720 resistance holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 02:00 | NZD | RBNZ Interest Rate Decision | 2.50% | 2.50% | 2.00% | |

| 06:00 | GBP | GDP M/M May | 0.50% | 0.00% | -0.30% | |

| 06:00 | GBP | Index of Services 3M/3M May | 0.10% | 0.20% | 0.00% | 0.20% |

| 06:00 | GBP | Industrial Production M/M May | 0.90% | 0.00% | -0.60% | -0.10% |

| 06:00 | GBP | Industrial Production Y/Y May | 1.40% | 1.70% | 0.70% | 1.60% |

| 06:00 | GBP | Manufacturing Production M/M May | 1.40% | 0.10% | -1.00% | -0.60% |

| 06:00 | GBP | Manufacturing Production Y/Y May | 2.30% | 0.30% | 0.50% | 1.30% |

| 06:00 | GBP | Goods Trade Balance (GBP) May | -21.4B | -18.3B | -20.9B | -21.5B |

| 06:00 | EUR | Germany CPI M/M Jun F | 0.10% | 0.10% | 0.10% | |

| 06:00 | EUR | Germany CPI Y/Y Jun F | 7.60% | 7.60% | 7.60% | |

| 09:00 | EUR | Eurozone Industrial Production M/M May | 0.20% | 0.40% | ||

| 11:00 | GBP | NIESR GDP Estimate (3M) Jun | -0.10% | |||

| 12:30 | USD | CPI M/M Jun | 1.00% | 1.00% | ||

| 12:30 | USD | CPI Y/Y Jun | 8.70% | 8.60% | ||

| 12:30 | USD | CPI Core M/M Jun | 0.50% | 0.60% | ||

| 12:30 | USD | CPI Core Y/Y Jun | 5.70% | 6.00% | ||

| 14:00 | CAD | BoC Interest Rate Decision | 2.00% | 1.50% | ||

| 14:30 | USD | Crude Oil Inventories | -1.5M | 8.2M | ||

| 18:00 | USD | Fed’s Beige Book |