While risk aversion still dominates, sentiments appeared to be lifted by comments from Russian Foreign Minister Sergei Lavrov. In a televised exchanged, Lavrov told President Vladimir Putin, “I must say there are always chances… It seems to me that our possibilities are far from exhausted… At this stage, I would suggest continuing and building them up.” US futures are staging a u-turn after the comments while European indexes recovered some ground.

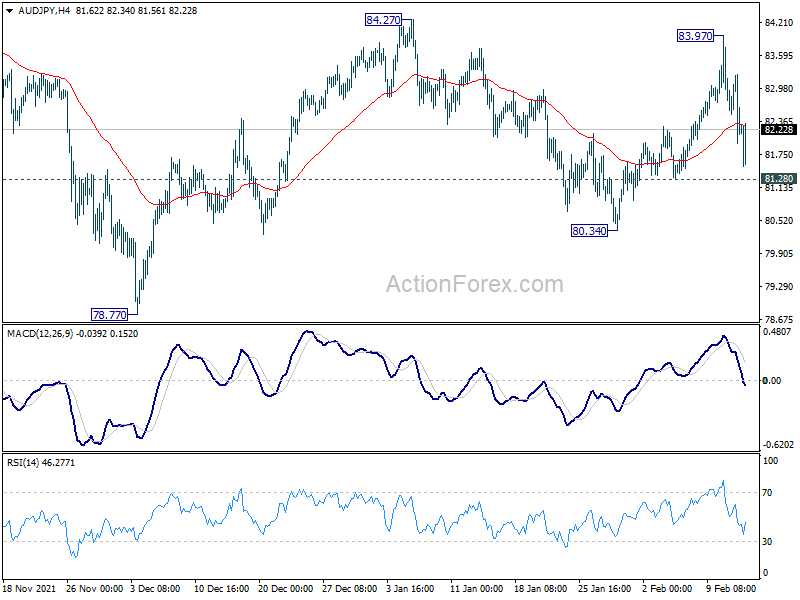

In the currency markets, Dollar is currently the strongest one for today, followed by Yen which is retreating slightly. New Zealand Dollar is the worst performing one, followed by Sterling and then Euro. Technically, there is no clear development yet. But attention will be paid to some levels in Yen crosses including 155.11 minor support in GBP/JPY, and 81.28 minor support in AUD/JPY. Break of these levels will argue that Yen buying is picking up momentum again.

{kind=link}

In Europe, at the time of writing, FTSE is down -1.41%. DAX is down -2.21%. CAC is down -2.33%. Germany 10-year yield is down -0.046 at 0.253. Earlier in Asia, Nikkei dropped -2.23%. Hong Kong HSI dropped -1.41%. China Shanghai SSE dropped -0.98%. Singapore Strait Times dropped -0.23%. Japan 10-year JGB yield dropped -0.0117 to 0.218.

Fed George: We have got to get to neutral really fast

In a WSJ interview, Kansas City Fed Esther George said that with inflation at at 7.5% in January, and the benchmark interest a rate near zero, Fed’s policy is “out of sync”. But she said it’s too soon to say if Fed should hike by 50bps in March. She also hasn’t form a view on how much interest rate has to go up this year.

“What we have to do is be systematic,” George said. “It is always preferable to go gradual…Given where we are, the uncertainties around the pandemic effects and other things, I’d be hard-pressed to say we have got to get to neutral really fast.”

“If we get to March and the data says we should be talking about that [a half-point rate increase], I’m sure that will be in play, but I’m not sure that is the answer, per se, to how we get there,” George added.

She also dismissed the idea of holding an emergency FOMC meeting to raise interest rate. “I don’t know that I’d call the markets reacting to data an emergency here, because frankly, in my own forecast of looking where inflation was moving, the print was not a surprise,” she said.

Nikkei lost -2.2% on risk aversion, heading back to 26k first

Markets are generally staying in risk-off mode today as there is no sign of de-escalation in Russia-Ukraine situation. Nikkei tumbled sharply by -616.49 pts, or -2.23%, to close at 27079.59.

Near term bearishness in Nikkei remains after rejection by 55 day EMA. The choppy decline from 30795.77 is in progress for retesting 26044.52 low. But, the major line of defense is at 38.2% retracement of 16358.9 to 30795.77 at 25280.61. We’d expect strong support from there to bring rebound.

However, the rejection by 55 week EMA is also a medium term bearish sign, which argues that the fall from 30795.77, as a correction to the up trend from 16358.19, might last longer than originally expected. Indeed, sustained break of 25280.61 could send Nikkei further to the zone between 50% retracement at 23576.98 and 61.8% retracement at 21873.34 before bottoming.

{kind=link}

{kind=link}

New Zealand BNZ services dropped to 45.9, lowest since Oct

New Zealand BusinssNZ Performance of Services index dropped -3.9 to 45.9 in January. That was the lowest result since October 2021. Looking at some details, activity/sales dropped sharply from 50.7 to 44.1. Employment ticked down from 49.1 to 48.1. New orders/businesses dropped deeply from 52.0 to 41.8. Stocks/inventories dropped from 51.0 to 47.6. Supplier deliveries also tumbled from 49.8 to 43.6.

BNZ Senior Economist Craig Ebert said that “the PSI can jag around quite a lot from month to month – upwards and downwards. However, it’s also worth pointing out that the long-term average of the PSI is 53.6, which is starting to feel some distance away. So much for the new traffic light system releasing the brakes on activity.”

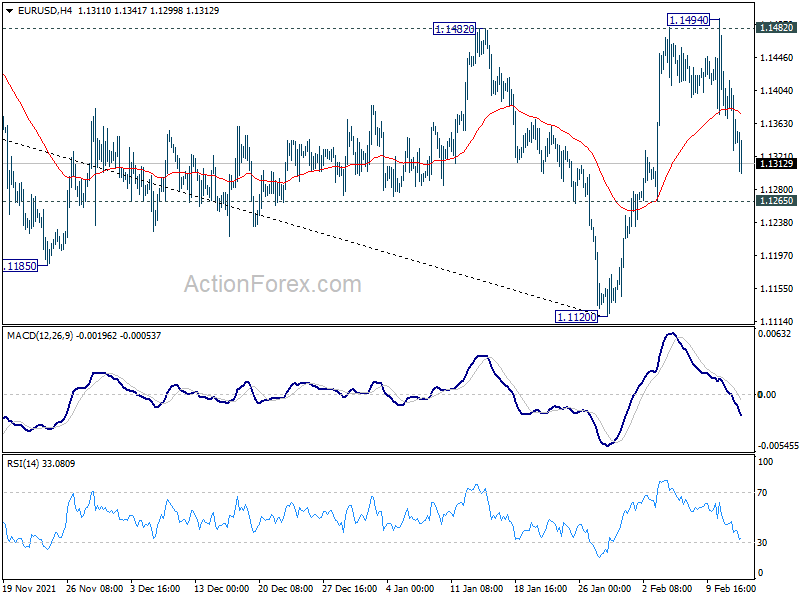

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1308; (P) 1.1370; (R1) 1.1409; More…

Intraday bias in EUR/USD remains neutral and outlook is unchanged. Further rise will remain mildly in favor as long as 1.1265 minor support holds. On the upside break of 1.1482 will target 38.2% retracement of 1.2348 to 1.1120 at 1.1589 next. Sustained break there will argue that whole fall from 1.2348 has completed too and target 61.8% retracement at 1.1879. On the down, however, break of 1.1265 support will dampen this bullish view and bring retest of 1.1120 low instead.

{kind=link}

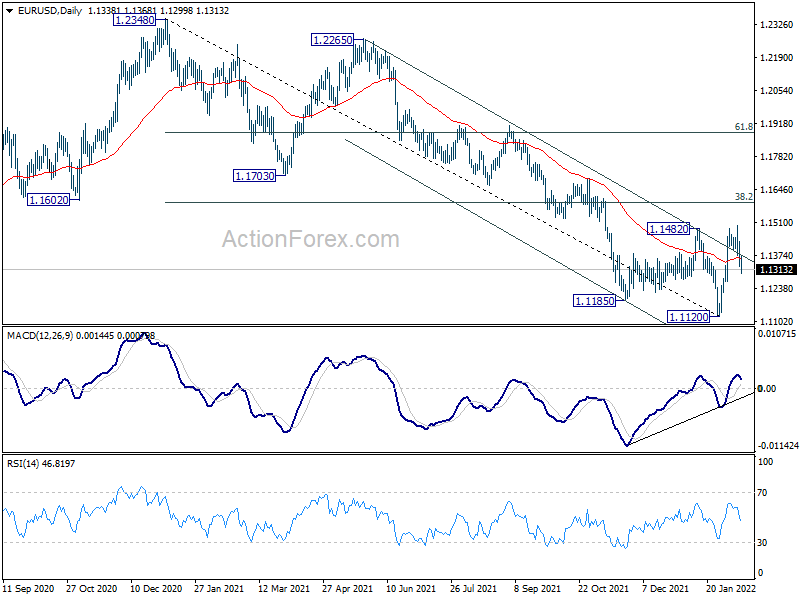

In the bigger picture, the decline from 1.2348 (2021 high) is seen as a leg inside the range pattern from 1.2555 (2018 high). Sustained trading above 55 week EMA (now at 1.1613) will argue that it has completed and stronger rise would be seen back towards top of the range between 1.2348 and 1.2555. However, firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:30 | CHF | Producer and Import Prices M/M Jan | 0.60% | 0.10% | -0.10% | |

| 07:30 | CHF | Producer and Import Prices Y/Y Jan | 5.40% | 5.60% | 5.10% |