Dollar strengthens mildly in Asia today but overall markets have been quiet this week so far. Euro continues to consolidate last week’s sharp gain, ahead of a key near term resistance against the greenback. Commodity currencies are the slightly stronger ones. Major benchmark global treasury yields continue to rally while stocks tread water. There might not be clear directions in the markets until US consumer inflation data later in the week.

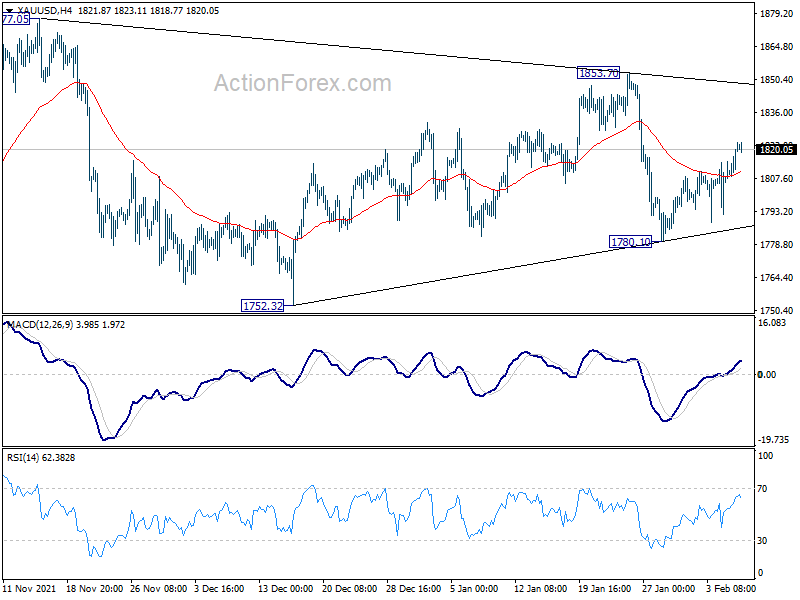

Technically, Gold’s recovery from 1780.10 was admittedly stronger than expected, even though upside momentum is unconvincing. Despite the steepness of the fall from 1853.70 to 1780.10, Gold is not ready to breakout to the downside. Instead, current development suggest that it’s recent price actions were just forming a symmetric triangle pattern. Some more time is needed to break out from range of 1780.10/1853.70. But such breakout could reveal which direction the greenback is taking too.

{kind=link}

In Asia, at the time of writing, Nikkei is up 0.24%. Hong Kong HSI is down -1.56%. China Shanghai SSE is down -0.39%. Singapore Strait Times is up 0.61%. Japan 10-year JGB yield is up 0.012 at 0.212. Overnight, DOW rose 0.00%. S&P 500 dropped -0.37%. NASDAQ dropped -0.58%. 10-year yield dropped -0.014 to 1.916.

Australia NAB business confidence rose to 3 in Jan, strong recovery expected

Australia NAB business confidence rose from -12 to 3 in January, turned positive. Business conditions, however, dropped from 8 to 3. Looking at some details, trading conditions dropped from 14 to 7. Profitability conditions dropped from 10 to 2. Employment conditions dropped from 2 to -1 and turned negative.

“Overall, the January survey shows significant disruption to business activity from the spread of the Omicron variant, albeit impacts on businesses were less severe than in past outbreaks,”said NAB Group Chief Economist Alan Oster. “However, we continue to expect a strong recovery as case numbers come down.”

RBNZ Orr: An innovative approach needed to support a more efficient and resilient cash system

RBNZ is currently commencing Central Bank Digital Currency (CBDC) proof-of-concept design work, which is a “multi-stage and multi-year effort”. The consultation on an issues paper Future of Money – Cash System Redesign, which closes on March 7, received 190 submissions so far.

Governor Adrian Orr said in a speech, “we must decide how best to use of digital technology to modernize central bank money, while we continue to ensure cash remains an option for those who need it. An innovative approach is needed to support a more efficient and resilient cash system, and the changes required are potentially far reaching”.

“The technology exists now to implement a CBDC, but it needs to be well designed. At a basic hygiene level, a CBDC must be user-friendly, resilient to cyber and other operational risks, and enable privacy. These features promote widespread trust and use.”

Elsewhere

Japan labor cash earnings dropped -0.2% yoy in December versus expectation of 0.9% yoy. Household spending dropped -0.2% yoy versus expectation of 0.3% yoy. Current account surplus narrowed to JPY 0.79T in December, versus expectation of JPY 1.16T.

Looking ahead, France trade balance and Italy retail sales will be released in European session. Later in the day, both US and Canada will release trade balance.

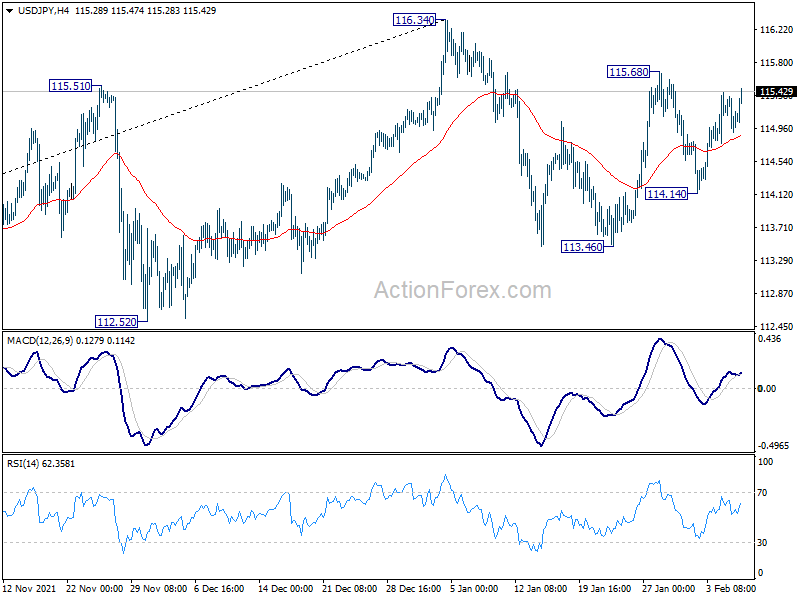

USD/JPY Daily Outlook

Daily Pivots: (S1) 114.89; (P) 115.13; (R1) 115.35; More…

USD/JPY rises slightly today but stays in range of 114.14/115.68, and intraday bias remains neutral first. Overall, consolidation pattern from 116.34 is still extending. On the upside, break of 115.68 will resume the rebound from 113.46 to retest 116.34 high first. On the downside, break of 114.14 should extend the consolidation with another falling leg through 113.46 support.

{kind=link}

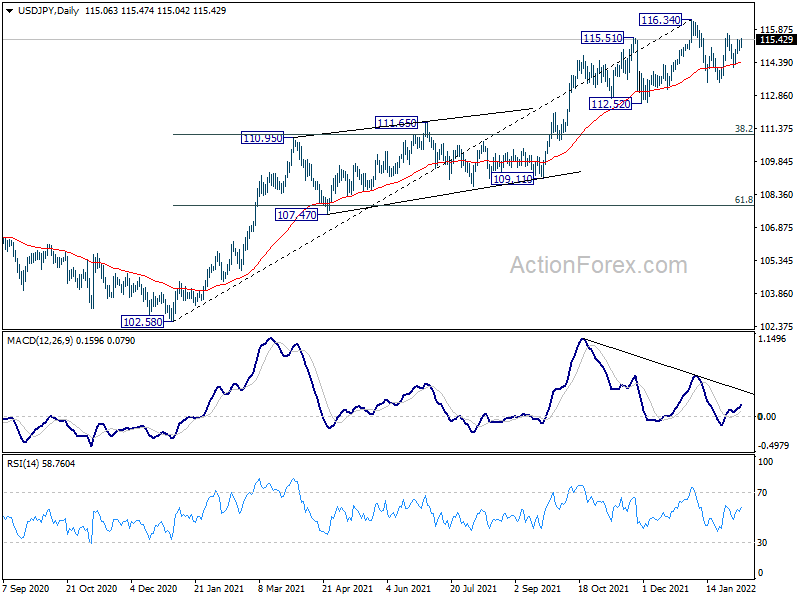

In the bigger picture, no change in the view that rise from 102.58 is the third leg of the up trend from 101.18 (2020 low). Such rally should target a test on 118.65 (2016 high). Sustained break there will pave the way to 120.85 (2015 high) and raise the chance of long term up trend resumption. This will remain the favored case as long as 55 week EMA (now at 111.21) holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Dec | -0.20% | 0.90% | 0.80% | |

| 23:30 | JPY | Household Spending Y/Y Dec | -0.20% | 0.30% | -1.30% | |

| 23:50 | JPY | Bank Lending Y/Y Jan | 0.60% | 0.80% | 0.60% | |

| 23:50 | JPY | Current Account (JPY) Dec | 0.79T | 1.16T | 1.37T | |

| 00:30 | AUD | NAB Business Confidence Jan | 3 | -12 | ||

| 00:30 | AUD | NAB Business Conditions Jan | 3 | 8 | ||

| 05:00 | JPY | Eco Watchers Survey: Current Jan | 37.9 | 49.3 | 56.4 | |

| 07:45 | EUR | France Trade Balance (EUR) Dec | -9.1B | -9.7B | ||

| 09:00 | EUR | Italy Retail Sales M/M Dec | 0.30% | -0.40% | ||

| 11:00 | USD | NFIB Business Optimism Index Jan | 97.7 | 98.9 | ||

| 13:30 | USD | Trade Balance (USD) Dec | -83.0B | -80.2B | ||

| 13:30 | CAD | Trade Balance (CAD) Dec | 3.6B | 3.1B |