Global stocks continue to rebound today. The West’s refrain from excluding Russia out of SWIFT was seen as a relief. But still risks remain, in particular if war spreads to NATO countries. Economic data continue to take a back seat, and even another surge in US inflation doesn’t move markets. As for currencies, Aussie is currently the strongest for the week, followed by Kiwi. Sterling and Euro are the worst performing ones.

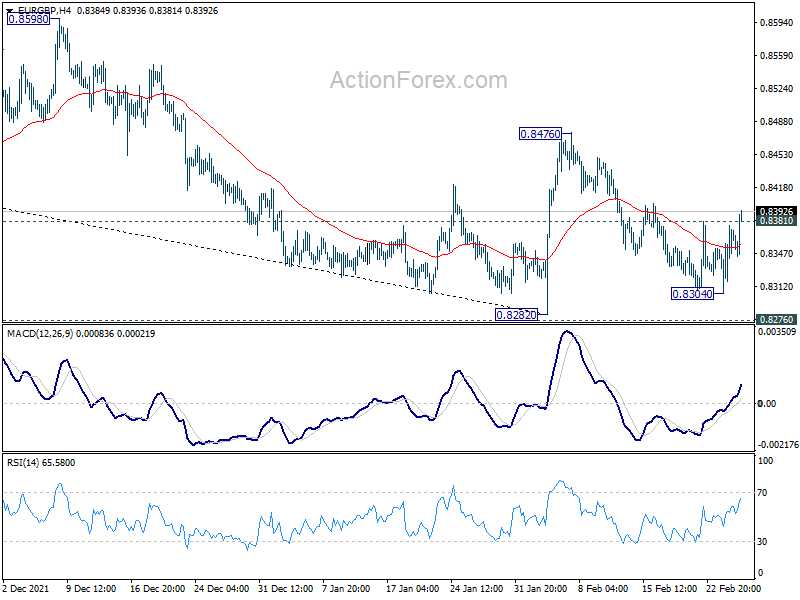

Technically, EUR/GBP’s break of 0.8381 minor resistance argues that pull back from 0.8476 might have completed at 0.8304. The tide between Euro and Sterling could be turning for the near term, as EUR/GBP could now try to head back to 0.8476 resistance level.

{kind=link}

In Europe, at the time of writing, FTSE is up 2.95%. DAX is up 2.83%. CAC is up 2.90%. Germany 10-year yield is up 0.051 at 0.223. Earlier in Asia, Nikkei rose 1.95%. Hong Kong HSI dropped -0.59%. China Shanghai SSE rose 0.63%. Singapore Strait Times rose 0.56%. Japan 10-year yield rose 0.0212 to 0.208.

US PCE inflation rose to 6.1% yoy in Jan, core PCE rose to 5.2% yoy

US personal income rose 0.0%, or USD 9B in January, better than expectation of -0.3% decline. Personal spending rose 2.1%, or USD 337.2B, above expectation of 1.5%.

Headline PCE price index accelerated from 5.8% yoy to 6.1% yoy, above expectation of 5.5% yoy. Core PCE price index rose from 4.8% yoy to 5.2% yoy, above expectation of 5.1% yoy. Energy prices rose 25.9% yoy while food prices rose 6.7% yoy.

US durable goods orders rose 1.6% in Jan, ex-transport orders up 0.7%

US durable goods orders rose 1.6%, or USD 4.3B to USD 277.5B in January, above expectation of 0.6%. Ex-transport orders rose 0.7%, above expectation of 0.4%. Ex-defends orders rose 1.6%. Transportation equipment rose 3.4%, or USD 2.9B to USD 87.6B.

BoE Mann: Important to dampen very robust inflation expectations

BoE MPC member Catherine Mann said, “to me, the data was still showing very robust (inflation) expectations and I thought it was important to dampen those expectations using a 50 basis point increase.”

“There was very little in the data that showed any diminution of expected wage increases, expected price increases or for that matter in financial markets … other than in gilts,” she added.

Mann was among the four policymakers who voted for a 50bps at last BoE meeting, which lost to a 5-4 vote.

Eurozone economic sentiment indicator rose to 114.0 in Feb, EU rose to 112.8

Eurozone Economist Sentiment Indicator rose from 112.7 to 114.0 in February. Industry confidence rose from 13.9 to 14.0. Services confidence rose from 9.1 to 13.0. Consumer confidence rose from -8.5 to -8.8. Retail trade confidence rose from 3.7 to 5.4. Employment Expectation Indicator rose from 112.7 to 116.2, highest since May 2000.

EU Economic Sentiment Indicator rose from 111.6 to 112.8. Employment Expectation Indicator rose from 113.4 to 115.8, an all time high. Amongst the largest EU economies, the ESI improved in Spain (+2.4), France (+1.9), Germany (+1.2) and Italy (+1.0), whereas it weakened in the Netherlands and Poland (both -1.7).

Also released, Germany GDP was finalized at -0.3% qoq in Q4, versus expectation of -0.7% qoq. Import price index rose 4.3% mom in January, versus expectation of 0.2% mom.

France consumer spending dropped -1.5% mom in January, versus expectation of -0.3% mom. GDP was finalized at 0.7% qoq.

RBNZ Orr: Raising rates sooner prevents the need for even higher rates

RBNZ Governor Adrian Orr said in a speech, “amongst many of our central bank peers, we were one of the first to begin removing monetary stimulus and start the tightening cycle”.

“Financial market pricing for future interest rate levels have been very responsive to our signalling,” he added. “Market pricing of future central bank policy rates continue to indicate that New Zealand is expected to tighten policy sooner than many other comparable economies.”

“By getting on top of inflation pressures quickly, by raising interest rates sooner, we aim to prevent the need for even higher rates in the future,” he said. “In other words, we are taking our foot off the accelerator now to minimise having to use the brakes harder in future.”

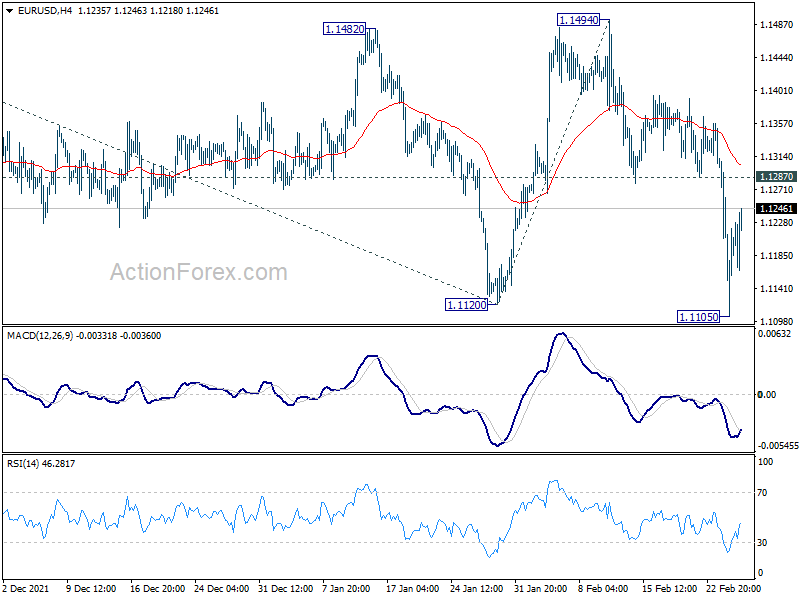

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1096; (P) 1.1204; (R1) 1.1301; More…

Intraday bias in EUR/USD is turned neutral as it’s now consolidating above 1.1105 temporary low. But Further fall is still expected with 1.1287 support turned resistance intact. Sustained break of 1.1120 will confirm resumption of larger down trend from 1.2348. Next target is 61.8% projection of 1.2265 to 1.1120 from 1.1494 at 1.0786. However, firm break of 1.1287 will dampen this bearish view and turn bias back to the upside for 1.1494 resistance.

{kind=link}

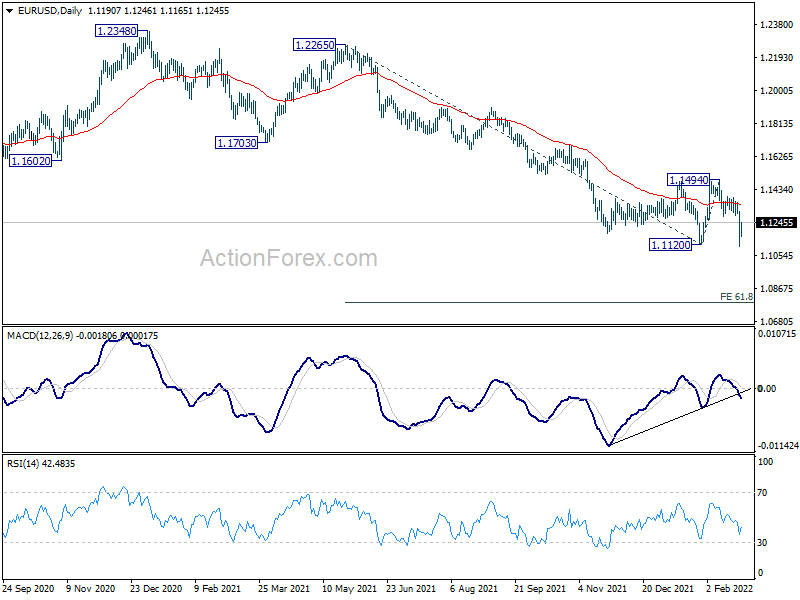

In the bigger picture, the decline from 1.2348 (2021 high) is seen as a leg inside the range pattern from 1.2555 (2018 high). Sustained trading above 55 week EMA (now at 1.1593) will argue that it has completed and stronger rise would be seen back towards top of the range between 1.2348 and 1.2555. However, firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Retail Sales Q/Q Q4 | 8.60% | 6.20% | -8.10% | -8.20% |

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q4 | 6.80% | 5.50% | -6.70% | -6.80% |

| 23:30 | JPY | Tokyo CPI Core Y/Y Feb | 0.50% | 0.40% | 0.20% | |

| 00:01 | GBP | GfK Consumer Confidence Feb | -26 | -16 | -19 | |

| 07:00 | EUR | Germany Import Price Index M/M Jan | 4.30% | 0.20% | 0.10% | |

| 07:00 | EUR | Germany GDP Q/Q Q4 F | -0.30% | -0.70% | -0.70% | |

| 07:45 | EUR | France Consumer Spending M/M Jan | -1.50% | -0.30% | 0.20% | |

| 07:45 | EUR | France GDP Q/Q Q4 | 0.70% | 0.70% | 0.70% | |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Jan | 6.40% | 6.70% | 6.90% | |

| 10:00 | EUR | Eurozone Economic Sentiment Indicator Feb | 114 | 113 | 112.7 | |

| 10:00 | EUR | Eurozone Services Sentiment Feb | 0.8 | 10.3 | 9.1 | |

| 10:00 | EUR | Eurozone Industrial Confidence Feb | 14 | 14.2 | 13.9 | |

| 10:00 | EUR | Eurozone Consumer Confidence Feb F | -8.8 | -8.8 | -8.8 | |

| 13:30 | USD | Personal Income M/M Jan | 0.00% | -0.30% | 0.30% | 0.40% |

| 13:30 | USD | Personal Spending Jan | 2.10% | 1.50% | -0.60% | -0.80% |

| 13:30 | USD | PCE Price Index M/M Jan | 0.60% | 0.30% | 0.40% | 0.50% |

| 13:30 | USD | PCE Price Index Y/Y Jan | 6.10% | 5.50% | 5.80% | |

| 13:30 | USD | Core PCE Price Index M/M Jan | 0.50% | 0.50% | 0.50% | |

| 13:30 | USD | Core PCE Price Index Y/Y Jan | 5.20% | 5.10% | 4.90% | |

| 13:30 | USD | Durable Goods Orders Jan | 1.60% | 0.60% | -0.70% | |

| 13:30 | USD | Durable Goods Orders ex Transportation Jan | 0.70% | 0.40% | 0.60% | |

| 15:00 | USD | Pending Home Sales M/M Jan | -0.20% | -3.80% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Feb F | 61.7 | 61.7 |