Inflation data were the main drivers in the forex markets in the past 12 hours. New Zealand Dollar turned slightly weaker after Q1 CPI came in lower than expected, despite surging to 30-year high. On the other hand, Canadian Dollar remains supported by the stronger than expected CPI readings released overnight. Dollar’s retreat appears to be relatively brief in general, as it’s regaining some ground against European majors. Yen also turned weaker in very tight range, as it’s now in consolidations.

For now, Loonie is the strongest one for the week, followed by Aussie and then Kiwi. Yen remains the worst, followed by Swiss Franc and then Sterling. Dollar and Euro are mixed.

Technically, EUR/CAD’s down trend resumed already by breaking through 1.3541 temporary low. GBP/CAD also breaks through 1.6292 temporary low too. At the same time, CAD/JPY is extending recent up trend and edged higher to 102.93. It’s on track to 61.8% projection of 89.21 to 100.17 from 98.17 at 104.94.

{kind=link}

In Asia, at the time of writing, Nikkei is up 1.05%. Hong Kong HSI is down -1.74%. China Shanghai SSE is down -1.60%. Singapore Strait Times is up 0.46%. Japan 10-year JGB yield is down -0.0004 at 0.254. Overnight, DOW rose 0.71%. S&P 500 dropped -0.06%. NASDAQ dropped -1.22%. 10-year yield dropped -0.073 to 2.840.

Fed Daly busy thinking about three things – inflation, inflation, inflation

San Francisco Fed President Mary Daly said yesterday that ” an expeditious march to neutral by the end of the year as a prudent path.” And it’s the “top priority” to move “purposefully to a more neutral stance that does not stimulate the economy”

“The case for a 50 basis-point adjustment is now complete,” she said after the speech. “The economy is resilient; it can handle these adjustments.” And, she’s “busy thinking about are three things: inflation, inflation, inflation.”

Nevertheless she also emphasized, ,”if we ease on the brakes by methodically removing accommodation and regularly assessing how much more is needed, we have a good chance of transitioning smoothly and gliding the economy to its long-run sustainable path,” she said.

As for the economy, she said, recession is one word, but it describes a whole range of outcomes. It can be a couple of quarters of a tiny bit below zero. That’s a very different beast than something like the financial crisis or the Volcker disinflation period.”

“That’s not something that I’m forecasting or something I think would derail the long-run expansion,” she added.

BoJ starts four day unlimited bond purchases to defend yield cap

BoJ announced yesterday another round of bond purchases to defend the 10-year JGB yield cap at 0.25%. It will carry out unlimited purchases through auctions on April 21, 22, 25, and 26, with 0.25% fixed-rate applied.

“Given recent yield movements on longer-ended notes, we have announced a consecutive unlimited fixed-rate purchase of bonds to achieve our policy to guide the 10-year yield around 0%,” the BoJ said in a statement.

Under the yield curve control framework, BoJ intends to keep 10-year JGB yield at 0%, with allowance to move up and down 0.25%.

IMF: Yen’s move driven by fundamentals

Sanjaya Panth, deputy director of the IMF’s Asia and Pacific Department, said Yen’s depreciation is “driven by fundamentals.

“Economic policymaking should continue to look at fundamentals. We don’t see any reason to change economic policy because what’s happening right now reflects fundamentals.”

“As you know, a weak yen hasn’t been bad for Japan,” Panth said. “At the same time, it does affect households. It’s a little bit of a mixed bag,”

“Japan is in a very different situation compared with other advanced countries who have begun tightening monetary policy,” he said. “We do not see any need to change the accommodative monetary policy stance.”

NZ CPI rose to 6.9% yoy in Q1, highest since 1990

New Zealand CPI rose 1.8% qoq in Q1, below expectation of 2.0% qoq. For the 12-month period, CPI accelerated from 5.9% yoy to 6.9% yoy, below expectation of 7.1% yoy. That’s nonetheless still the highest annual rate since June 1990 quarter.

StatsNZ said: “The main driver for the 6.9 percent annual inflation to the March 2022 quarter was the housing and household utilities group, influenced by rising prices for construction and rentals for housing.”

“Construction firms have been experiencing many supply-chain issues, higher labour costs, and also higher demand, which have pushed up the cost of building a new house,” senior prices manager Aaron Beck said.

Looking ahead

Eurozone CPI final is the main feature in European session. Later in the day, US will release jobless claims and Philly Fed survey.

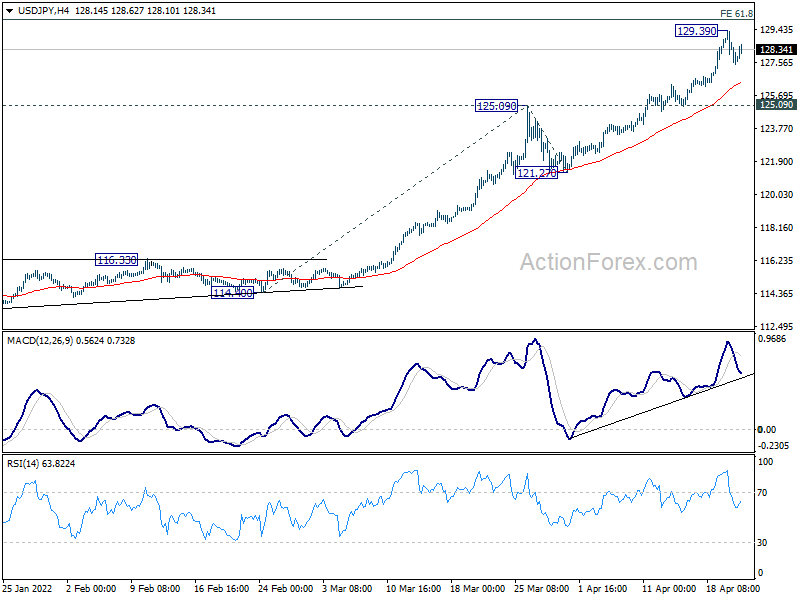

USD/JPY Daily Outlook

Daily Pivots: (S1) 127.09; (P) 128.24; (R1) 129.03; More…

Intraday bias in USD/JPY remains neutral for the moment. Consolidation from 129.39 temporary top is extending and deeper retreat cannot be ruled out. But downside should be contained above 125.09 resistance turned support to bring another rally. On the upside, above 129.39 will resume larger up trend to 130.04 long term projection level next.

{kind=link}

In the bigger picture, the break of 125.85 resistance (2015 high) suggests that whole up trend from 75.56 (2011 low) is resuming. Further rise should be seen to 61.8% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 130.04. Sustained break there wave the way to 147.68 (1998 high). For now, this will remain the favored case as long as 121.27 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q1 | 1.80% | 2.00% | 1.40% | |

| 22:45 | NZD | CPI Y/Y Q1 | 6.90% | 7.10% | 5.90% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Mar F | 3.00% | 3.00% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Mar F | 7.50% | 7.50% | ||

| 12:30 | USD | Initial Jobless Claims (Apr 15) | 177K | 185K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Apr | 20.9 | 27.4 | ||

| 14:00 | EUR | Eurozone Consumer Confidence Apr P | -20 | -19 | ||

| 14:30 | USD | Natural Gas Storage | 40B | 15B |