It feels like the markets are turning a corner. Euro staged a strong rebound overnight on hope of cease-fire in Ukraine. Focus has then turned to Yen today, which is staging a notable recovery in Asia. On the other hand, both Dollar and Sterling are under some selling pressure. Commodity currencies are mixed for now. In other markets, US 10-year yield took a dive and the mostly watched 2-10yr yield curve is about to invert. US stocks shrugged the recession warning and closed higher. Gold is recovering after yesterday’s fall but oil remains heavy.

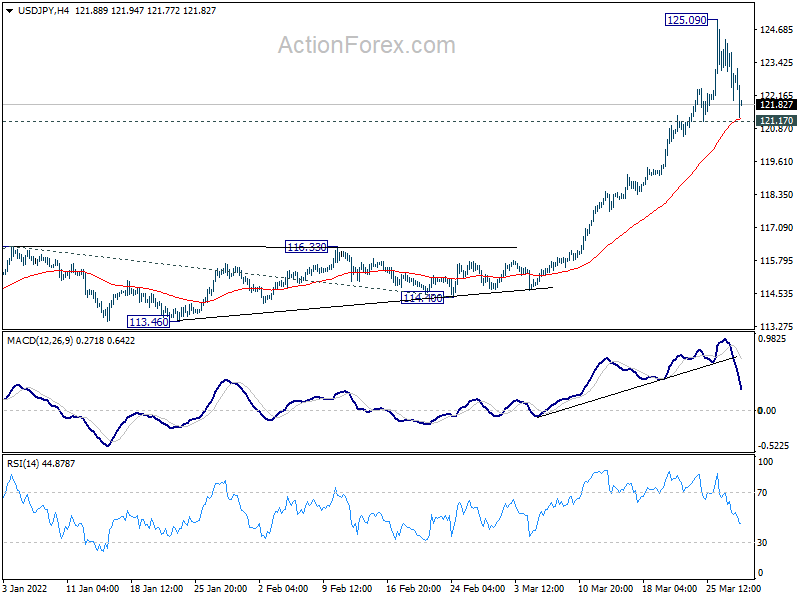

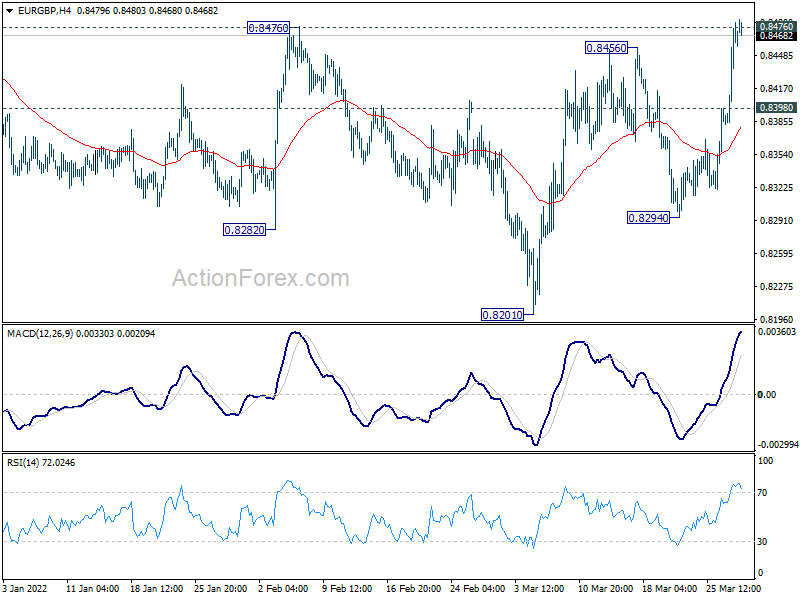

Technically, firstly, Euro will still have to do more to confirm that it’s in a bullish reversal. Levels to watch include 1.1120 resistance in EUR/USD, 0.8476 resistance in EUR/GBP and 1.0400 resistance in EUR/CHF. These levels are not decisively taken out yet. Secondly, focus will also be on 121.17 minor support in USD/JPY. Break there will confirm short term topping, to be followed by deeper near term correction.

{kind=link}

In Asia, at the time of writing, Nikkei is down -1.64%. Hong Kong HSI is up 1.14%. China Shanghai SSE is up 1.42%. Singapore Strait Times is up 0.04%. Japan 10-year JGB yield is down -0.0283 at 0.224, and it seems like BoJ’s intervention is working. Overnight, DOW rose 0.97%. S&P 500 rose 1.23%. NASDAQ rose 1.84%. 10-year yield dropped -0.077 to 2.400.

S&P 500 broke key resistance, heading back to record high

S&P 500 rose 1.23% to close at 4631.60 overnight. The solid break of 4595.31 resistance should confirm that correction from 4818.62 has completed with three waves down to 4114.65. Further rise is now expected as long as 4455.61 support holds, for retesting 4818.62 record high.

At the same time, NASDAQ has taken out corresponding resistance level at 14509.55. It’s time for DOW to break through 35824.28 resistance to align with the overall developments.

BoJ increases size of JGB purchases to defend yield cap

BoJ announced to increase the size of its JGB purchases to defend it’s 10-year yield cap imposed under the yield curve control.

It increased the size of purchase of JGB with maturities of 3 to 10 years today, by a combined JPY 450B to JPY 1325B. It will additionally buy JPY 150B of JGB with maturities between 10 to 25 years, and JPY 100B with maturity more than 25 years.

“The BOJ will increase the number of auction dates and the amount of outright JGB purchases as needed, taking account of market conditions,” the BOJ said in a statement.

Released from Japan, retail sales dropped -0.8% yoy in February, worse than expectation of -0.3% yoy.

New Zealand ANZ business confidence rose to -41.9, inflation expectations rose again

New Zealand ANZ business confidence rose from -51.8 to -41.9 in March. Own activity outlook rose from -2.2 to 3.3. Looking at some details, export intentions rose from 0.9 to 7.9. Investment intentions rose from 4.5 to 5.2. Employment intentions rose from 2.3 to 12.3. Pricing intentions rose from 74.1 to 80.5. Cost expectations rose from 92.0 to 95.9. Inflation expectations rose back from 5.29 to 5.51.

ANZ said: “With inflation pressures now so extreme, and the RBNZ’s inflation-targeting credibility on the line, it’s full steam ahead for rate hikes – we’re forecasting 50bp hikes in both April and May.

“It could well be a rough ride, but maintaining medium-term price stability is the best contribution monetary policy can make to New Zealand’s big-picture economic prospects from this very difficult starting point.”

Also from New Zealand, building permits rose 10.5% mom in February.

Looking ahead

Swiss KOF economic barometer and Credit Suisse economic expectations will be release in European session. Eurozone will release economic sentiment indicator. Germany will release March CPI flash.

Later in the day, main focus is on US ADP employment while Q4 GDP final will be published.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8409; (P) 0.8445; (R1) 0.8505; More…

Intraday bias in EUR/GBP remains on the upside with focus on 0.8476 structural resistance. Decisive break there should confirm medium term bottoming at 0.8201, with a head and shoulder bottom pattern too (ls: 0.8282, h: 0.8201, rs: 0.8294). In this case, near term outlook will turn bullish for 0.8697 fibonacci level next. On the downside, however, below 0.8398 minor support will mix up the outlook and turn intraday bias neutral first.

{kind=link}

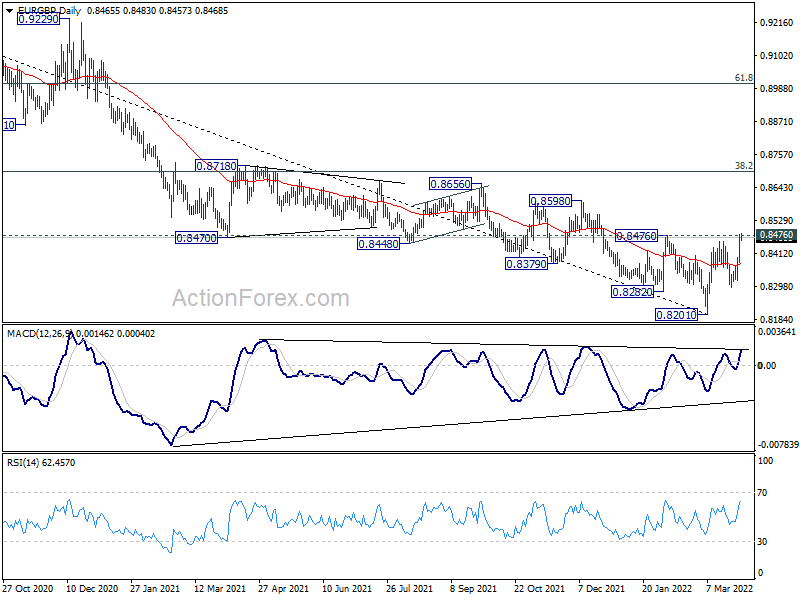

In the bigger picture, the down trend from 0.9499 is expected to continue as long as 0.8476 resistance holds. Sustained trading below 0.8276 support will argue that the whole up trend from 0.6935 (2015 low) has reversed. Deeper fall should be seen to 61.8% retracement of 0.6935 to 0.9499 at 0.7917 next. However, firm break of 0.8476 will indicate medium term bottoming at least, on bullish convergence condition in daily and weekly MACD. Stronger rally would be seen back to 38.2% retracement of 0.9499 to 0.8201 at 0.8697.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Feb | 10.50% | -9.20% | -8.70% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y Feb | 2.10% | 1.80% | ||

| 23:50 | JPY | Retail Trade Y/Y Feb | -0.80% | -0.30% | 1.10% | |

| 00:00 | NZD | ANZ Business Confidence Mar | -41.9 | -51.8 | ||

| 07:00 | CHF | KOF Leading Indicator Mar | 101 | 105 | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Mar | 9 | |||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Mar | 110 | 114 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Mar | 8.9 | 14 | ||

| 09:00 | EUR | Eurozone Services Sentiment Mar | 10 | 13 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Mar F | -18.7 | -18.7 | ||

| 12:00 | EUR | Germany CPI M/M Mar P | 1.60% | 0.90% | ||

| 12:00 | EUR | Germany CPI Y/Y Mar P | 6.10% | 5.10% | ||

| 12:15 | USD | ADP Employment Change Mar | 450K | 475K | ||

| 12:30 | USD | GDP Annualized Q4 F | 7.10% | 7.00% | ||

| 12:30 | USD | GDP Price Index Q4 F | 7.10% | 7.10% | ||

| 14:30 | USD | Crude Oil Inventories | -2.0M | -2.5M |