The forex markets are generally steady in Asian session, as traders await ECB and BoE rate decisions. Dollar is staying as the weakest for the week one after yesterday’s selloff, followed by Yen. Aussie and Euro are the strongest ones. There is upside prospect for Euro even if ECB delivers just a slight hawkish tilt. But that’s far from being certain. Meanwhile, the greenback will continue to look into the developments in overall market sentiments, as well as ISM services today and non-farm payroll report tomorrow.

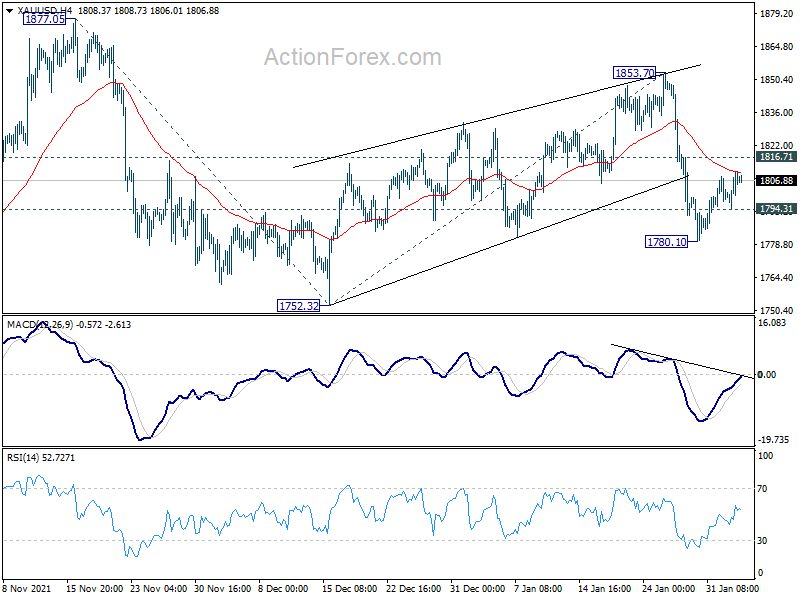

Technically, it should be about time for Gold to complete the recovery from 1780.10, as it touches 4 hour 55 EMA while 4 hour MACD is approaching trend line. Break of 1794.31 minor support will suggest that fall from 1853.70 is ready to resume through 1780.10 to 1753.32 low. However, firm break of 1816.71 minor resistance will put 1853.70 back into focus. The move in Gold will again be used to confirm the underlying momentum in Dollar’s next move.

{kind=link}

In Asia, at the time of writing, Nikkei is down -0.98%. Japan 10-year JGB yield is up 0.0073 at 0.186. Hong Kong and China are still on holiday. Overnight, DOW rose 0.63%. S&P 500 rose 0.94%. NASDAQ rose 0.50%. 10-year yield dropped -0.034 to 1.766.

BoC Macklem: It will be a series of increases, not a single increase

BoC Governor Tiff Macklem told the Senate banking committee yesterday that inflation could stay “uncomfortably high” around 5% over the first half of 2022, and then “coming down fairly quickly in the second half.”

However, “there is some uncertainty about how quickly inflation will come down because we’ve never experienced a pandemic like this before.”

“It’s clear that interest rates need to be on a rising path,” Macklem said. “The slope of that path is going to depend on economic developments, and if consumers spend more, the slope of that path, likely, has to be steeper.”

“It will be a series of increases, not a single increase,” he said.

BoJ Wakatabe: Definitely too early to start tightening

BoJ Deputy Governor Masazumi Wakatabe said in a speech, “given the current situation where Japan’s economy has finally started to pick up from the pandemic, it is definitely too early for the Bank to start tightening monetary policy when the target has not yet been achieved as this could hinder the economic recovery.”

He reiterated the current policy as to continue with QQE with yield curve control, “as long as it is necessary” to maintain 2% inflation target in a “stable manner”. That is, CPI should remain at 2% while medium- to long-term inflation expectations are “anchored”.

Australia NAB business confidence rose to 18 in Q4

Australia NAB business confidence jumped from -2 to 18 in Q4. Current business conditions was unchanged at 12. Conditions for the next 3 months rose from 8 to 30. Conditions for the next 12 months also rose from 26 to 34. Capex plans rose from 26 to 34.

“The economy was showing considerable strength prior to the spread of the Omicron variant, and that translated into a positive outlook for the coming months,”Alan Oster, NAB Group Chief Economist. “We now know that Omicron has dampened that recovery somewhat but, fundamentally, we expect that positive trajectory to continue when the current virus outbreak recedes.”

Also released, goods and services export rose 1% mom to AUD 45.32B in December. Goods and services imports rose 5% mom to AUD 36.96B. Trade surplus narrowed to AUD 8.36B, below expectation of AUD 9.80B. AiG Performance of Construction index dropped from 57 to 45.9 in December. Building permits rose 8.2% mom in December.

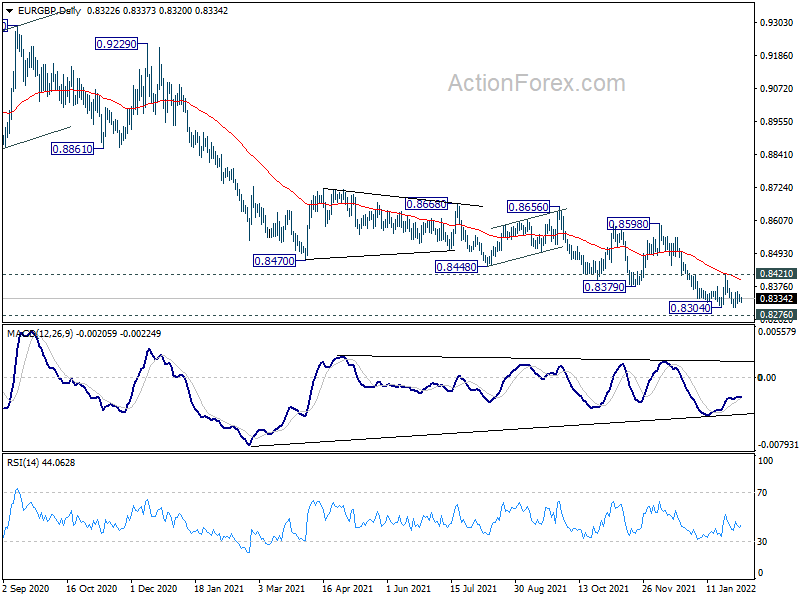

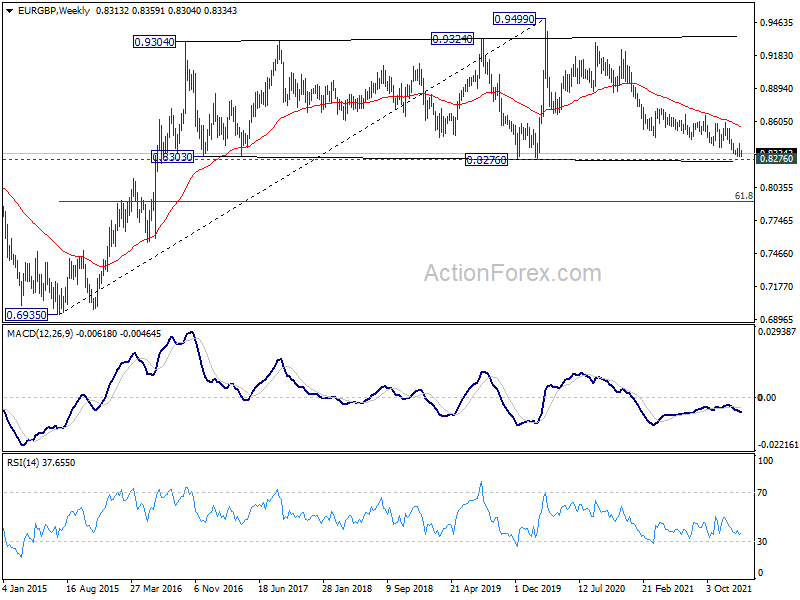

BoE and ECB previews, a look at EUR/GBP

Two central banks will announce monetary policy decisions today. BoE is generally expected to deliver a back-to-back rate hike and raise Bank Rate by 25bps to 0.50%. The central bank would also reveal the approach to wind down the GBP 895B asset purchases. Looking ahead, more tightening is expected ahead to bring the Bank Rate to 1.00% level by the end of the year. That should be reflected in the new economic projections in the Monetary Policy Summary.

On the other hand, ECB is expected to stand pat and maintain a cautious tone even though inflation surged to another record in January. Markets are seeing the first rate hike, at 10bps, by July. But President Christine Lagarde would likely talk down such expectations.

Here are some previews on ECB and BoE:

EUR/GBP is a pair to watch today. It should be noted that it’s now very close to a key long term support level at 0.8276, with bullish convergence condition in daily MACD. The conditions are there for a trend reversal. Break of 0.8421 resistance will complete a small double bottom pattern (0.8304, 0.8304), and bring stronger rebound. Further break of 0.8598 resistance should confirm medium term bottoming and turn outlook bullish.

However, sustained break of 0.8276 would argue that fall from 0.9499 is developing into a long term down trend rather than a correction. Deeper decline would then be seen for the rest of the year towards 61.8% retracement of 0.6935 to 0.9499 at 0.7917, and possibly below.

EUR/GBP is now at a juncture.

{kind=link}

{kind=link}

Looking ahead

Eurozone will release PMI services final and PPI. UK will release PMI services final. Main focuses will be on BoE and ECB rate decisions.

Later in the day, US will release jobless claims, non-farm productivity, ISM services and factory orders.

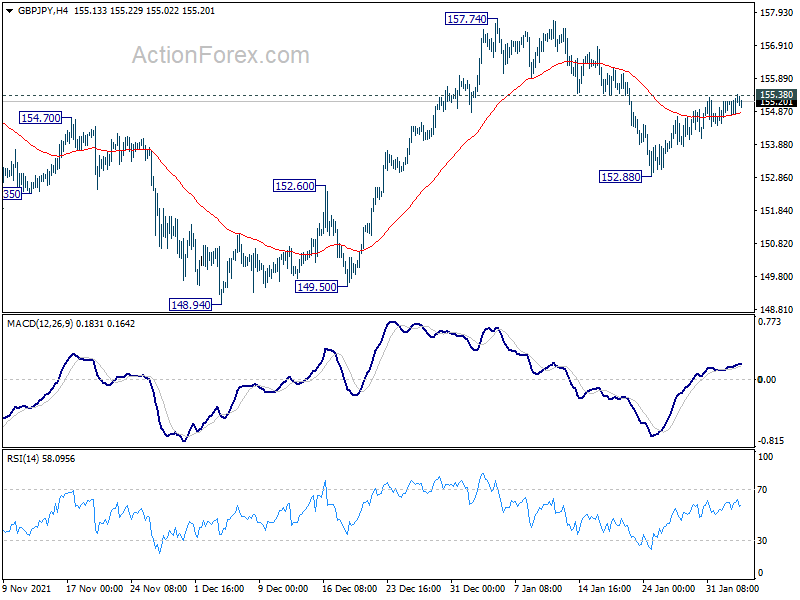

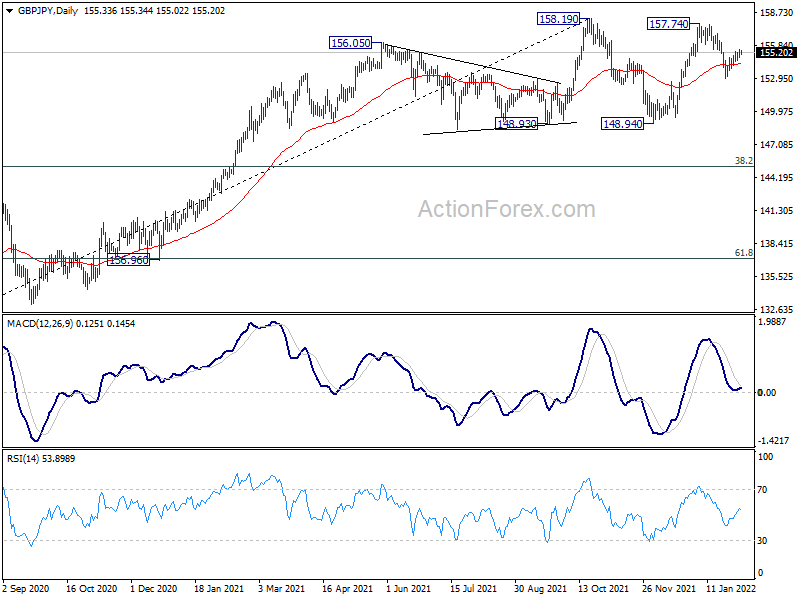

GBP/JPY Daily Outlook

Daily Pivots: (S1) 154.95; (P) 155.19; (R1) 155.57; More…

GBP/JPY is staying in consolidation from 152.88 and intraday bias remains neutral. Further fall is still in favor with 155.38 minor resistance intact. Break of 152.88 will resume the decline from 157.74, as the third leg of the corrective pattern from 158.19, to 148.93 support next. However, sustained break of 155.38 will dampen this view and flip bias back to the upside for 157.74/158.19 resistance zone instead.

{kind=link}

In the bigger picture, price actions from 158.19 are currently seen as developing into a consolidation pattern to up trend from 123.94 (2020 low). Downside should be contained by 123.94 to 158.19 at 145.10 to bring rebound. Firm break of 158.19 will resume the up trend to long term fibonacci level at 167.93. However, sustained break of 145.10 will raise the chance of trend reversal and target 61.8% retracement at 137.02.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Dec | 45.9 | 57 | ||

| 00:30 | AUD | Building Permits M/M Dec | 8.20% | -0.90% | 3.60% | 2.60% |

| 00:30 | AUD | Trade Balance (AUD) Dec | 8.36B | 9.80B | 9.42B | 9.76B |

| 08:50 | EUR | France Services PMI Jan F | 53.1 | 53.1 | ||

| 08:55 | EUR | Germany Services PMI Jan F | 52.2 | 52.2 | ||

| 09:00 | EUR | Eurozone Services PMI Jan F | 51.2 | 51.2 | ||

| 09:30 | GBP | Services PMI Jan F | 53.5 | 53.3 | ||

| 10:00 | EUR | Eurozone PPI M/M Dec | 3.00% | 1.80% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Dec | 26.60% | 23.70% | ||

| 12:00 | GBP | BoE Interest Rate Decision | 0.50% | 0.25% | ||

| 12:00 | GBP | BoE Asset Purchase Facility | 895B | 895B | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | 7–0–2 | 8–0–1 | ||

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–9 | 0–0–9 | ||

| 12:30 | USD | Challenger Job Cuts Y/Y Jan | -75.30% | |||

| 12:45 | EUR | ECB Interest Rate Decision | 0.00% | 0.00% | ||

| 13:30 | EUR | ECB Press Conference | ||||

| 13:30 | USD | Initial Jobless Claims (Jan 28) | 264K | 260K | ||

| 13:30 | USD | Nonfarm Productivity Q4 P | 2.80% | -5.20% | ||

| 13:30 | USD | Unit Labor Costs Q4 P | 1.50% | 9.60% | ||

| 14:45 | USD | Services PMI Jan F | 50.9 | 50.9 | ||

| 14:45 | USD | PMI Composite Jan | 50.8 | 50.8 | ||

| 15:00 | USD | ISM Services Prices Paid Jan | 83 | 82.5 | ||

| 15:00 | USD | ISM Services PMI Jan | 58.7 | 62 | ||

| 15:00 | USD | Factory Orders M/M Dec | 0.10% | 1.60% | ||

| 15:30 | USD | Natural Gas Storage | -280B | -219B |