Dollar trades broadly lower again today, as pressured by generally positive risk-sentiment. Yen is following as the next weakest. Canadian Dollar is also soft as WTI crude oil is struggling below 90 handle. On the other hand, Australian Dollar and New Zealand Dollar are trading broadly higher. Sterling and Swiss Franc are mixed for now. The US economic calendar is empty today. Investors will likely hold their bet until tomorrow’s US CPI release.

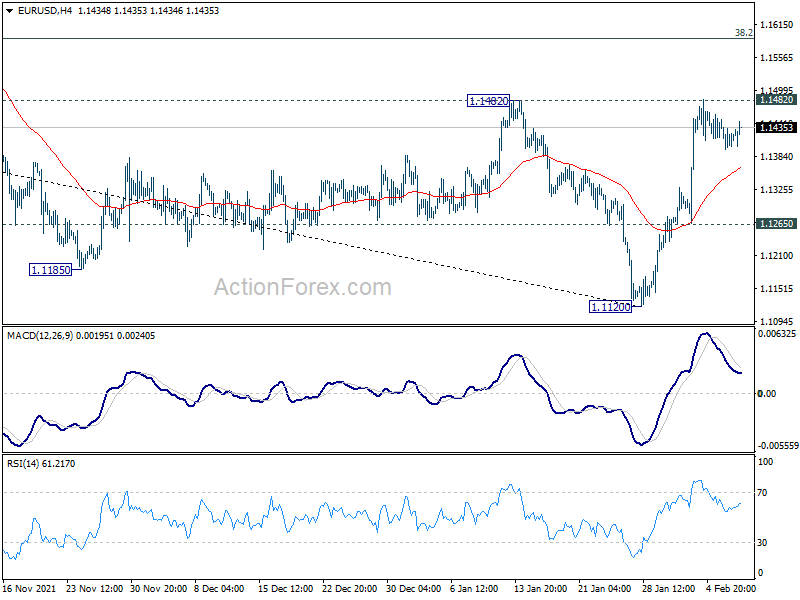

Technically, focus is now back on 1.1482 key resistance in EUR/USD. As noted before, sustained break there will at least confirm medium term bottoming at 1.1120, and raise the chance of bullish trend reversal. Further rally should then be seen to 38.2% retracement of 1.2348 to 1.1120 at 1.1589 next. If this happens, attention will also be on whether EUR/GBP would break through 0.8467 temporary top, and whether EUR/CHF would break through 1.0602 temporary top, to confirm underlying strength of Euro.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.71%. DAX is up 1.59%. CAC is up 1.51%. Germany 10-yaer yield is down -0.044 at 0.223. Earlier in Asia, Nikkei rose 1.08%. Hong Kong HSI rose 2.06%. China Shanghai SSE rose 0.79%. Singapore Strait Times rose 0.54%. Japan 10-year JGB yield rose 0.0003 to 0.208.

Fed Bostic: Let data shows if 25bps or 50bps hike is appropriate

Atlanta Federal Reserve President Raphael Bostic said today on CNBC, “in terms of hikes for the interest rates, right now I have three forecast for this year. I’m leaning a little towards four, but we’re going to have to see how the economy responds as we take our first steps through the first part of this year.”

“For me, I’m thinking very much of a 25-basis-point perspective,” he said. “But I want everyone to understand that every option is on the table, and I don’t want people to have the view that we’re locked into a particular trajectory in terms of how our rates have to move over time. We’re really going to let the data show us to what extent a 50 basis point or 25 basis point move is appropriate.”

BoE Pill: A case can be made for measured rather than activist approach to policy decisions

BoE Chief Economist Huw Pill said in a speech even though the voted for a 25bps hike last week, “given the inflationary pressures we currently face, I can certainly understand why colleagues on the MPC voted for a 50bp hike”.

But, “a case can be made for a measured rather than activist approach to policy decisions, with a focus on more persistent developments in the data that have lasting implications for the outlook for price stability,” he said.

“That is what I would label a ‘steady handed’ approach to monetary policy. Even if it does not provide guidance in all circumstances, I hope it can help explain why I voted for a 25bp hike – rather than something larger – last week.”

Bundesbank Nagel: ECB interest rates could rise this year

In a Die Zeit interview, new Bundesbank President Joachim Nagel said, “if the (inflation) picture does not change by March, I will advocate normalizing monetary policy.” “The first step is to end net bond purchases during 2022,” he said. “Then interest rates could rise this year.”

Nagel also expects inflation in Germany to rise “significantly” above 4% in 2022. He warned that the economic costs of acting too late on inflation are significantly higher than acting early.

BoJ Nakamura: Conditions not fallen into place for modifying monetary policy

BoJ board member Toyoaki Nakamura said, “I don’t think conditions have fallen into place for Japan to modify monetary policy.” He warned, “if we raise interest rates now or before wages pick up, we would be taking away from companies money that would otherwise have been used to raise pay.”

He added, “we’ll patiently maintain our ultra-easy monetary policy until wages begin to rise sustainably.”

“For companies, what’s most important is for currency rates to move stably. If the dollar/yen moves within the current range (of around 103-115), that will make it easier for companies to make business decisions,” he added.

Australia Westpac consumer sentiment dropped to 100.8, elevated pressures on finances

Australia Westpac-Melbourne Institute consumer sentiment dropped -1.3% to 100.8 in February, down from 102.2. The “economy, next 12 months” sub-index increased by 2.4% and the “economy, next 5 years” sub-index was up by 1.5%.

However, the “finances vs a year ago” sub-index slumped by -9.2% (more than reversing the surprise 7.5% lift in January) while the “finances, next 12 months” sub-index fell by -1.5% to be down by -4.3% since December.

Westpac said, “the most likely explanations for these elevated pressures on finances relate to: Omicron-related disruptions to activity and earnings at the start of the year; the rising cost of living; and the prospect of rising interest rates.”

Also, Westpac does not expect the first rate hike by the RBA until August and it will be very interesting to observe how resilient this surprising recovery in confidence will be in the lead up to the first move.”

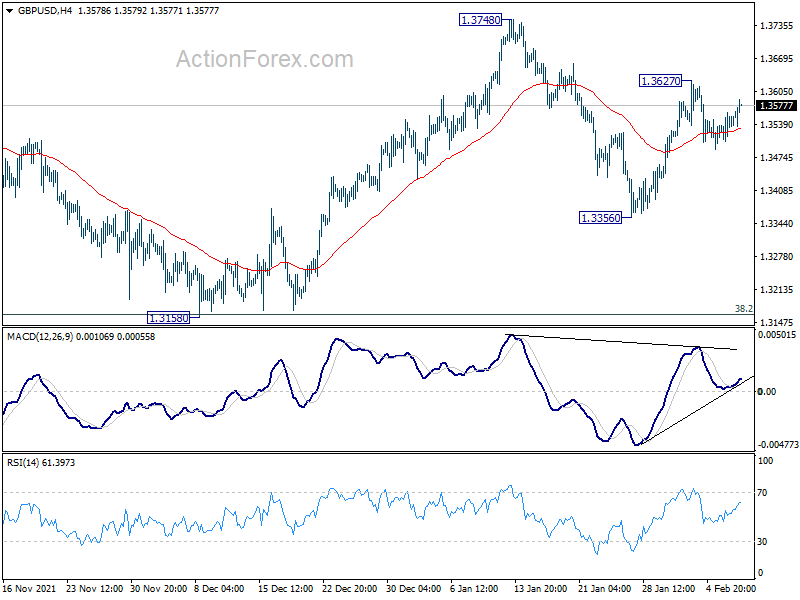

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3516; (P) 1.3540; (R1) 1.3572; More…

Intraday bias in GBP/USD remains neutral and outlook is unchanged. On the upside, break of 1.3627 will resume the rebound to 1.3748 resistance. Firm break there will revive the bullish case that correction from 1.4248 has completed with three waves down to 1.3158. Further rally should then be seen to retest 1.4248 high. On the downside, however, break of 1.3356 will bring retest of 1.3158 low.

{kind=link}

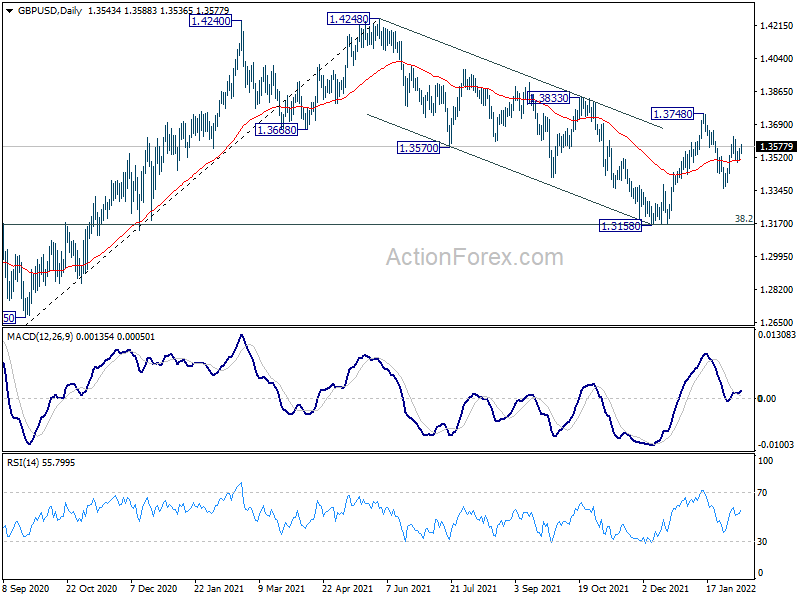

In the bigger picture, as long as 38.2% retracement of 1.1409 to 1.4248 at 1.3164 holds, up trend from 1.1409 (2020 low) is still in progress. On resumption, next target will be 38.2% retracement of 2.1161 to 1.1409 at 1.5134. Nevertheless sustained break of 1.3164 will argue that whole rise from 1.1409 has completed and bring deeper fall to 61.8% retracement at 1.2493.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Feb | -1.30% | -2% | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Jan | 3.60% | 3.50% | 3.70% | |

| 07:00 | EUR | Germany Trade Balance (EUR) Dec | 6.8B | 11.3B | 10.9B | |

| 09:00 | EUR | Italy Industrial Output M/M Dec | -1.00% | 1.70% | 1.90% | |

| 15:00 | USD | Wholesale Inventories Dec F | 2.00% | 2.10% | ||

| 15:30 | USD | Crude Oil Inventories | 1.5M | -1.0M |