Canadian Dollar is currently the weakest one for today, following the pull back in oil prices. Japanese Yen is following as European and US yields are apparently trying to outpace benchmark JGB yield again. On the other hand, Aussie is trading slightly firmer, together with Kiwi and Dollar. Euro is paring some of the post-ECB gains, but the retreats are relatively shallow so far.

Technically, WTI crude oil is now pressing 4 hour 55 EMA (now at 89.20), which is close to the short term channel support. Sustained break there will argue that it’s already in correction to rise from 66.46 or even that from 62.90. In such case, deeper pull back would be seen back to 82.42/87.70 to set up the base for rebound. If happens, Canadian Dollar could be dragged further down.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.10%. DAX is down -0.03%. CAC is up 0.23%. Germany 10-year yield is up 0.022 at 0.249. Earlier in Asia, Nikkei rose 0.13%. Hong Kong HSI dropped -1.02%. China Shanghai SSE rose 0.67%. Singapore Strait Times rose 1.05%. Japan 10-year JGB yield rose 0.0079 to 0.208.

US trade deficit up slightly to USD 80.7B, deficit with China widened

US exports of goods and services rose 1.5% to USD 228.1B in December. Imports rose 1.6% mom to USD 308.9B. Trade deficit came in at USD 80.7B, smaller than expectation of USD 83.0B.

The deficit with China increased USD 6.0B to USD 34.1B. Exports decreased USD 2.2B to USD 11.8B and imports increased USD 3.8B to USD 45.9B.

The deficit with the European Union decreased USD 3.0B to USD 16.3 B in December. Exports increased USD 0.7B to USD 25.1B and imports decreased USD 2.4B to USD 41.4B.

Canada imports rose 3.7% in December while exports dropped -0.9%. Merchandise trade balance returned to a deficit position of CAD 137m.

ECB de Cos: Uncertainty around inflation very high due to geopolitical risks

ECB Governing Council member Pablo Hernandez de Cos said “risks to inflation are tilted to the upside in the short term.” Recent data on Recent data on inflation has shown surprising upwards trends both in headline inflation and core inflation. He added, that the level of uncertainty around inflation is very high also due to geopolitical risks.

De Cos emphasized that more than ever it is necessary to keep all options open on monetary policy. But for now, ECB policymakers are sticking to the sequencing, starting first with tapering, before raising interest rate.

He added, that the next move on monetary policy is clear but will be gradual and depend on data.

Australia NAB business confidence rose to 3 in Jan, strong recovery expected

Australia NAB business confidence rose from -12 to 3 in January, turned positive. Business conditions, however, dropped from 8 to 3. Looking at some details, trading conditions dropped from 14 to 7. Profitability conditions dropped from 10 to 2. Employment conditions dropped from 2 to -1 and turned negative.

“Overall, the January survey shows significant disruption to business activity from the spread of the Omicron variant, albeit impacts on businesses were less severe than in past outbreaks,”said NAB Group Chief Economist Alan Oster. “However, we continue to expect a strong recovery as case numbers come down.”

RBNZ Orr: An innovative approach needed to support a more efficient and resilient cash system

RBNZ is currently commencing Central Bank Digital Currency (CBDC) proof-of-concept design work, which is a “multi-stage and multi-year effort”. The consultation on an issues paper Future of Money – Cash System Redesign, which closes on March 7, received 190 submissions so far.

Governor Adrian Orr said in a speech, “we must decide how best to use of digital technology to modernize central bank money, while we continue to ensure cash remains an option for those who need it. An innovative approach is needed to support a more efficient and resilient cash system, and the changes required are potentially far reaching”.

“The technology exists now to implement a CBDC, but it needs to be well designed. At a basic hygiene level, a CBDC must be user-friendly, resilient to cyber and other operational risks, and enable privacy. These features promote widespread trust and use.”

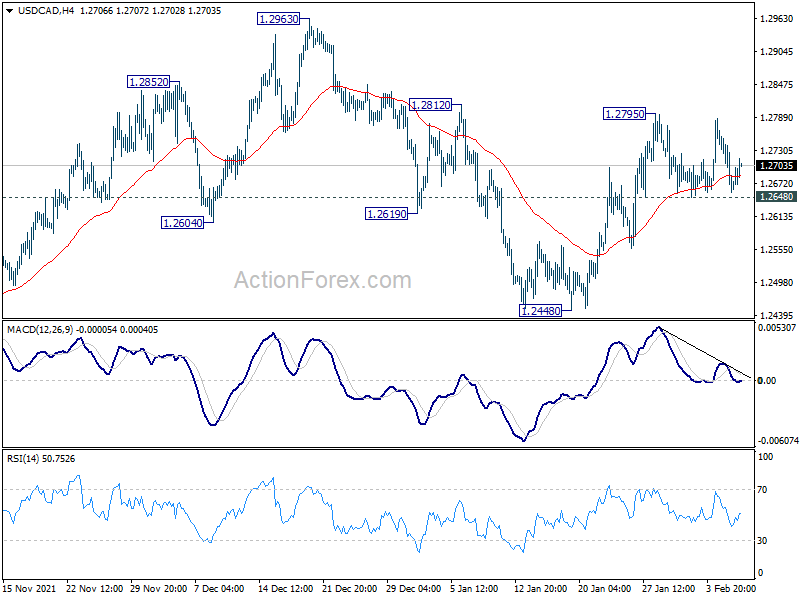

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2633; (P) 1.2694; (R1) 1.2731; More…

USD/CAD recovers mildly but stays in range of 1.2648/2795. Intraday bias remains neutral for the moment. With 1.2648 minor support intact, further rise is mildly in favor. On the upside, break of 1.2795 will resume the rally from 1.2448 to 1.2963 resistance next. However, break of 1.2648 will turn bias back to the downside for 1.2448 support instead.

{kind=link}

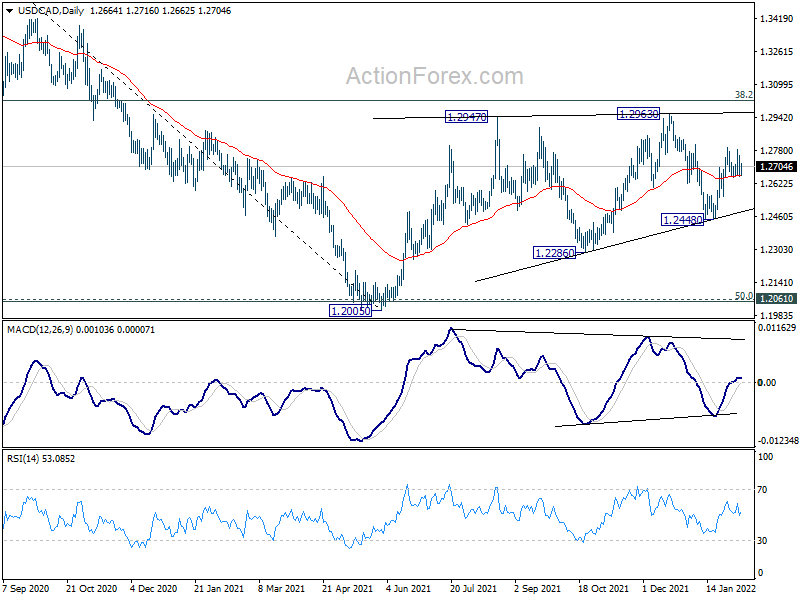

In the bigger picture, focus stays on 38.2% retracement of 1.4667 (2020 high) to 1.2005 (2021 low) at 1.3022. Sustained break there should confirm that the down trend from 1.4667 has completed after defending 1.2061 long term cluster support. Further rise would then be seen towards 61.8% retracement at 1.3650. However, rejection by 1.3022 will maintain medium term bearishness. Break of 1.2005 will resume the down trend from 1.4667 and that carries larger bearish implications too.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Dec | -0.20% | 0.90% | 0.80% | |

| 23:30 | JPY | Household Spending Y/Y Dec | -0.20% | 0.30% | -1.30% | |

| 23:50 | JPY | Bank Lending Y/Y Jan | 0.60% | 0.80% | 0.60% | |

| 23:50 | JPY | Current Account (JPY) Dec | 0.79T | 1.16T | 1.37T | |

| 00:30 | AUD | NAB Business Confidence Jan | 3 | -12 | ||

| 00:30 | AUD | NAB Business Conditions Jan | 3 | 8 | ||

| 05:00 | JPY | Eco Watchers Survey: Current Jan | 37.9 | 49.3 | 56.4 | |

| 07:45 | EUR | France Trade Balance (EUR) Dec | -11.3B | -9.1B | -9.7B | -9.8B |

| 09:00 | EUR | Italy Retail Sales M/M Dec | 0.90% | 0.30% | -0.40% | |

| 11:00 | USD | NFIB Business Optimism Index Jan | 97.1 | 97.7 | 98.9 | |

| 13:30 | USD | Trade Balance (USD) Dec | -80.7B | -83.0B | -80.2B | -79.3B |

| 13:30 | CAD | Trade Balance (CAD) Dec | -0.1B | 3.6B | 3.1B |