Dollar is digesting some of this week’s gain as markets are awaiting FOMC rate hike and economic projections. There are a lot questions to be answered given the uncertainty over inflation and the economic impact of Russia invasion of Ukraine. As for today, Aussie and Euro are the stronger ones while Dollar and Yen are soft. But the picture could flip in any direction depending on the FOMC outcome.

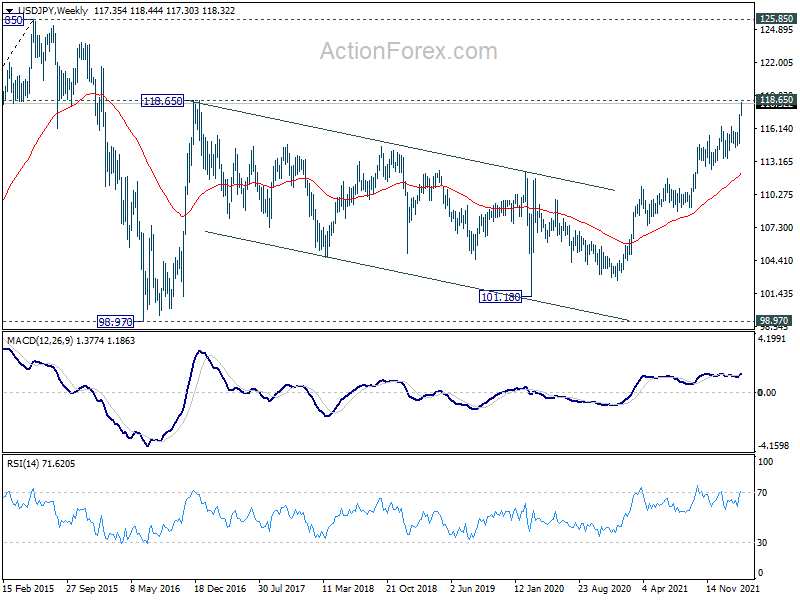

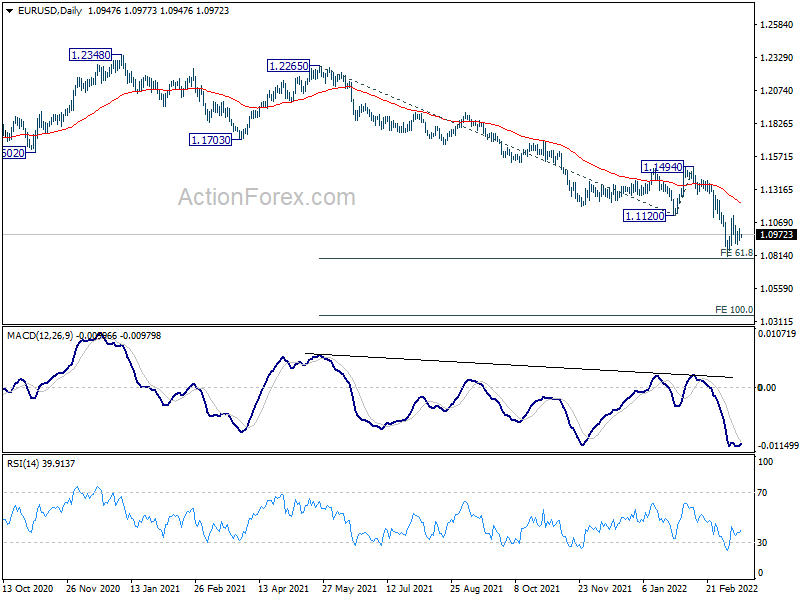

Technically, if Dollar is to show its muscle today, the first move should be a strong break of 118.65 long term resistance (2016 high) in USD/JPY. The second should be a decisive break of 1.0805 near term bottom in EUR/USD. We’ll see if the greenback could do that to confirm it’s strength.

In Asia, Nikkei closed up 1.64%. Hong Kong HSI is up 7.81%. China Shanghai SSE is up 3.41%. Singapore Strait Times is up 1.42%. Japan 10-year JGB yield is down -0.0053 at 0.205. Overnight, DOW rose 1.82%. S&P 500 rose 2.14%. NASDAQ rose 2.92%. 10-year yield rose 0.020 to 2.160.

ECB Lagarde: Russia-Ukraine war lowers and raises inflation

ECB President Christine Lagarde said in a speech that the Russia-Ukraine war would “lower growth and raise inflation through higher energy and commodity prices, the disruption of international trade and weaker confidence”. But the baseline scenario is still for the economy to “grow robustly in 2022”.

However, “uncertainty surrounding the outlook had increased significantly”, policy makers are looking at two alternative scenarios that ” growth could be dampened significantly and inflation could be considerably higher in the near term”. Still, “in all scenarios, inflation is still expected to decrease progressively and settle at levels around our two per cent inflation target in 2024.”

Lagarde added that if data support the expectation that medium-term inflation outlook will not weaken even after the end of net asset purchases, ECB will “conclude net purchases in the third quarter”. Any adjustments to interest rates will “take place some time after the end of our net purchases and will be gradual.”

Japan imports surged 34% yoy in Feb on Yen depreciation and higher energy prices

Japan exports rose 19.1% yoy to JPY 7190B in February. That’s the 12th straight month of growth. Auto exports increased 8.3% yoy, rebounding from January’s -1.0% yoy decline. Exports to the US rose 16.0% yoy to JPY 1.3T. Exports to China rose 25.8% yoy to JPY 1.5T.

Imports rose 34.0% yoy to 7858B. That’s the 13th consecutive month of growth. Crude oil imports surged a massive 93.2% yoy to JPY 08.6B, up for the 11th straight months, on the back of Yen’s depreciation and higher oil prices. Trade deficit came in at JPY -668B.

In seasonally adjusted terms, exports dropped -0.5% mom to JPY 7432B. Imports rose 2.7% mom to JPY 8463B. Trade deficit widened to JPY -1031B.

Australia Westpac leading index improved slightly in Feb

Australia Westpac-MI leading index improved slightly from -0.50% to -0.25% in February. But Westpac is expecting “strong above trend growth in 2022”, largely due to the aftermath of the extraordinary emergency policy measures from both the fiscal and monetary authorities during 2020 and 2021.

Westpac expects RBA to stand pat in April meeting with its “patience” stance. But after Q1 inflation data and further progress on wages growth, RBA would moving to a tightening bias over June and July, prior to raising the cash rate in August.

FOMC rate hike and projections awaited, 10-year yield pressing key resistance

Fed is widely expected to raise interest rate for the first time since 2018, lifting the federal funds rate target by just 25bps to 0.25-0.50%. It’s nonetheless the start of a tightening cycle to combat persistently high inflation.

The new economic projections would be the main market moving factor. Given the development since December, it’s likely that FOMC members are now penciling more than just three 25bps rate hike this year. There are three questions to answer. Firstly, where would interest be by the end of the year? Secondly, is FOMC going to “front-load” some of the rate hikes? And thirdly, will the estimated longer run federal funds rate be lifted from the current 2.50%?

US 10-year yield is extending recent up trend this week, and it’s now pressing a important long term resistance zone at 2.159/2.187 (61.8% retracement of 3.248 to 0.398 at 2.159, 61.8% projection of 0.398 to 1.765 to 1.343 at 2.187). This level is expected to hold for a while.

Nevertheless, a strong break there could clear the way to 100% projection at 2.710, probably with some medium term up side acceleration. That, if happens, would be very supportive to USD/JPY and set up further rally back to 125, the level reached only back in 2015.

Next target is cluster resistance level at 2.159/2.187 (61.8% retracement of 3.248 to 0.398 at 2.159, 61.8% projection of 0.398 to 1.765 to 1.343 at 2.187). Current upside momentum doesn’t warrant a strong break of this cluster level yet. This, strong resistance will likely be seen there to set the top of the range of a medium term consolidation.

However, strong break of 2.159/2.187 will suggest some dramatic underlying development. In such case, coupled with extending risk aversion, the greenback could be given a strong, sustainable boost.

{kind=link}

{kind=link}

On the data front

Canada CPI and wholesale sales will be released. US retail sales import price, business inventories, NAHB housing index will also be featured.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0914; (P) 1.0967; (R1) 1.1008; More…

EUR/USD is still bounded in range of 1.0805/1120 and intraday bias remains neutral first. Further decline is still expected with 1.1120 support turned resistance intact. On the downside, firm break of 61.8% projection of 1.2265 to 1.1120 from 1.1494 at 1.0786 will pave they way to 100% projection at 1.0349 next. However, strong break of 1.1120 will confirm short term bottoming, at least, and bring stronger rebound back towards 1.1494 structural resistance instead.

{kind=link}

In the bigger picture, the decline from 1.2348 (2021 high) is expected to continue as long as 1.1494 resistance holds. Firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next. Nevertheless, break of 1.1494 will maintain medium term neutral outlook, and extend range trading first.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Current Account (NZD) Q4 | -7.26B | -6.49B | -8.30B | -8.25B |

| 23:30 | AUD | Westpac Leading Index M/M Feb | -0.20% | 0.10% | ||

| 23:50 | JPY | Trade Balance (JPY) Feb | -1.03T | -0.39T | -0.93T | -0.78T |

| 04:30 | JPY | Industrial Production M/M Jan F | -0.80% | -1.30% | -1.30% | |

| 12:30 | CAD | Wholesale Sales M/M Jan | 4.00% | 0.60% | ||

| 12:30 | CAD | CPI M/M Feb | 0.90% | 0.90% | ||

| 12:30 | CAD | CPI Y/Y Feb | 5.50% | 5.10% | ||

| 12:30 | CAD | CPI Common Y/Y Feb | 2.40% | 2.30% | ||

| 12:30 | CAD | CPI Median Y/Y Fed | 3.50% | 3.30% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Fed | 4.20% | 4.00% | ||

| 12:30 | USD | Retail Sales M/M Feb | 0.60% | 3.80% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Feb | 0.90% | 3.30% | ||

| 12:30 | USD | Export Price Index Y/Y Feb | 12.60% | 15.10% | ||

| 12:30 | USD | Import Price Index M/M Feb | 1.60% | 2.00% | ||

| 14:00 | USD | Business Inventories Jan | 1.10% | 2.10% | ||

| 14:00 | USD | NAHB Housing Market Index Mar | 81 | 82 | ||

| 15:30 | USD | Crude Oil Inventories | -1.8M | -1.9M | ||

| 18:00 | USD | Fed Interest Rate Decision | 0.50% | 0.25% | ||

| 18:30 | USD | FOMC Press Conference |