The forex markets are digesting recent moves in mixed Asian session today. Yen is recovering slightly but remains the worst performer for the week. BoJ is still trying hard to defend the 0.25% 10-year JGB yield cap. On the other hand, Euro and Dollar are the strongest ones so far. The greenback is trying to recover against commodity currencies and there is some near term upside prospect. Euro, on the other hand, is helped by its recovery against the Pound and Swiss Franc.

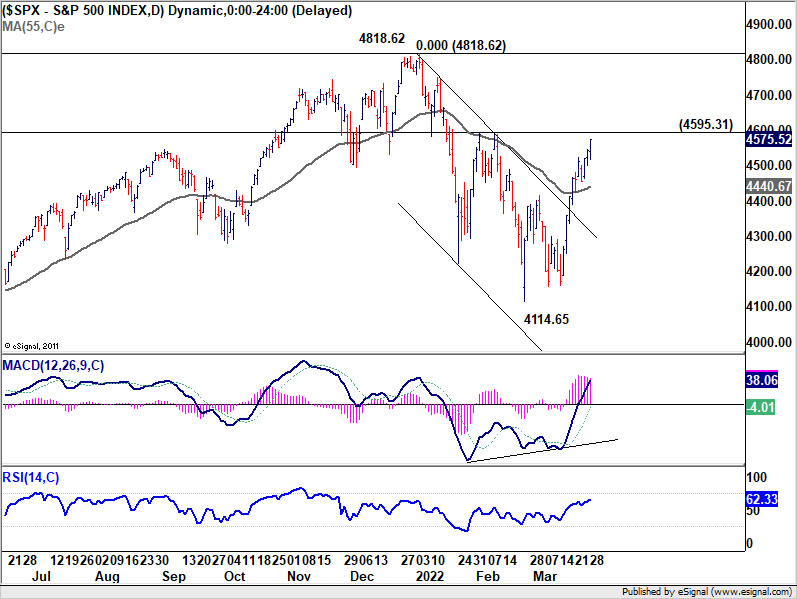

Technically, some attention will be paid to S&P 500 today after yesterday’s 0.71% rise. SPX should be testing 4959.31 resistance soon. The correction from 4818.62 should have completed with three waves down to 4114.65 already. Firm break of 4595.31 will solidify upside momentum for retest of 4818.62 high. Such development could give Yen some renewed pressure.

{kind=link}

In Asia, at the time of writing, Nikkei is up 0.67%. Hong Kong HSI is up 0.45%. China Shanghai SSE is down -0.43%. Singapore Strait Times is down -0.23%. Japan 10-year JGB yield is down -0.0069 at 0.253. Overnight, DOW rose 0.27%. S&P 500 rose 0.71%. NASDAQ rose 1.31%. 10-year yield dropped -0.015 to 2.477.

BoJ opinions emphasize importance to maintain monetary easing

In the Summary of Opinions of the March 17-18 meeting, BoJ noted, “unlike the United States and the United Kingdom, Japan is not in a situation where the inflation rate will likely exceed the price stability target of 2 percent in a continuous manner.” Hence, “it is important for the Bank to continue with monetary easing to support the economic recovery from the pandemic.”

Situations surrounding Ukraine have “caused price rises of energy and other items”, and this will “push down domestic demand while raising the CPI.” Under these circumstances, it is “necessary to improve labor market conditions and provide stronger support for wage increases”.

One member warned that “if downward pressure on economic activity and prices increases, the economy may instead be in danger of falling into deflation again. If it becomes difficult to achieve the price stability target, the Bank should act nimbly and without hesitation.”

Japan FM Suzuki carefully watching bad yen weakening

Japan Finance Minister Shunichi Suzuki said the government is carefully watching the foreign exchange market to avoid “bad yen weakening”. He repeated that currency stability was important. While a weak Yen is positive for exporters, it’s negative for household on popping up living costs.

Yesterday, BoJ started offering four days of unlimited bond purchases to defend the 0.25% cap of 10-year JGB yield. The first offer drew no bid but JPY 64.5B in JGBs were accepted in the second offer. According to the current guidance, BoJ targets to keep 10-year JGB yield at around 0% with 25bps limit up and down.

Released from Japan, unemployment rate dropped from 2.8% to 2.7% in February, better than expectation of 2.8%.

Australia retail sales rose 1.8% mom in Feb, hitting second highest on record

Australia retail sales rose 1.8% mom to AUD 33.09B in February, well above expectation of 1.0% mom.

Director of Quarterly Economy Wide Statistics, Ben James, said February’s result saw retail sales reach their second highest level on record after November 2021 and turnover continuing to regain lost momentum caused by the peak of the Omicron outbreak in January.

“Lower COVID-19 case numbers in February, alongside the further easing of restrictions over the month, saw consumer spending return to similar behaviour seen previously as states and territories come out of a COVID-19 wave,” James said.

Looking ahead

Germany Gfk consumer sentiment and import prices, UK mortgage approvals and M4 money supply, will be release in European session. Later in the day, US will release house price index and consumer confidence.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7459; (P) 0.7500; (R1) 0.7532; More…

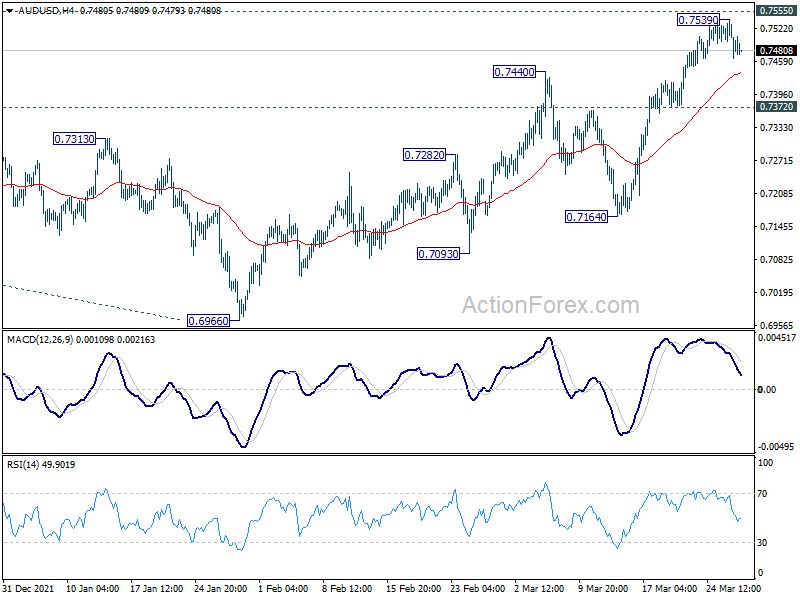

A temporary top is formed at 0.7539 in AUD/USD, just ahead of 0.7555 resistance. Intraday bias is turned neutral for some consolidations first. Further rise is expected as long as 0.7372 minor support holds. On the upside, decisive break of 0.7555 should confirm that whole corrective decline from 0.8006 has completed at 0.6966. Further rise should then be seen back to retest 0.8005. However, break of 0.7372 will dampen this bullish view and turn bias back to the downside for 0.7164 support instead.

{kind=link}

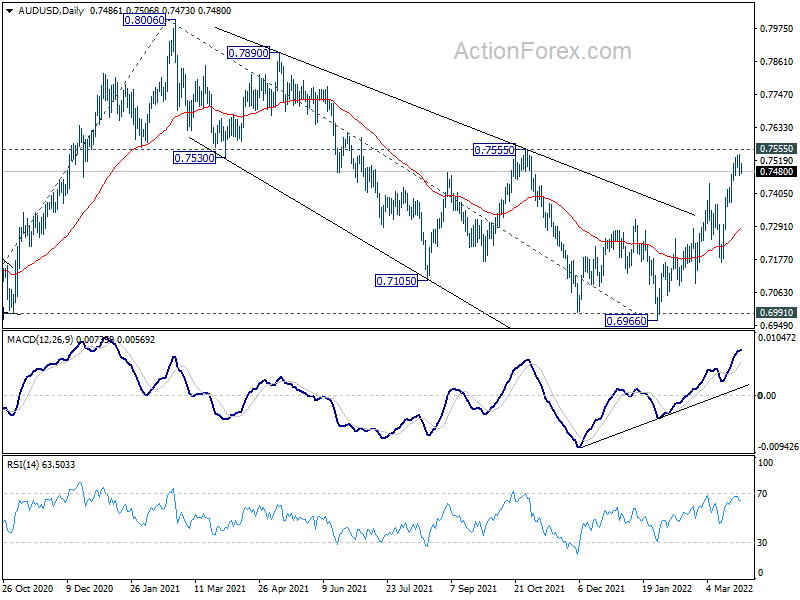

In the bigger picture, correction from 0.8006 could have completed at 0.6966, after drawing support from 0.6991. That is, up trend from 0.5506 (2020 low) might be ready to resume. Firm break of 0.8006 will target 61.8% projection of 0.5506 to 0.8006 from 0.6966 at 0.8511 next. This will remain the favored case as long as 0.7164 support holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Unemployment Rate Feb | 2.70% | 2.80% | 2.80% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 00:30 | AUD | Retail Sales M/M Feb | 1.80% | 1.00% | 1.80% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence Survey Apr | -12 | -8.1 | ||

| 06:00 | EUR | Germany Import Price Index M/M Feb | 2.10% | 4.30% | ||

| 08:30 | GBP | Mortgage Approvals Feb | 73K | 74K | ||

| 08:30 | GBP | M4 Money Supply M/M Feb | 0.50% | 0.10% | ||

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y Jan | 18.40% | 18.60% | ||

| 13:00 | USD | Housing Price Index M/M Jan | 1.40% | 1.20% | ||

| 14:00 | USD | Consumer Confidence Mar | 107.9 | 110.5 |