Worries of stagflation intensified a whole lot last week. In particular, even the habitually cautious ECB pre-committed to rate hikes in July and September, while delivering new economic forecasts with sharply higher inflation and lower growth projections. Selloff in risk markets accelerated further after US CPI re-accelerated to new 40-year high. The hope of inflation having peaked was dashed. Fed is more likely than not to continue with its plan of 50bps hike per meeting through September. Higher prices and rates will suppress consumer spending and eventually bite back the economy.

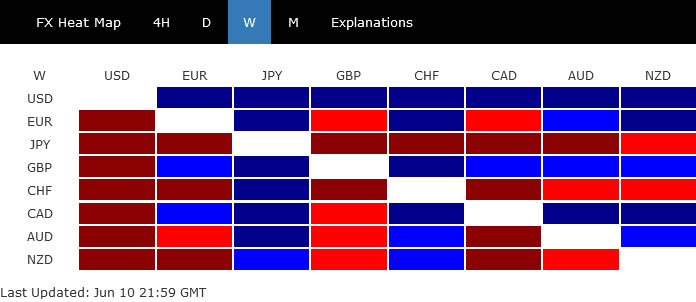

Dollar ended as the strongest one, as both supported by risk aversion and rising treasury yields. Yen was originally the run away loser, but it did come back to live on risk aversion on Friday. Swiss Franc was the second worst. Euro’s performance was disappointing given the more hawkish than expected ECB. Other mostly traded currencies were mixed against each other.

{kind=link}

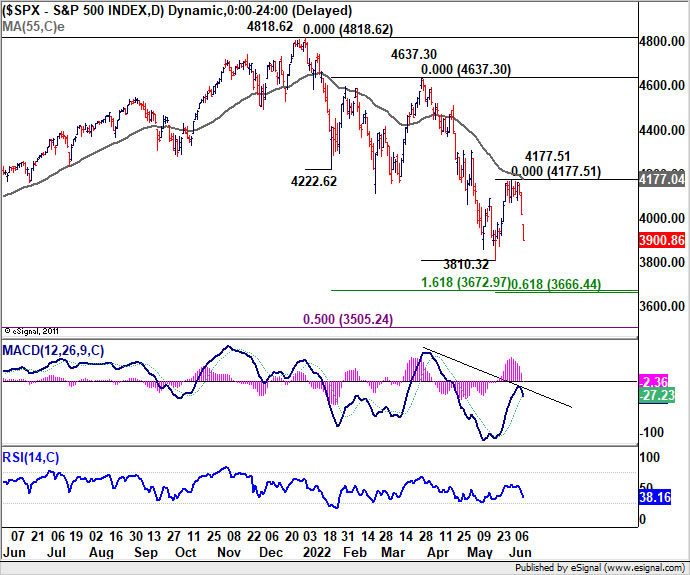

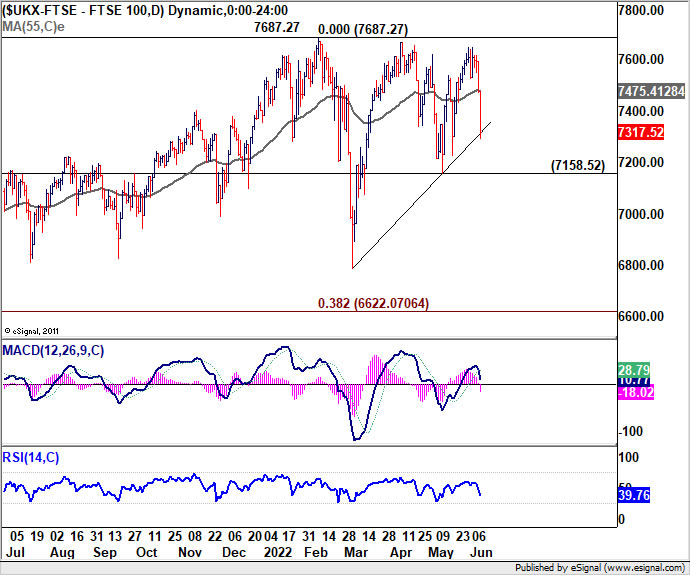

S&P 500, FTSE and DAX tumbled on stagflation fear

In the US, S&P 500’s fall started in Thursday, followed by a gap down on Friday and accelerated selloff. The development suggests that oversold bounce from 3810.32 has completed at 4177.41. Rejection by 55 day EMA keeps near term outlook bearish.

Whole corrective pattern from 4818.62 is still in progress and it’s likely started another falling leg through 3810.32 low. Strong support could be seen around 3666.44/3672.97 cluster projection level to finish the correction (61.8% projection of 4637.30 to 3810.32 from 4177.51 at 3666.44, 161.8% projection of 4818.62 to 4222.62 from 4637.30 at 3672.97).

However, firm break of 3666.44/3672.97 will bring even deeper correction into support zone between 3195.28 and 3505.24 (61.8% and 50% retracement of 2191.86 to 4818.62).

{kind=link}

{kind=link}

Over the Atlantic in the UK, FTSE’s price actions from 7687.27 are seen as a correction pattern to rise from 4898.79. It’s likely starting another falling leg. Break of 7158.52 support should send FTSE lower towards 38.2% retracement of 4898.79 to 7687.27 at 6622.07.

{kind=link}

{kind=link}

In Germany, DAX’s sharp decline suggests that it’s probably starting another falling leg in the correction from 16290.19. Rejection by 55 week EMA affirms this bearish case. Near term focus is on 13380.67 support. Firm break there will affirm this bearish case and target 12438.85 support, and probably further to 61.8% retracement of 8255.65 to 16290.19 at 11324.84.

{kind=link}

{kind=link}

US 10-year yield to taken on 2018 high as up trend resumes

German 10-year bund yield jumped to close at 1.52%, highest level since 2014. UK 10-year gilt yield also rose to 2.4475, highest since 2014 too. In the US, 10-year yield’s breach of 3.167 suggests that the medium term up trend is resuming. But it should be noted again that TNX is facing a key long term resistance level at 3.248 (2018 high), which could cap its upside. However, Sustained break of 3.248 would finally mark the end of the multi-decade down trend from 15.84 (1981 high). That would be a significant, era-defining development if happens.

{kind=link}

{kind=link}

Dollar index might be ready to resume long term up trend

Dollar index’s rebound from 101.29 extended higher last week. The strong support seen from 55 day EMA is a bullish sign. Current upside acceleration raising the chance of up trend resumption. Near term focus is back on 105.00 high. Rejection by 105.00 will extend the corrective pattern from there with another falling leg, probably with one more take on 55 day EMA.

However, sustained break of 105.00 will resume the long term up trend. Next target will be 61.8% projection of 72.69 (2011 low) to 103.82 (2017 high) from 89.20 (2021 low) at 108.43.

{kind=link}

{kind=link}

USD/JPY heading to 150? Or Japan will intervene?

Yen dropped to the lowest level against Dollar since 2001 last week. The selloff in Yen was originally broad based, but it managed to recover against most others on risk aversion on Friday. Widening yield gap will keep the Japanese currency pressured. But the question is whether current development is enough to trigger intervention by the government, or any action by BoJ.

In rare occasion, the Ministry of Finance, the Financial Services Agency, and BoJ issued a statement, expressing concerns. The statement noted that “we are worried about the rapid depreciation of the yen”. The government and BoJ will work to “closely monitor the trends” and their impact on the economy. Most importantly, it noted that based on G7 agreement, “excessive fluctuations and chaotic movements” can lead to “appropriate action if necessary.

Barring any special actions, including direct intervention by the MoF, or BoJ’s allowance for a wider band for 10-year JGB yield, USD/JPY’s rally is there to continue. As long as 126.35 support holds, current up trend should target 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 149.26, which is close to 147.68 (1998 high).

{kind=link}

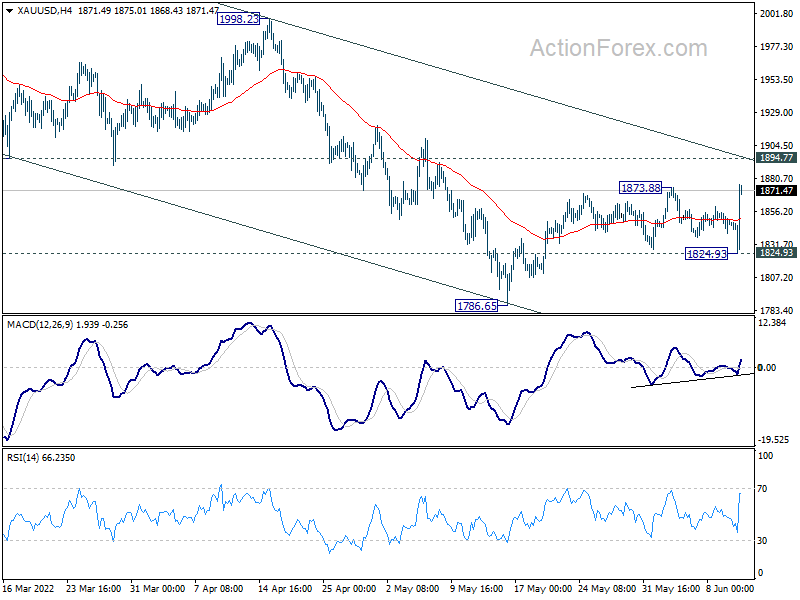

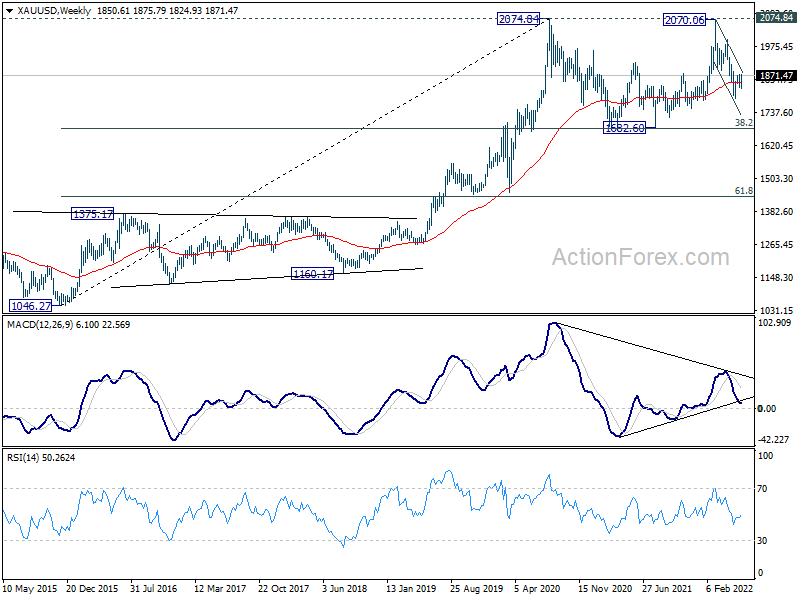

Gold’s main hurdle at 1900 despite impressive rebound

Gold’s reversal on Friday is impressive and worth a mention. It initially dived to 1824.93 after US CPI release, but then rebounded to close at 1871.47, after breaching 1873.88 resistance. An environment where global interest rates are on the way up should be unfavorable to Gold. Yet, it’s attracting some safe-haven flows (much less than Dollar), when funds are rushing out of treasuries and stocks.

Technically, there is upside potential for the near term. But key hurdle lies 1900 handle, which is close to 1894.77 support turned resistance and the near term falling channel resistance. Strong resistance could be seen from this handle to complete the corrective recovery from 1786.65.

Fall from 2070.06 is seen as the third leg of the whole corrective pattern from 2074.74 (2020 high), and there should be one more fall to go, towards 1682 60 support. Nevertheless, sustained break of 1900 will dampen this bearish case and could trigger some fierce buying back towards 2000.

{kind=link}

{kind=link}

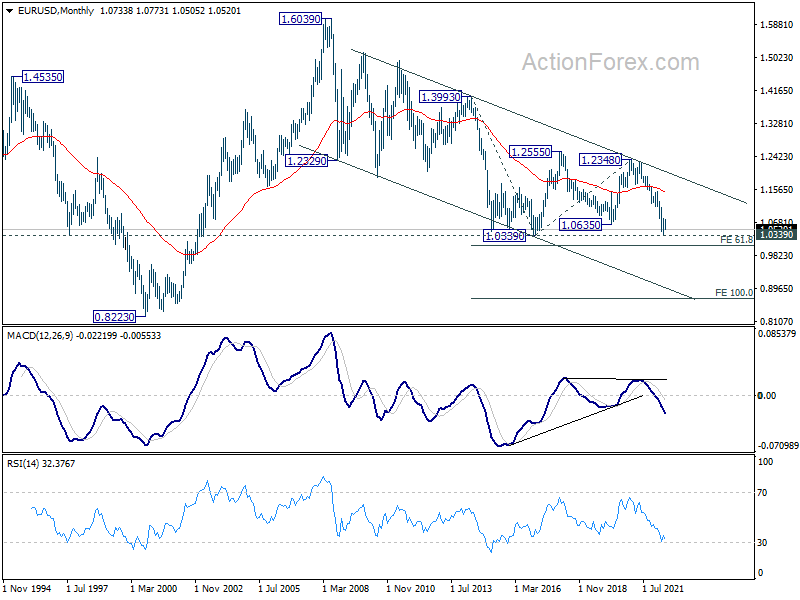

EUR/USD Weekly Outlook

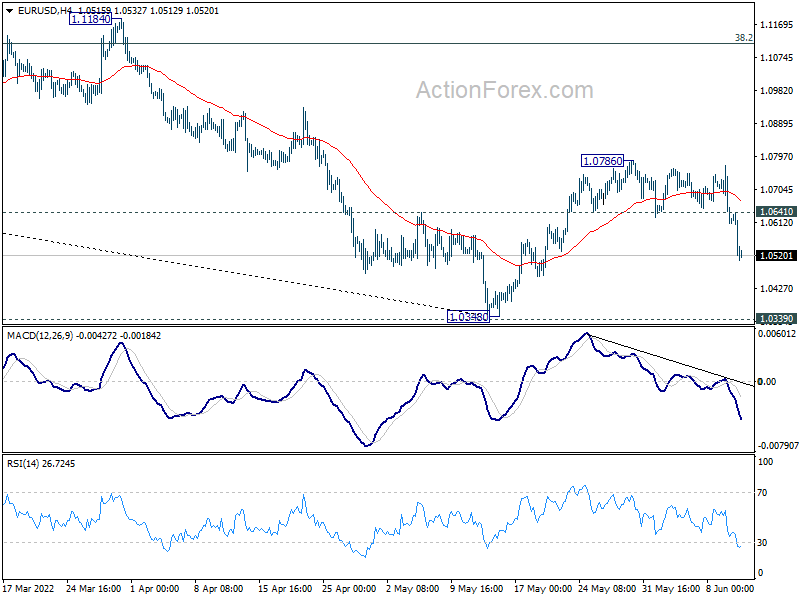

EUR/USD’s late decline last week suggests that corrective recovery from 1.0348 has completed at 1.0786, after rejection by 55 day EMA. Initial bias stays on the downside this week for retesting 1.0348 and 1.0339 long term support. Decisive break there will resume larger down trend. On the upside, above 1.0641 minor resistance will turn intraday bias neutral first.

{kind=link}

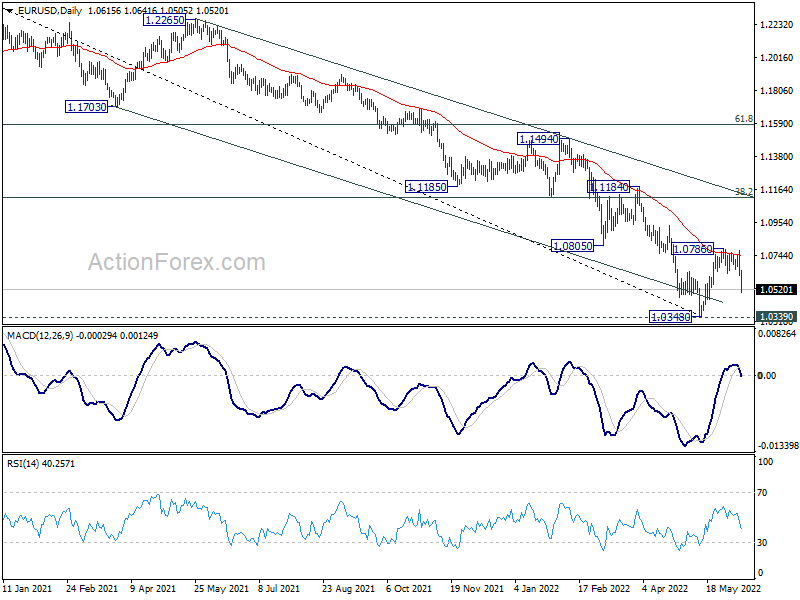

In the bigger picture, focus stays on 1.0339 long term support (2017 low). Decisive break there will resume whole down trend from 1.6039 (2008 high). Next target is 61.8% projection of 1.3993 to 1.0339 from 1.2348 at 1.0090. However, firm break of 1.0805 support turned resistance will delay this bearish case. Rise from 1.0348 is at least a correction to the down trend from 1.2348. Stronger rebound would be seen to 38.2% retracement of 1.2348 to 1.0348 at 1.1112.

{kind=link}

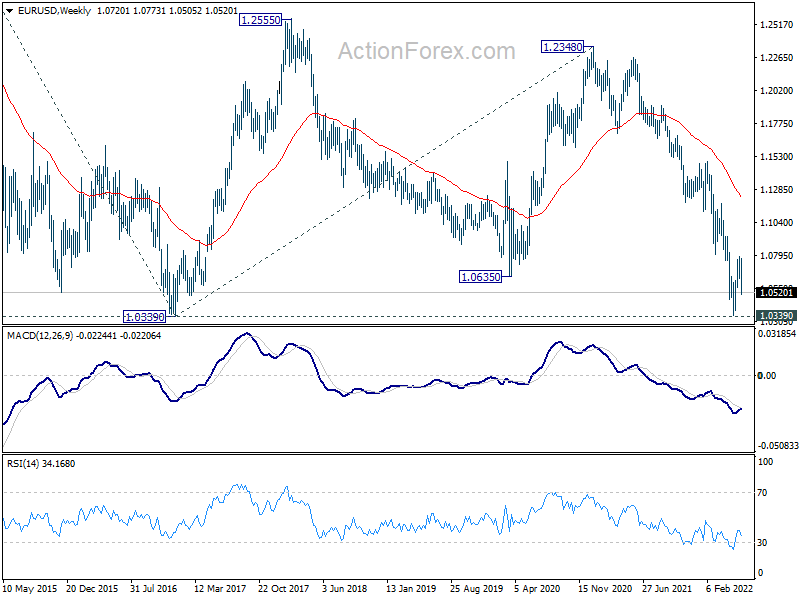

In the long term picture, current development suggests that long term down trend from 1.6039 (2008 high) is ready to resume. Break of 1.0339 will target 61.8% projection of 1.3993 to 1.0339 from 1.2348 at 1.0090. Decisive break there could bring downside acceleration towards 100% projection at 0.8694.

{kind=link}

{kind=link}