The markets are generally steady in Asian session. Dollar is paring some recent gains while Yen and Swiss Franc soften. Trading in Asia would likely be subdue for the next few days on Lunar New Year holidays. But volatility is anticipated in the week as a whole considering the massive amount of key events featured, including three central bank meetings as well ass heavy weight data like non-farm payrolls.

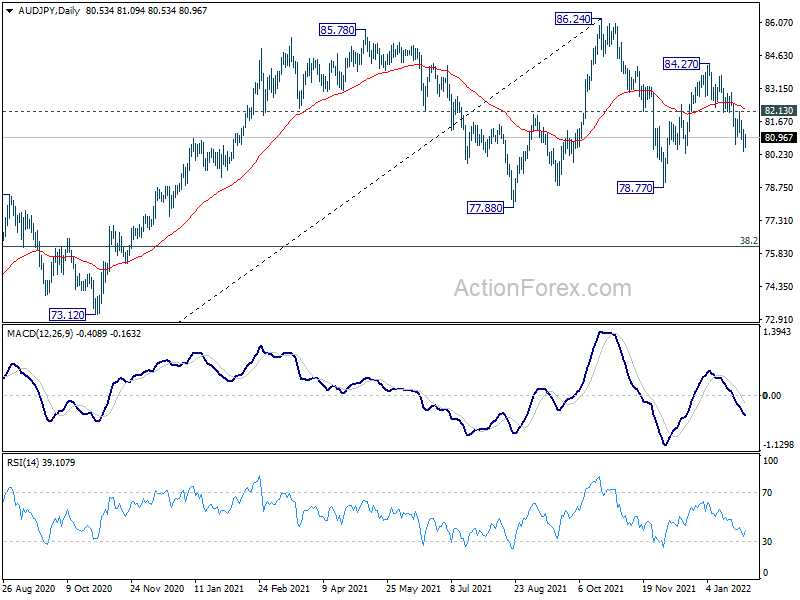

Technically, AUD/USD is now trying to defend 0.7 handle, with 0.6991 key structural support. Sustained break there will argue that recent fall from 0.8006 is more of a medium term impulsive down trend then a corrective move. Selloff in AUD/USD could also be accompanied by a corresponding move in AUD/JPY. Break of 78.77 support will complete a head and shoulder top pattern (ls: 85.78, h: 86.24, rs: 84.27) which is also medium term bearish. The development will very much depend on what RBA is going to deliver tomorrow.

{kind=link}

In Asia, at the time of writing, Nikkei is up 1.27%. Hong Kong HSI is up 1.07%. China Shanghai SSE is down -0.97%. Singapore Strait Times is up 0.10%. Japan 10-year JGB yield is up 0.0106 at 0.179.

Fed Bostic comfortable with 50bps or if data support

Atlanta Fed President Raphael Bostic said in an FT interview that “every option is on the table” for every FOMC meeting. “If the data say that things have evolved in a way that a 50 basis point move is required or [would] be appropriate, then I’m going to lean into that . . . If moving in successive meetings makes sense, I’ll be comfortable with that,” he said.

“The reduction of accommodation should translate into tighter financial markets,” Bostic said. “The developments that we’ve seen on that front are comforting in the sense that markets are still functioning the way they’re supposed to, and they are responding to conditions in ways that are rational and appropriate.” He also supports starting the runoff of the USD 9T balance sheet “as quickly as” possible without impairing market functioning.

“Our policy path is not a constriction path. It’s a less accommodative path,” he said. “If we do the three [rate hikes] that I have in mind, that’ll still leave our policy in a very accommodative space. “I don’t think there’s going to be a lot of constraint on growth as we remove these emergency actions.”

Japan industrial production dropped -1.0% mom in Dec, expected to rebound in Jan and Feb

Japan industrial production dropped -1.0% mom in December, worse than expectation of -0.8% mom. Manufacturers surveyed by the Ministry of Economy, Trade and Industry (METI) expected output to grow 5.2% in January and 2.2% in February.

Retail sales grew 1.4% yoy in December, below expectation of 2.7% yoy. That’s nonetheless the third straight month of increase for sales, lifted by demand for general merchandise and food and beverages. Housing starts rose 4.2% yoy in December, versus expectation of 7.1% yoy. Consumer confidence dropped from 39.1 to 36.7, below expectation of 37.3.

China Caixin PMI manufacturing dropped to 49.1, straining under the triple pressures

China Caixin PMI Manufacturing dropped from 50.9 to 49.1 in January. That’s the worst reading in 23 months. Also, the index slumped into negative territory for the fourth time since February 2020.

Wang Zhe, Senior Economist at Caixin Insight Group said: “From December to January, the resurgence of Covid-19 in several regions including Xi’an and Beijing forced local governments to tighten epidemic control measures, which restricted production, transportation and sales of manufactured goods. It became more evident that China’s economy is straining under the triple pressures of contracting demand, supply shocks and weakening expectations.”

RBA, BoE and ECB; US ISMs and NFP

Three central banks will meet this week. Given the surprise drop in unemployment and strong inflation data, RBA is likely to just wrap up the QE program, rather than winding it down to end in May. That would also give the central bank some flexibility to raise interest rate to combat inflation. The question is how RBA would shape market expectation on the timing of the rate hike, or leave it to the Statement on Monetary Policy to be released later in the week.

BoE is expected to deliver another hike to bring the Bank Rate to 0.50%. Back in August, the central bank indicated in will start reducing its balance sheet once the policy rate hits 0.50%. So, so sort of announcement on this topic is expected. Additionally, the Monetary Policy Report would provide guidance on the path of rate hikes ahead too.

ECB’s meeting would likely be a lackluster one. No change in policy is expected. It will also reiterate that inflation is going to ease along the course of the year. President Christine Lagarde could also try to talk down the prospect of a rate hike this year.

Here are some suggested readings:

The data calendar is also extremely busy, with US ISMs and NFP, Eurozone GDP and unemployment rate, Canada GDP and employment, Australia retail sales, New Zealand employment featured. Here are some highlights for the week:

- Monday: Japan industrial production, retail sales, consumer confidence, housing starts; Eurozone GDP; Canada IPPI and RMPI; US Chicago PMI.

- Tuesday: Australia AiG manufacturing, retail sales, RBA rate decision; New Zealand trade balance; Japan unemployment rate, PMI manufacturing final; Germany retail sales, unemployment; Swiss retail sales, SECO consumer climate, PMI manufacturing; Eurozone PMI manufacturing final, unemployment rate; UK PMI manufacturing final; Canada GDP, PMI manufacturing; US ISM manufacturing, construction spending.

- Wednesday: New Zealand employment change, labor cost index; Japan monetary base; Eurozone CPI flash; US ADP employment; Canada building permit.

- Thursday: Australia AiG construction; Australia building approvals, NAB business confidence, trade balance; Eurozone PMI services final, ECB rate decision; UK PMI manufacturing final, BoE rate decision; US jobless claims, non-farm productivity, ISM services, factory orders.

- Friday: RBA monetary policy statement; Germany factory orders; France industrial production; UK PMI construction; Eurozone retail sales; Canada employment, Ivey PMI; US non-farm payroll employment.

EUR/GBP Daily Outlook

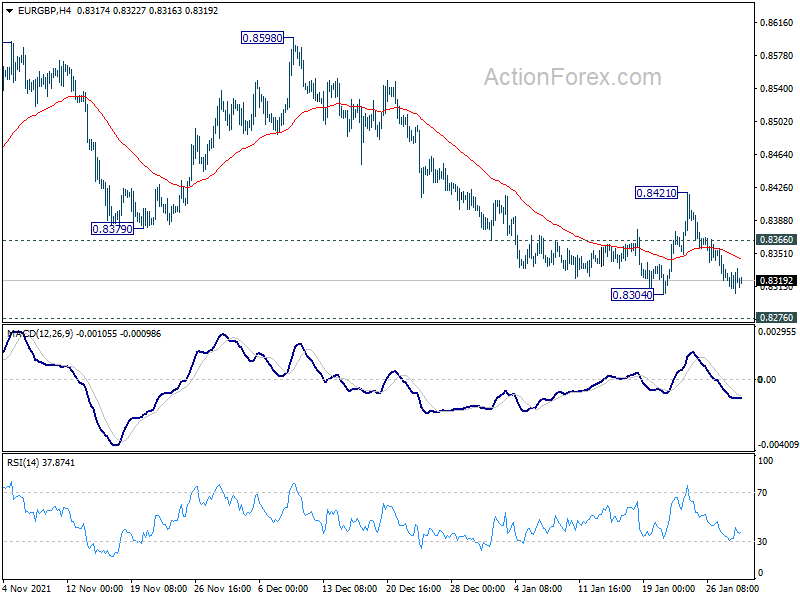

Daily Pivots: (S1) 0.8307; (P) 0.8321; (R1) 0.8335; More…

Intraday bias sin EUR/GBP remains mildly on the downside at this point. Break of 0.8304 will resume larger down trend to 0.8276 key long term support. On the upside, above 0.8366 minor resistance will turn bias back to the upside for 0.8421 resistance first. Break there will bring stronger rally back to 0.8598 resistance.

{kind=link}

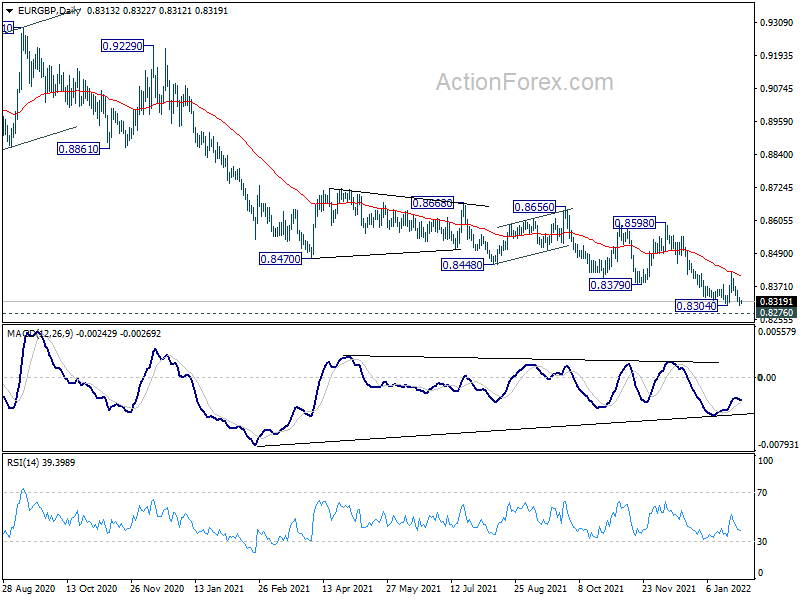

In the bigger picture, price actions from 0.9499 (2020 high) are still seen as developing into a corrective pattern. Deeper fall could be seen as long as 0.8598 resistance holds, towards long term support at 0.8276. We’d look for bottoming signal around there to bring reversal. Meanwhile, firm break of 0.8598 will now be an early sign of medium term bottoming and bring stronger rebound. However, sustained break of 0.8276 will argue that the long term trend has reversed.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Dec P | -1.00% | -0.80% | 7.00% | |

| 23:50 | JPY | Retail Trade Y/Y Dec | 1.40% | 2.70% | 1.90% | |

| 00:30 | AUD | Private Sector Credit M/M Dec | 0.80% | 0.70% | 0.90% | 1.00% |

| 05:00 | JPY | Housing Starts Y/Y Dec | 4.20% | 7.10% | 3.70% | |

| 05:00 | JPY | Consumer Confidence Index Jan | 36.7 | 37.3 | 39.1 | |

| 09:00 | EUR | Italy GDP Q/Q Q4 P | 0.50% | 2.60% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | 0.40% | 2.20% | ||

| 13:00 | EUR | Germany CPI M/M Jan P | -0.30% | 0.50% | ||

| 13:00 | EUR | Germany CPI Y/Y Jan P | 4.30% | 5.30% | ||

| 13:30 | CAD | Industrial Product Price M/M Dec | 0.80% | 0.80% | ||

| 13:30 | CAD | Raw Material Price Index Dec | 0.60% | -1.00% | ||

| 14:45 | USD | Chicago PMI Jan | 62.5 | 63.1 |