Swiss Franc continues to rise broadly today, with additional help from selloff in Euro. The common currency is weighed down by Germany CPI, which unexpectedly slowed in June. But for now, Aussie, Sterling and Yen are even weaker than Euro. On the other hand, Canadian Dollar is second strongest as supported by rebound in oil prices, while Dollar is third.

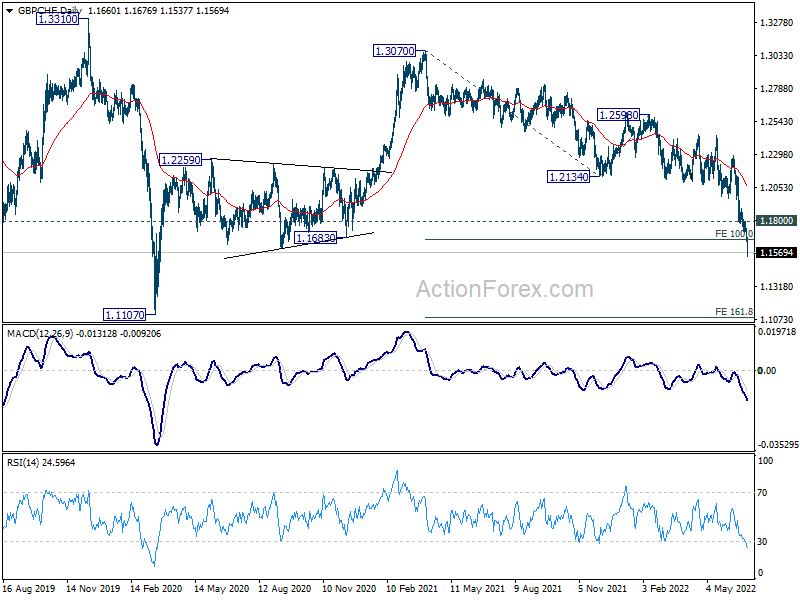

Technically, GBP/CHF’s falls through 100% projection 1.3070 to 1.2134 from 1.2598 at 1662 and there is no sign of bottoming yet. Outlook will remain bearish as long as 1.1800 resistance holds, for 161.8% projection at 1.1084, which is close to 202 low at 1.1107. The decline in GBP/CHF could accelerate further if EUR/CHF takes out 0.9970 low with some power.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.15%. DAX is down -1.58%. CAC is down -1.08%. Germany 10-year yield is down -0.0039 at 1.590. Earlier in Asia, Nikkei dropped -0.91%. Hong Kong HSI dropped -1.88%. China Shanghai SSE dropped -1.40%. Singapore Strait Times dropped -0.17%. Japan 10-year JGB yield dropped -0.0016 to 0.232.

Fed Mester: Getting interest rates up to 3-3.5% expeditiously is really important

Cleveland Fed President Loretta Mester told CNBC today, “if conditions were exactly the way they were today going into that meeting (in July) — if the meeting were today — I would be advocating for 75 because I haven’t seen the kind of numbers on the inflation side that I need to see in order to think that we can go back to a 50 increase.”

“I think getting interest rates up to that 3-3.5%, it’s really important that we do that, and do it expeditiously and do it consistently as we go forward, so it’s after that point where I think there is more uncertainty about how far we’ll need to go in order to rein in inflation,” she said.

“At the Fed, we’re on a path now to bring our interest rates up to a more normal level and then probably a little bit higher into restrictive territory, so that we can get those inflation rates down so that we can sustain a good economy going forward,” she said. “Job one for us now is to get inflation rates under control, and I think right now that’s coloring how consumers are feeling about the economy and where it’s going.”

Released from the US, Q1 GDP contraction was finalized at -1.6%.

ECB Simkus: We should move decisively toward monetary-policy normalization

ECB Governing Council member Gediminas Simkus said that by July meeting, “should see some change in the data, some change in relation to what we have seen at the beginning of June”. He added, “if we see this change in data that points to the persistence of inflation, to its acceleration, 50 basis points should be a policy option for July.”

“With these levels of inflation and inflation being more and more broad-based, with wages growing in the euro area, we should move decisively toward monetary-policy normalization,” said Simkus,

ECB has pre-committed to a 25bps rate hike in July. Another hike is also pre-committed for September, but the size would be dependent on incoming data.

Eurozone economic sentiment dropped to 104 in Jun, EU down to 102.5

Eurozone Economic Sentiment Indicator dropped from 105.0 to 104.0 in June. Employment Expectation Indicator dropped from 112.6 to 110.9. Economic Uncertainty Indicator rose from 23.4 to 24.8. Industry confidence rose from 6.5 to 7.4. Services confidence rose from 14.1 to 14.8. Consumer confidence dropped from -21.2 to -23.6. Retail trade confidence dropped from -4.2 to -5.1. Construction confidence dropped from 6.3 to 3.7.

EU Economic Sentiment Indicator dropped from 104.2 to 102.5. Employment Expectation Indicator dropped from 112.2 to 110.6. Economic Uncertainty Indicator rose from 22.6 to 23.9. The ESI fell across the six largest EU economies: confidence dropped most markedly in the Netherlands (-3.6), but also in Germany (-1.9), Spain (-1.9), Poland (-1.5), France (-1.0) and Italy (-1.0).

From Germany, CPI slowed from 7.9% yoy to 7.6% yoy in June, below expectation of 7.9% yoy.

BoJ Kuroda: Japan not much affected by global inflationary trend

BoJ Governor Haruhiko Kuroda said, “Unlike other economies, the Japanese economy has not been much affected by the global inflationary trend, so monetary policy will continue to be accommodative,” according to the recording released by the Bank for International Settlements (BIS).

After 15 years of deflation that lasted through 2013, businesses have be “very cautious” in raising prices and wages. “The economy recovered and companies recorded high profits. The labour market became quite tight. But wages didn’t increase much and prices didn’t increase much,” he added.

Also released, Japan retail sales rose 3.6% yoy in May, below expectation of 4.0% yoy. On seasonally adjusted basis, sales rose 0.6% mom.

Australia retail sales rose 0.9% mom in May, higher prices added to growth

Australia retail sales rose 0.9% mom in May, above expectation of 0.4% mom. That’s the fifth consecutive monthly growth.

Ben Dorber, Director of Quarterly Economy Wide Statistics said, “There was growth across five of the six retail industries in May as spending remained resilient. Higher prices added to the growth in retail turnover in May. This was most evident in cafes, restaurants and takeaway food services and food retailing.”

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0042; (P) 1.0086; (R1) 1.0117; More….

EUR/CHF’s fall continues today and breaches parity to as low as 0.9990 so far. Intraday bias stays on the downside for retesting 0.9970 low. Decisive break there will resume larger down trend. Next target is 0.9650 long term projection level. On the upside, however, above 1.0214 minor resistance will delay the bearish case, and turn bias back to the upside for stronger rebound.

{kind=link}

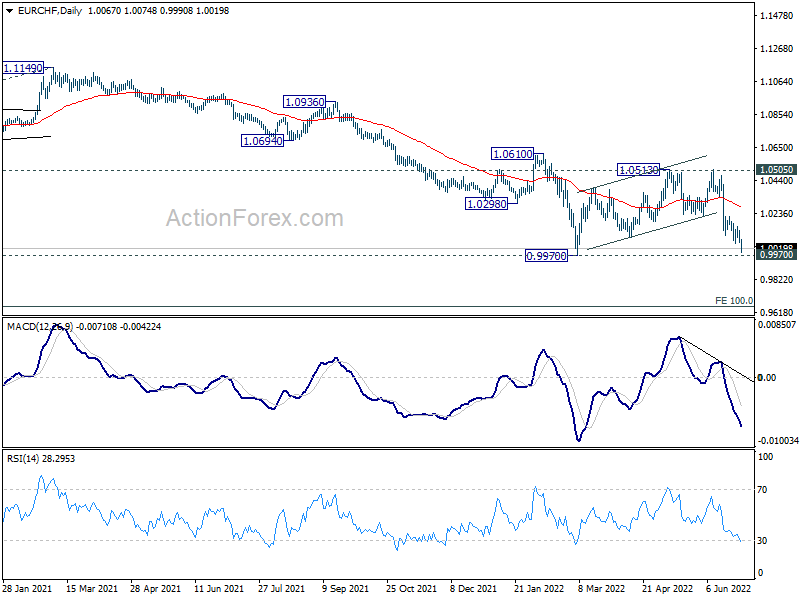

In the bigger picture, as long as 1.0505 support turned resistance (2020 low) holds, long term down trend from 1.2004 (2018 high) is expected to continue. Next target is 100% projection of 1.2004 to 1.0505 to 1.1149 at 0.9650. However, firm break of 1.0505 will suggest medium term bottoming, and bring stronger rebound towards 1.1149 structural resistance.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y May | 3.60% | 4.00% | 3.10% | |

| 01:30 | AUD | Retail Sales M/M May | 0.90% | 0.40% | 0.90% | |

| 08:00 | CHF | Credit Suisse Economic Expectations Jun | -72.7 | -52.6 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y May | 5.60% | 6.10% | 6.00% | 6.10% |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jun | 104 | 103 | 105 | |

| 09:00 | EUR | Eurozone Services Sentiment Jun | 14.8 | 12.7 | 14 | 14.1 |

| 09:00 | EUR | Eurozone Industrial Confidence Jun | 7.4 | 4.7 | 6.3 | 6.5 |

| 09:00 | EUR | Eurozone Consumer Confidence Jun F | -23.6 | -23.6 | -23.6 | |

| 12:00 | EUR | Germany CPI M/M Jun P | 0.10% | 0.30% | 0.90% | |

| 12:00 | EUR | Germany CPI Y/Y Jun P | 7.60% | 7.90% | 7.90% | |

| 12:30 | USD | GDP Annualized Q1 F | -1.60% | -1.50% | -1.50% | |

| 12:30 | USD | GDP Price Index Q1 F | 8.20% | 8.10% | 8.10% | |

| 14:30 | USD | Crude Oil Inventories |