Canadian Dollar surges broadly in early US session after stronger than expected consumer inflation reading, which solidifies the case for more tightening from BoC. Though, as for today, Aussie is still the strongest, as helped by the massive rebound in China stocks earlier. Yen is turning soft again but following global risk rebound, and more importantly, rally in US and European benchmark yields. European majors are mixed.

Dollar is also soft in consolidation, awaiting FOMC’s 25bps rate hike, There are three questions to answer. Firstly, where would interest be by the end of the year? Secondly, is FOMC going to “front-load” some of the rate hikes? And thirdly, will the estimated longer run federal funds rate be lifted from the current 2.50%? The new economic projections would hopefully provide something concrete.

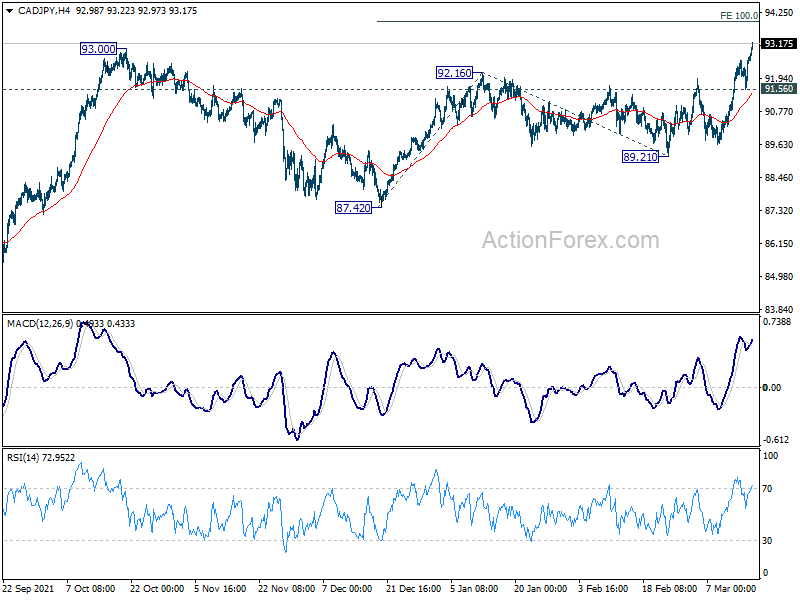

Technically, CAD/JPY rises through 93.00 high to resume the medium term up trend from 73.80. Next target is 100% projection of 87.42 to 92.16 from 89.21 at 93.95. Attention is now on when AUD/JPY would follow and break through 86.24 resistance to resume the up trend from 59.85.

{kind=link}

In Europe, at the time of writing, FTSE is up 1.39%. DAX is up 2.82%. CAC is up 3.26%. Germany 10-year yield is up 0.0544 at 0.390. Earlier in Asia, Nikkei rose 1.64%. Hong Kong HSI rose 9.08%. China Shanghai SSE rose 3.48%. Singapore Strait Times rose 1.70%. Japan 10-year JGB yield dropped -0.0068 to 0.204.

US retail sales rose 0.3% mom in Feb, ex-auto sales rose 0.2% mom, missed expectations

US retail sales rose 0.3% mom to USD 658.1B in February, below expectation of 0.6% mom. Ex-auto sales rose 0.2% mom, below expectation of 0.9% mom. Ex-gasoline sales dropped -0.2% mom. Ex-auto, ex-gasoline sales dropped -0.4% mom. Total sales for December 2021 through February 2022 period were up 16.0% from the same period a year ago.

Import price index rose 1.4% mom in February, below expectation of 1.6% mom.

Canada CPI jumped to 5.7% yoy in Feb, highest since 1991

Canada CPI accelerated sharply form 5.1% yoy to 5.7% yoy in February, above expectation of 5.5% yoy. That’s the largest gain since August 1991, and it’s the second consecutive month where headline inflation exceeded 5% level. Excluding gasoline, CPI rose 4.7% yoy up from January’s 4.3% yoy, fastest since its introduction in 1999. On a monthly basis, CPI rose 1.0% mom in February, largest monthly increase since February 2013.

CPI common rose from 2.3% yoy to 2.6% yoy, above expectation of 2.4% yoy. CPI median rose from 3.3% yoy to 3.5% yoy, matched expectations. CPI trimmed rose from 4.0% yoy to 4.3% yoy, above expectation of 4.2% yoy.

ECB Nagel doesn’t expect stagflation at the moment

ECB Governing Council member Joachim Nagel told German newspaper Handelsblatt, “I don’t expect stagflation at the moment, even though the fallout of the war will boost inflation rates and weaken economic growth.” He added that there are currently “no signs” of a wage-price spiral.

He said ECB’s current approach of tapering asset purchases while being non-committal on rate hike was a “good and balanced” approach. He said, “”I consider it very important that we don’t pre-commit in times of high uncertainty, but stay flexible.”

Japan imports surged 34% yoy in Feb on Yen depreciation and higher energy prices

Japan exports rose 19.1% yoy to JPY 7190B in February. That’s the 12th straight month of growth. Auto exports increased 8.3% yoy, rebounding from January’s -1.0% yoy decline. Exports to the US rose 16.0% yoy to JPY 1.3T. Exports to China rose 25.8% yoy to JPY 1.5T.

Imports rose 34.0% yoy to 7858B. That’s the 13th consecutive month of growth. Crude oil imports surged a massive 93.2% yoy to JPY 08.6B, up for the 11th straight months, on the back of Yen’s depreciation and higher oil prices. Trade deficit came in at JPY -668B.

In seasonally adjusted terms, exports dropped -0.5% mom to JPY 7432B. Imports rose 2.7% mom to JPY 8463B. Trade deficit widened to JPY -1031B.

Australia Westpac leading index improved slightly in Feb

Australia Westpac-MI leading index improved slightly from -0.50% to -0.25% in February. But Westpac is expecting “strong above trend growth in 2022”, largely due to the aftermath of the extraordinary emergency policy measures from both the fiscal and monetary authorities during 2020 and 2021.

Westpac expects RBA to stand pat in April meeting with its “patience” stance. But after Q1 inflation data and further progress on wages growth, RBA would moving to a tightening bias over June and July, prior to raising the cash rate in August.

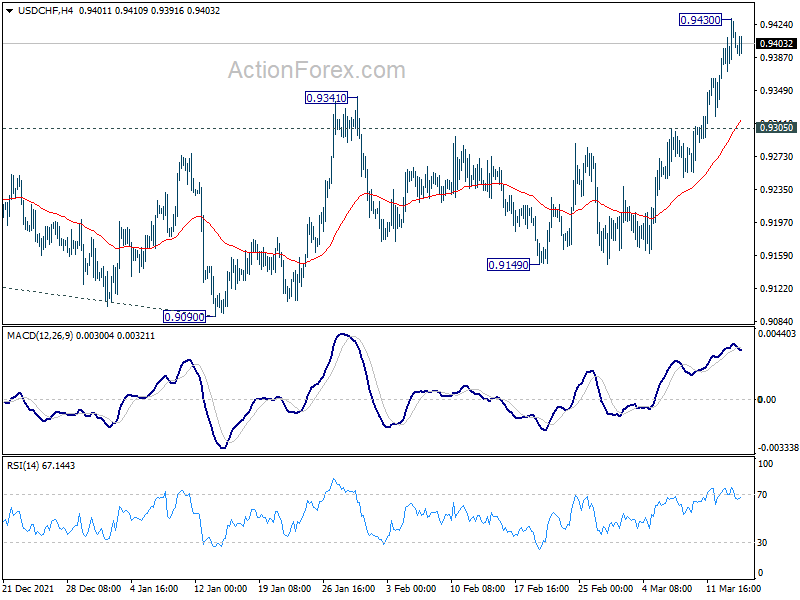

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9380; (P) 0.9406; (R1) 0.9438; More….

Intraday bias in USD/CHF remains neutral for consolidation below 0.9430. Downside of retreat should be contained above 0.9305 resistance turned support to bring another rally. On the upside, above 0.9430 will target 0.9471 resistance first. Break there will resume whole rally from 0.8756 to 61.8% projection of 0.8756 to 0.9471 from 0.9090 at 0.9532.

{kind=link}

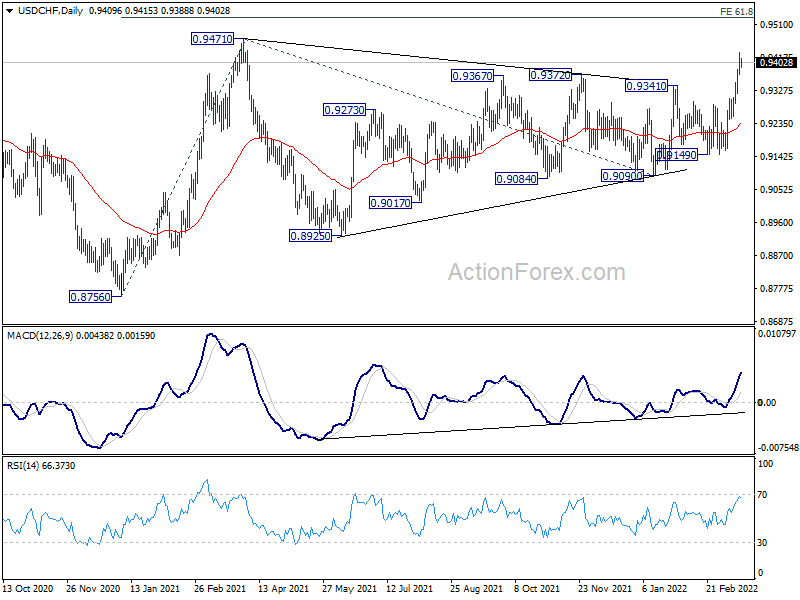

In the bigger picture, medium term outlook will be neutral at best as long as 0.9471 resistance holds. Larger down trend could still extend through 0.8756 (2021 low). However, firm break of 0.9471 will argue that whole down trend form 1.0342 (2016 high), has completed with waves down to 0.8756. A medium term up trend should be set up to target 1.0237/0342 resistance zone.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Current Account (NZD) Q4 | -7.26B | -6.49B | -8.30B | -8.25B |

| 23:30 | AUD | Westpac Leading Index M/M Feb | -0.20% | 0.10% | ||

| 23:50 | JPY | Trade Balance (JPY) Feb | -1.03T | -0.39T | -0.93T | -0.78T |

| 04:30 | JPY | Industrial Production M/M Jan F | -0.80% | -1.30% | -1.30% | |

| 12:30 | CAD | Wholesale Sales M/M Jan | 4.20% | 4.00% | 0.60% | |

| 12:30 | CAD | CPI M/M Feb | 1.00% | 0.90% | 0.90% | |

| 12:30 | CAD | CPI Y/Y Feb | 5.70% | 5.50% | 5.10% | |

| 12:30 | CAD | CPI Common Y/Y Feb | 2.60% | 2.40% | 2.30% | |

| 12:30 | CAD | CPI Median Y/Y Fed | 3.50% | 3.50% | 3.30% | |

| 12:30 | CAD | CPI Trimmed Y/Y Fed | 4.30% | 4.20% | 4.00% | |

| 12:30 | USD | Retail Sales M/M Feb | 0.30% | 0.60% | 3.80% | |

| 12:30 | USD | Retail Sales ex Autos M/M Feb | 0.20% | 0.90% | 3.30% | |

| 12:30 | USD | Import Price Index M/M Feb | 1.40% | 1.60% | 2.00% | |

| 14:00 | USD | Business Inventories Jan | 1.10% | 2.10% | ||

| 14:00 | USD | NAHB Housing Market Index Mar | 81 | 82 | ||

| 15:30 | USD | Crude Oil Inventories | -1.8M | -1.9M | ||

| 18:00 | USD | Fed Interest Rate Decision | 0.50% | 0.25% | ||

| 18:30 | USD | FOMC Press Conference |