Euro is trading broadly lower today, as EU announces the fifth package of sanctions against Russia. As European Commission President Ursula von der Leyen said, “Russia is waging a cruel, ruthless war, also against Ukraine’s civilian population.” The sanctions include ban of Russia coals, access to EU ports and transaction banks of four key Russian banks. On the other hand, Australian Dollar remains the strongest one, as lifted by the hawkish twist in RBA statement.

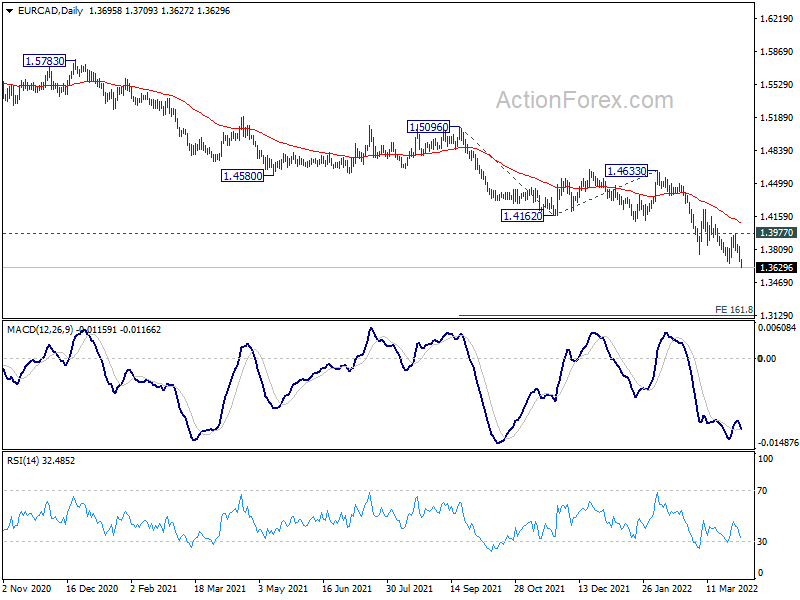

Technically, EUR/CAD’s down trend resumed by breaking through 1.3671 low. Outlook will stay bearish as long as 1.3977 resistance holds. Next target is 161.8% projection of 1.5096 to 1.4162 from 1.4633 at 1.3122. At the same time, break of 1.0943 support in EUR/USD, and 0.8294 support in EUR/GBP, will further solidify weakness in Euro.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.02%. DAX is down -0.57%. CAC is down -1.49%. Germany 10-year yield is up 0.075 at 0.580. Earlier in Asia, Nikkei rose 0.19%. Hong Kong HSI rose 2.10%. China was on holiday. Singapore Strait Times rose 0.82%. Japan 10-year JGB yield dropped -0.0055 to 0.211.

US trade deficit unchanged at US 89.2B in Feb

US exports of goods and services rose 1.8% to USD 228.6B in February. Imports of goods and services rose 1.3% to USD 317.8B. Trade deficit was relatively unchanged at USD 89.2B, larger than expectation of USD 88.5B.

Trade deficit with Mexico dropped USD 2.7B to USD 9.8B. Deficit with Japan dropped USD 2B to USD 5.1B. Deficit with China rose USD 7.9B to USD 41.2B.

Canada trade surplus narrowed to CAD 2.7B in Feb

Canada imports rose 3.9% to CAD 56.1B in February. Gains were observed in 9 of 11 import product sections. Exports rose 2.8% to CAD 58.7B, with increases in 8 of 11 products sections. Trade surplus narrowed from CAD 3.1B to CAD 2.7B, smaller than expectation of CAD 2.9B.

UK PMI services finalized at 62.6, second strongest since 1997

UK PMI Services was finalized at 62.6 in March, up from February’s 60.5. Rate of expansion was the second strongest since May 1997, exceeded only by the post-lockdown recovery in May 2021. PMI composite was finalized at 60.9, up from prior months 59.9, fastest expansion since June 2021.

Tim Moore, Economics Director at S&P Global: “UK economic growth continued to surge higher in March after an Omicron-induced slowdown at the turn of the year… However, the near-term growth outlook weakened in March, with optimism dropping to its lowest since October 2020 as the war in Ukraine and global inflation concerns took a considerable toll on business sentiment.

“Service providers experienced the second-fastest rise in business expenses since this index began in 1996, driven by higher wages, energy bills and fuel prices. Soaring costs meant that output charges were increased to the greatest extent for more than 25 years in March. Many survey respondents commented that the full extent of the recent spike in their operating costs had yet to be passed on to customers.”

Eurozone PMI composite finalized at 54.9, greater risk of economy stalling or contracting

Eurozone PMI Services was finalized at 55.6 in March, up from February 55.5, hitting a 4-month high. However, PMI Composite was finalized at 54.9, down from prior month’s 55.5.

Looking at some member states, Ireland PMI composite rose to 5-month high at 61.0. France rose to 8-month high at 56.3. But Germany dropped to 55.1. Spain dropped to 53.1. Italy dropped to 52.1. PMI composite of Germany, Spain and Italy were all at 2-month low.

Chris Williamson, Chief Business Economist at S&P Global said: “The further reopening of the eurozone economy amid the fading Omicron wave has provided a welcome tailwind to business activity in March… However, the resilience of the economy will be tested in the coming months by headwinds which include a further spike in energy costs and other commodity prices due to Russia’s invasion of Ukraine, as well as worsening supply chain issues arising from the war and a marked deterioration in business optimism regarding prospects for the year ahead…

“The outlook for growth has therefore deteriorated at a time when the inflation outlook has worsened. A recession is by no means assured, as the extent to which the economy could suffer in the coming months will depend on the duration of the war and any changes to both fiscal and monetary policy. It certainly seems likely however that the solid expansion seen in March will prove hard to sustain and there is clearly a greater risk of the economy stalling or contracting during the second quarter.”

RBA stands pat, drop the patient stance

RBA keeps cash rate unchanged at 0.10% today as widely expected. The central bank dropped the line that “the Board is prepared to be patient as it monitors how the various factors affecting inflation in Australia evolve.” It’s seen as a sign that RBA is preparing the markets for an earlier rate hike.

In the forward guidance, RBA said “the Board has wanted to see actual evidence that inflation is sustainably within the 2 to 3 per cent target range before it increases interest rates.”. While inflation has picked up and further increase is expected, “growth in labour costs has been below rates that are likely to be consistent with inflation being sustainably at target.”

RBA concluded, “over coming months, important additional evidence will be available to the Board on both inflation and the evolution of labour costs. The Board will assess this and other incoming information as its sets policy to support full employment in Australia and inflation outcomes consistent with the target.”

BoJ Kuroda: Recent Yen moves somewhat rapid

BoJ Governor Haruhiko Kuroda told the parliament today that recent moves in Yen exchange way have been “somewhat rapid”. He added, “it’s extremely important for currency rates to move stably reflecting economic and financial fundamentals.”

“We will patiently maintain powerful monetary easing to support an economy still in the midst of recovering from the COVID-19 pandemic’s impact,” he reiterated.

“If long-term interest rates rise rapidly, we are ready to deploy such market operations,” Kuroda said, referring to the intervention to cap 10-year JGB yield at 0.25%.

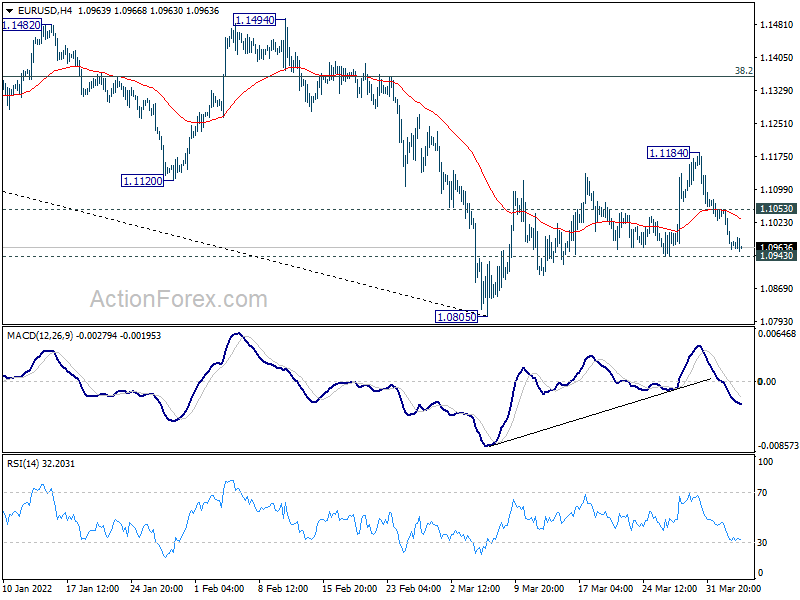

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0937; (P) 1.0996 (R1) 1.1031; More…

Intraday bias in EUR/USD remains neutral for the moment. Break of 1.0943 support will argue that rebound from 1.0805 has completed at 1.1184. Intraday bias will be back on the downside for retesting 1.0805 low. Further break of 1.0805 will resume larger down trend from 1.2348. On the upside, above 1.1053 minor resistance will revive near term bullishness, and turn bias back to the upside for 1.1184 resistance and above.

{kind=link}

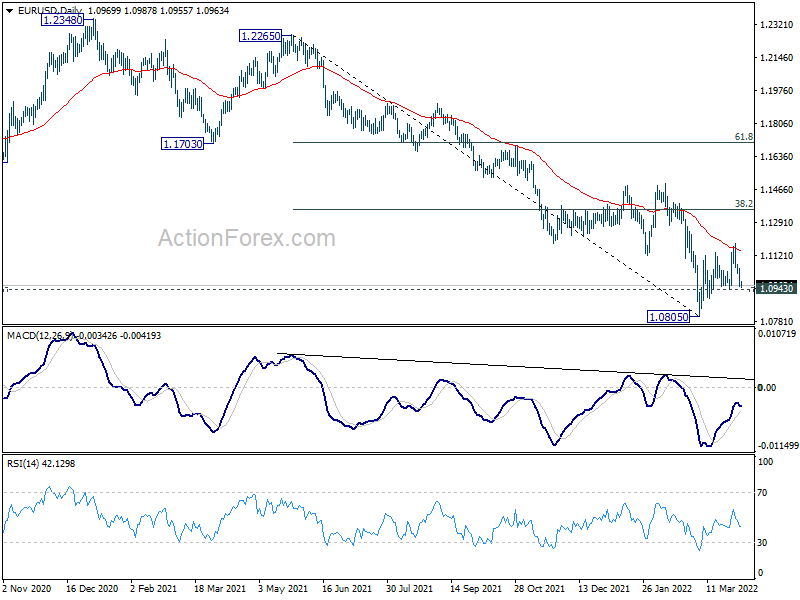

In the bigger picture, the decline from 1.2348 (2021 high) is expected to continue as long as 1.1494 resistance holds. Firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next. Nevertheless, break of 1.1494 will maintain medium term neutral outlook, and extending term range trading first.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Construction Index Mar | 56.5 | 53.4 | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Feb | 1.20% | 0.60% | 0.90% | 1.10% |

| 23:30 | JPY | Overall Household Spending Y/Y Feb | 1.10% | 2.70% | 6.90% | |

| 04:30 | AUD | RBA Interest Rate Decision | 0.10% | 0.10% | 0.10% | |

| 06:45 | EUR | France Industrial Output M/M Feb | -0.90% | -0.50% | 1.60% | 1.80% |

| 07:45 | EUR | Italy Services PMI Mar | 52.1 | 51.5 | 52.8 | |

| 07:50 | EUR | France Services PMI Mar F | 57.4 | 57.4 | 57.4 | |

| 07:55 | EUR | Germany Services PMI Mar F | 56.1 | 55 | 55 | |

| 08:00 | EUR | Eurozone Services PMI Mar F | 55.6 | 54.8 | 54.8 | |

| 08:30 | GBP | Services PMI Mar F | 62.6 | 61 | 61 | |

| 12:30 | CAD | Trade Balance (CAD) Feb | 2.7B | 2.9B | 2.6B | 3.1B |

| 12:30 | USD | Trade Balance (USD) Feb | -89.2B | -88.5B | -89.7B | -89.2B |

| 13:45 | USD | Services PMI Mar F | 58.9 | 58.9 | ||

| 14:00 | USD | ISM Services PMI Mar | 57.7 | 56.5 |