The forex markets are steady in tight range in Asia, while Dollar remains the strongest one for the week. Main focus today is on whether Fed would deliver a 75bps hike as markets fully priced in, or stick to its “original plan” of 50bps hike per meeting. Yen is staying as the second strongest on risk aversion while Euro is third. Sterling remains the worst performing, followed by other commodity currencies.

Technically, it should be pointed out that Dollar has yet to take out near term resistance level against most major currencies. The levels include 1.0348 in EUR/USD, 0.6828 support in AUD/USD, 1.0063 resistance in USD/CHF and 1.3075 resistance in USD/CAD. These are the levels for the greenback to overcome.

In Asia, at the time of writing, Nikkei is down -0.83%. Hong Kong HSI is up 1.42%. Chinas Shanghai SSE is up 1.41%. Singapore Strait Times is up 0.62%. Japan 10-year JGB yield is up 0.019 at 0.275, after touching 0.3 briefly. Overnight, DOW dropped -0.50%. S&P 500 dropped -0.38%. NASDAQ rose 0.18%. 10-year yield rose 0.117 to 3.483.

Australia Westpac consumer sentiment dropped to 86.5, on inflation and interest rate

Australia Westpac Consumer Sentiment dropped from 90.4 to 86.5 in June. Over the 46-year history of the survey, the reading was only at or below this level during “major economic dislocations”, including during COVID-19, the Global Financial Crisis, early 90s recession, mid-80s slowdown and early 80s recession.

Westpac said: “The survey detail shows a clear picture of a slump in sentiment being driven by rising inflation; an associated lift in interest rates; and a loss of confidence around the economic outlook, both here and abroad.”

Regarding RBA policy, Westpac expects another 50bps rate hike in July, as the central bank needs to move quickly in the early stages in a tightening cycle when interest rates are clearly below neutral and risk of over-tightening is moderate.

China industrial production rose 0.7% yoy in May, retail sales down -6.7% yoy

China industrial production rose 0.7% yoy in May, much better than expectation of -1.0% yoy decline. Retail sales dropped -6.7% yoy, above expectation of -7.3% yoy. Fixed asset investment rose 6.2% ytd yoy, above expectation of 6.0%.

The National Bureau of Statistics said the economy “showed a good momentum of recovery” in the month, “with negative effects from Covid-19 pandemic gradually overcome and major indicators improved marginally.”

Still, it warned, “we must be aware that the international environment is to be even more complicated and grim, and the domestic economy is still facing difficulties and challenges for recovery.”

Fed to hike by 75bps? 10-year yield heading to 4%?

FOMC rate decision is the major focus today. Just before last Friday, markets have well received Fed’s communication on the 50bps hike per meeting “plan”. But it’s another world now after data showed CPI inflation reaccelerated in May. Fed fund futures are pricing in near 100% change of a 75bps rate hike at this meeting. The question now is what Fed is going to deliver.

The new economic projections will also be closely watched too. The stubborn inflation reading should be reflected in the new forecasts, as well as it’s impact on growth and employment. More importantly, the dot plot will again catch most attention. Back in March, only 7 of 16 FOMC member penciled in interest rate above 2% by the end of 2022. The balance would likely shift further to the hawks’ side. But by how far?

Some suggested readings on FOMC:

The strong rally, with acceleration in 10-year yield this week is a big surprise. 2018 high at 3.248 was taken out with ease and it’s now close to 161.8% projection of 0.398 to 1.765 from 1.343 at 3.554. Break of 3.167 resistance turned support is needed to signal short term topping, or any retreat should be relatively brief. Sustained break of 3.554 will pave the way to 200% projection at 4.077, which is close to 4% handle.

{kind=link}

{kind=link}

{kind=link}

Looking ahead

Swiss PPI and SECO economic forecasts will be released in European session. Eurozone will release trade balance and industrial production.

US will release retail sales, Empire State manufacturing index, import price business inventories and NAHB housing index. But major focus is on FOMC rate decision and economic projections.

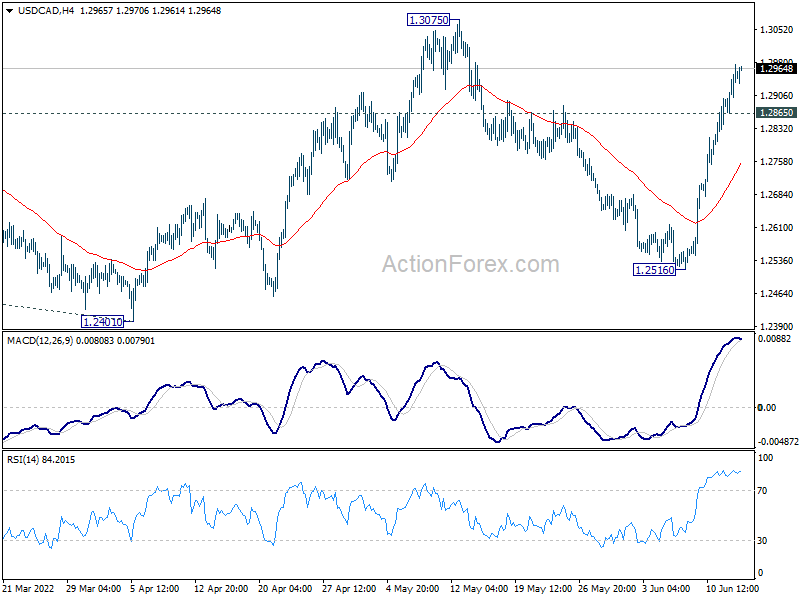

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2890; (P) 1.2932; (R1) 1.2999; More…

Intraday bias in USD/CAD remains on the upside for 1.3075 resistance. Firm break there will resume medium term rally and sustained trading above 1.3022 fibonacci level will carry larger bullish implications. Next target is 100% projection of 1.2005 to 1.2947 from 1.2401 at 1.3343. On the downside, below 1.2865 minor support will delay the bullish case and turn bias neutral first.

{kind=link}

In the bigger picture, focus stays on 38.2% retracement of 1.4667 (2020 high) to 1.2005 (2021 low) at 1.3022. Sustained break there should confirm that the down trend from 1.4667 has completed after defending 1.2061 long term cluster support. Further rise would then be seen towards 61.8% retracement at 1.3650. However, rejection by 1.3022 will maintain medium term bearishness.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account (NZD) Q1 | -6.14B | -5.96B | -7.26B | -7.34B |

| 23:50 | JPY | Machinery Orders M/M Apr | 10.80% | -1.50% | 7.10% | |

| 00:30 | AUD | Westpac Consumer Confidence Jun | -4.50% | -5.60% | ||

| 02:00 | CNY | Industrial Production Y/Y May | 0.70% | -1.00% | -2.90% | |

| 02:00 | CNY | Retail Sales Y/Y May | -6.70% | -7.30% | -11.10% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y May | 6.20% | 6.00% | 6.80% | |

| 04:30 | JPY | Tertiary Industry Index M/M Apr | 0.70% | 0.80% | 1.30% | 1.70% |

| 06:30 | CHF | Producer and Import Prices M/M May | 0.60% | 1.30% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y May | 6.90% | 6.70% | ||

| 07:00 | CHF | SECO Economic Forecasts | ||||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Apr | -14.5B | -17.6B | ||

| 09:00 | EUR | Eurozone Industrial Production M/M Apr | 0.50% | -1.80% | ||

| 12:15 | CAD | Housing Starts s.a Y/Y May | 265K | 267K | ||

| 12:30 | USD | NY Empire State Manufacturing Index Jun | 5 | -11.6 | ||

| 12:30 | USD | Retail Sales M/M May | 0.20% | 0.90% | ||

| 12:30 | USD | Retail Sales ex Autos M/M May | 0.80% | 0.60% | ||

| 12:30 | USD | Import Price Index M/M May | 1.10% | 0.00% | ||

| 14:00 | USD | Business Inventories Apr | 1.20% | 2.00% | ||

| 14:00 | USD | NAHB Housing Market Index Jun | 68 | 69 | ||

| 14:30 | USD | Crude Oil Inventories | -2.3M | 2.0M | ||

| 18:00 | USD | Fed Interest Rate Decision | 1.50% | 1.00% | ||

| 18:30 | USD | FOMC Press Conference |