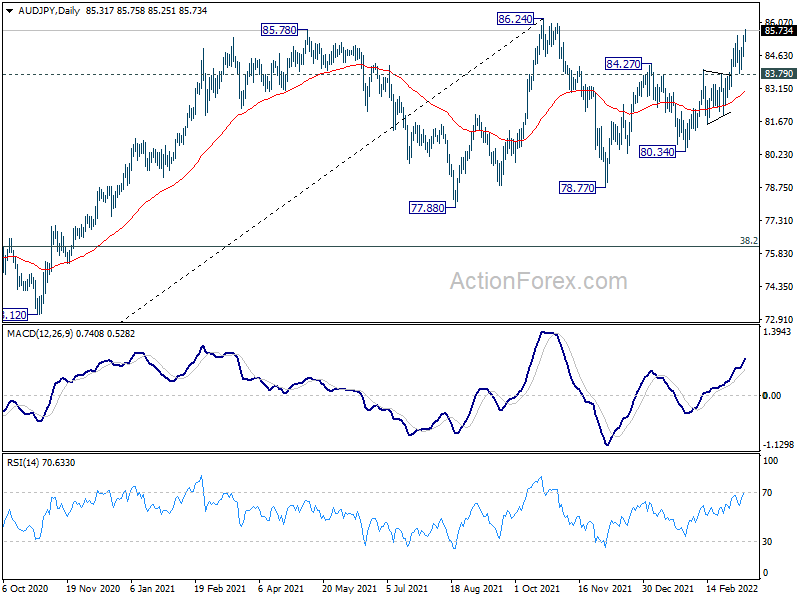

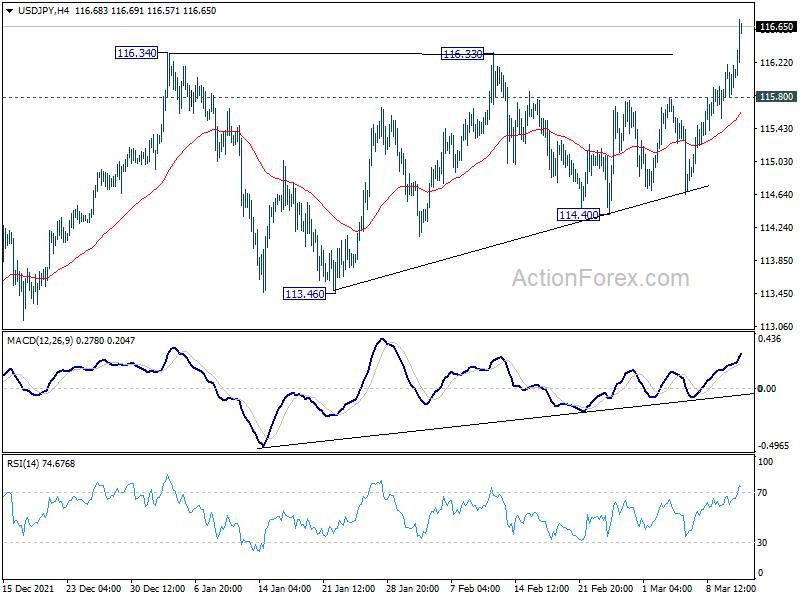

Yen is under some broad based pressure in Asia session despite some mild risk aversion sentiment. BoJ is clear to lag behind other major central bank in raising interest rates, due to the still underperforming inflation. Rally in global treasury yields is also weighing on the Japanese currency. Euro is maintaining this week’s recovery, but is apparently struggling to extend rebound as Russia invasion of Ukraine drags on. Dollar is firm and the upside breakout against Yen is a positive sign.

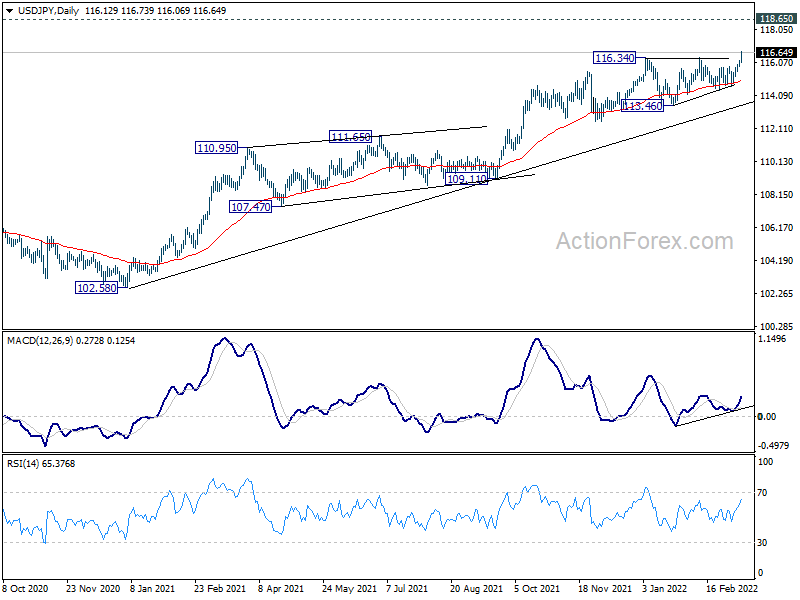

Technically, USD/JPY finally breaks through 116.34 resistance to resume medium term up trend. Next target is long term resistance level at 118.65. At the same time, AUD/JPY is also marching towards 86.24 high. Firm break there will resume medium term up trend too and would add to the case of more broad based Yen selloff. Though, break of 83.79 support will suggest rejection by 86.24 and bring near term reversal.

{kind=link}

In Asia, Nikkei closed down -2.05%. Hong Kong HSI is down -1.69%. China Shanghai SSE is down -0.22%. Singapore Strait Times is up 0.22%. Japan 10-year JGB yield is down -0.0078. Overnight, DOW dropped -0.34%. S&P 500 dropped -0.43%. NASDAQ dropped -0.95%. 10-year yield rose 0.063 to 2.011 (but it’s retreating in Asia).

IMF Georgieva: Global growth forecast to be downgraded, but remains in positive territory

IMF Managing Director Kristalina Georgieva told CNBC yesterday, “we think that we would be downgrading our growth projections as a result of the crisis (in Ukraine), but we still expect the world to be in positive growth territory.”

In the January outlook IMF projected global growth of 4.4% in 2022. For now, it’s unsure how the global economy would be affected by Russia invasion on Ukraine. “Obviously, how long this war goes is the main uncertainty factor we face,” Georgieva said.

Separately, Georgieva also said, sanctions on Russia for its invasion of Ukraine would cause an abrupt contraction of the Russian economy. Russia is facing a “deep recession” this year, and sovereign debt default is no longer seen as “improbable”.

RBA Lowe: It’s prudent to plan for an interest rate increase

RBA Governor Philip Lowe said it’s “plausible” for interest to be lifted from the current 0.1% this year. “It would be prudent to plan for an increase,” he added. “For many borrowers that’s going to come as quite an unwelcome development, although I know from the letters that I get every day when I turn up at work that many depositors have a different view,”

Meanwhile, he said “I don’t feel mounting pressure,” on raising rates. “We do what we think is the right thing at each of our meetings, so the pressure, it’s great for media stories, but I don’t feel that myself.”

New Zealand BNZ manufacturing rose to 53.6, next result may see fallout from Russia/Ukraine conflict

New Zealand BNZ Performance of Manufacturing Index rose from 52.3 to 53.6 in February. Looking at some details, Production rose from 51.1 to 52.1. Employment rose from 49.5 to 51.7. New Orders rose from 53.6 to 58.2. Finished stocks dropped from 52.5 to 50.0. Deliveries dropped from 54.0 to 53.5.

BNZ Senior Economist, Craig Ebert stated that “underlying unease will certainly be piqued by the sustained high COVID case numbers as we go into March. The next PMI result may also see fallout from the Russia/Ukraine conflict, whose global impacts will be felt far and wide.”

Elsewhere

Japan overall household spending rose 6.9% yoy in January, above expectation of 3.6% yoy. BSI large manufacturing condition dropped sharply from 8.2 to -7.6 in Q1.

UK GDP, production and trade balance are the major focuses in European session. Germany will release CPI final. Later in the day, Canada employment data will take center stage. US will release U of Michigan consumer sentiment.

USD/JPY Daily Outlook

Daily Pivots: (S1) 115.91; (P) 116.05; (R1) 116.29; More…

USD/JPY’s break of 116.34 resistance confirms up trend resumption. Intraday bias is back on the upside. Current rally should now target next long term resistance at 118.65. On the downside, below 115.80 minor support will turn intraday bias neutral first. But outlook will remain bullish as long as 114.40 support holds, in case of retreat.

{kind=link}

In the bigger picture, no change in the view that rise from 102.58 is the third leg of the up trend from 101.18 (2020 low). Such rally should target a test on 118.65 (2016 high). Sustained break there will pave the way to 120.85 (2015 high) and raise the chance of long term up trend resumption. This will remain the favored case as long as 55 week EMA (now at 111.75) holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Feb | 53.6 | 52.1 | 52.3 | |

| 23:30 | JPY | Overall Household Spending Y/Y Jan | 6.90% | 3.60% | -0.20% | |

| 23:50 | JPY | BSI Large Manufacturing Conditions Index Q1 | -7.6 | 8.2 | 7.9 | |

| 07:00 | EUR | Germany CPI M/M Feb F | 0.90% | 0.90% | ||

| 07:00 | EUR | Germany CPI Y/Y Feb F | 5.10% | 5.10% | ||

| 07:00 | GBP | GDP M/M Jan | 0.20% | -0.20% | ||

| 07:00 | GBP | Index of Services 3M/3M Jan | 1.20% | 1.20% | ||

| 07:00 | GBP | Industrial Production M/M Jan | 0.30% | 0.30% | ||

| 07:00 | GBP | Industrial Production Y/Y Jan | 0.20% | 0.40% | ||

| 07:00 | GBP | Manufacturing Production M/M Jan | 0.20% | 0.20% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Jan | 3.10% | 1.30% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Jan | -12.6B | -12.4B | ||

| 13:30 | CAD | Net Change in Employment Feb | 123.0K | -200.1K | ||

| 13:30 | CAD | Unemployment Rate Feb | 6.20% | 6.50% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Mar P | 61.3 | 62.8 | ||

| 15:00 | GBP | NIESR GDP Estimate (3M) Feb | 1.10% | 0.90% |