Euro falls broadly today after worse than expectation PMI data. Aussie and Loonie are also weak as commodity prices pull back. On the other hand, Yen and Swiss Franc are rebounding, following the rather deep pull back in US and European benchmark yields. Stock markets are mixed with European indexes trading in red, but US markets open slightly higher.

Technically, EUR/JPY’s break of 141.93 minor support suggest rejection by 144.23 resistance, and deeper retreat could be seen. Similarly, USD/JPY and GBP/JPY could also head lower for the near term,, if treasury yields extend pull back. But for now, there is no clear sign of trend reversal, and Yen crosses should resume rally sooner rather than later.

In Europe, at the time of writing, FTSE is down -0.45%. DAX is down -1.16%. CAC is down -0.25%. Germany 10-year yield is down -0.205 at 1.435. Earlier in Asia, Nikkei rose 0.08%. Hong Kong HSI rose 1.26%. China Shanghai SSE rose 1.62%. Singapore Strait Times dropped -0.02%. Japan 10-year JGB yield dropped -0.0053 to 0.236.

US initial jobless claims dropped slightly to 229k

US initial jobless claims dropped -2k to 229k in the week ending June 18, matched expectations. Four-week moving average of initial claims rose 4.5k to 223.5k.

Continuing claims rose 5k to 1315k in the week ending June 11. Four-week moving average of continuing claims dropped -7k to 1310k, lowest since January 3, 1970.

UK PMI composite unchanged at 53.1, troubling combination of recession and inflation into H2

UK PMI Manufacturing dropped from 54.6 to 53.4 in June, below expectation of 53.8. That’s the lowest level in 23 months. PMI Services was unchanged at 53.4, above expectation of 53.0. PMI Composite was unchanged at 53.1.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “The weakness of the broad flow of economic data so far in the second quarter points to a drop in GDP which the forward-looking PMI numbers suggest will gather momentum in the third quarter. While there are some signs that the inflation could soon peak, the survey data suggest the rate of inflation will meanwhile remain historically high for some time to come, indicating that the UK looks set for a troubling combination of recession and elevated inflation as we move into the second half of the year.”

Eurozone PMI composite dropped to 16-mth low, just 0.2% GDP growth and worse to come

Eurozone PMI Manufacturing dropped from 54.6 to 52.0 in June, below expectation of 53.0. That’s the lowest level in 22 months. PMI Services dropped from 56.1 to 52.8, below expectation of 55.5, a 5-month low. PMI Composite dropped from 54.8 to 51.9, lowest in 16-months.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said: “Eurozone economic growth is showing signs of faltering … Excluding pandemic lockdown months, June’s slowdown was the most abrupt recorded by the survey since the height of the global financial crisis in November 2008…. The slowdown means the latest data signal a rate of GDP growth of just 0.2% at the end of the second quarter, down sharply from 0.6% at the end of the first quarter, with worse likely to come in the second half of the year.”

France PMI Manufacturing dropped sharply from 54.6 to 51.0 in June, well below expectation of 53.8. That’s the lowest level in 19 months. PMI Services dropped from 58.3 to 54.4, below expectation of 57.5, lowest in 5 months. PMI Composite dropped from 57.0 to 52.8, also a 5-month low.

Germany PMI Manufacturing dropped from 54.8 to 52.0 in June, below expectation of 54.0. That’s the lowest level in 23 months. PMI Services dropped from 55.0 to 52.4, below expectation of 54.5, a 5-month low. PMI Composite dropped from 53.7 to 51.3, a 6-month low.

Australia PMI composite dropped to 52.6, downside risks have increased

Australia PMI Manufacturing ticked up from 55.7 to 55.8 in June. PMI Services, on the other hand, dropped from 53.2 to 52.6. PMI Composite dropped from 52.9 to 52.6, a 5-month low.

Japan PMI manufacturing dropped to 52.7, but services jumped to 54.2

Japan PMI Manufacturing dropped slightly from 53.3 to 52.7 in June, below expectation of 54.4. PMI Services rose from 52.6 to 54.2, highest since October 2013. PMI Composite Output rose form 52.3 to 53.2.

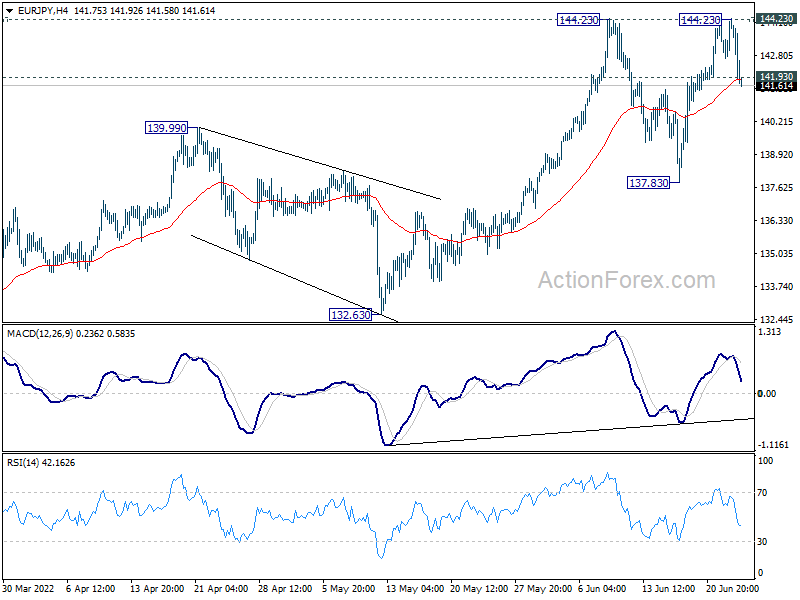

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.00; (P) 143.63; (R1) 144.57; More….

Intraday bias in EUR/JPY is back on the downside with break of 141.93 minor support. Current fall is viewed as the third leg of the consolidation from 144.23. Deeper decline could be seen to 137.83 support. On the upside, decisive break of 144.23 will resume larger up trend.

{kind=link}

In the bigger picture, up trend from 114.42 (2020 low) is in progress. Such rise is seen as the third leg of the pattern from 109.30 (2016 low). Sustained trading above 100% projection of 114.42 to 134.11 from 124.37 at 144.06 will indicate upside acceleration and target 149.76 long term resistance (2014 high). In any case, outlook will now remain bullish as long as 132.63 support holds, in case of deep pull back.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Jun P | 55.8 | 55.7 | ||

| 22:00 | AUD | Services PMI Jun P | 52.6 | 53.2 | ||

| 00:30 | JPY | Manufacturing PMI Jun P | 52.7 | 54.4 | 53.3 | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) May | 13.2B | 11.6B | 17.8B | 21.1B |

| 07:15 | EUR | France Manufacturing PMI Jun P | 51 | 53.8 | 54.6 | |

| 07:15 | EUR | France Services PMI Jun P | 54.4 | 57.5 | 58.3 | |

| 07:30 | EUR | Germany Manufacturing PMI Jun P | 52 | 54 | 54.8 | |

| 07:30 | EUR | Germany Services PMI Jun P | 52.4 | 54.5 | 55 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | 52 | 53.9 | 54.6 | |

| 08:00 | EUR | Eurozone Services PMI Jun P | 52.8 | 55.5 | 56.1 | |

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 08:30 | GBP | Manufacturing PMI Jun P | 53.4 | 53.8 | 54.6 | |

| 08:30 | GBP | Services PMI Jun P | 53.4 | 53 | 53.4 | |

| 12:30 | USD | Current Account (USD) Q1 | -291B | -275B | -218B | -225B |

| 12:30 | USD | Initial Jobless Claims (Jun 17) | 229K | 229K | 229K | 231K |

| 13:45 | USD | Manufacturing PMI Jun P | 56.4 | 57 | ||

| 13:45 | USD | Services PMI Jun P | 53.5 | 53.4 | ||

| 14:30 | USD | Natural Gas Storage | 63B | 92B |