Dollar is making a strong come back in Asian session today, as 10-year yield powers up to 1.85 level. Yen is under some selling pressure after BoJ stood pat as expected, and delivered little surprise other than upgrades in inflation forecasts. But Aussie and Kiwi are currently the weakest one. Canadian Dollar, on the other hand, in the second strongest, with WTI crude oil extending recent rise to 85 handle. European majors are mixed with Sterling having a slight upper hand.

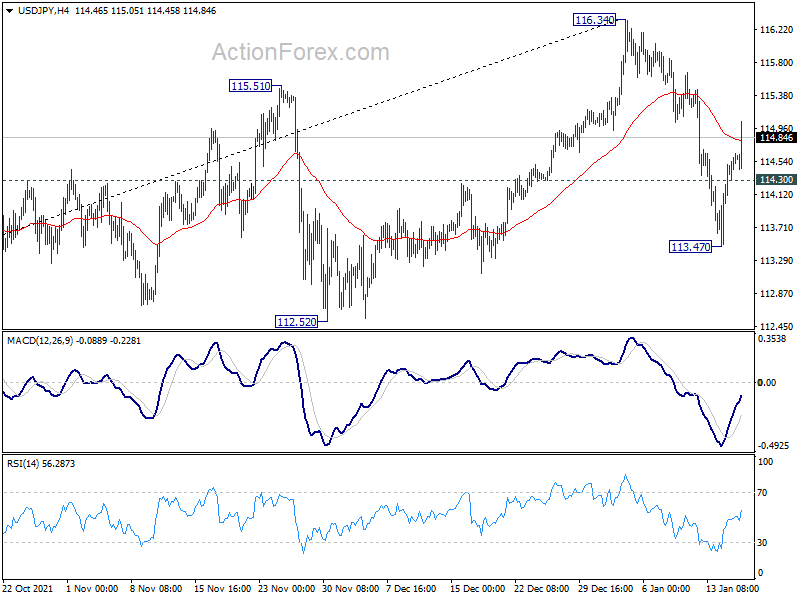

Technically, Yen crosses are displaying a mixed picture. AUD/JPY and NZD/JPY look rather weak after initial post-BoJ spike. EUR/JPY and GBP/JPY also lack momentum to get through 131.39 and 157.74 resistance levels respectively. While USD/JPY’s rebound from 113.47 accelerated, we’re not expecting a break of 116.34 high soon. So, it looks like Yen crosses are to be avoided for now.

{kind=link}

In Asia, at the time of writing, Nikkei is up 0.45%. Hong Kong HSI is down -0.14%. China Shanghai SSE is up 0.94%. Singapore Strait Times is up 0.22%. Japan 10-year JGB yield is up 0.0051 at 0.151. US 10-year yield is up 0.051 at 1.843.

{kind=link}

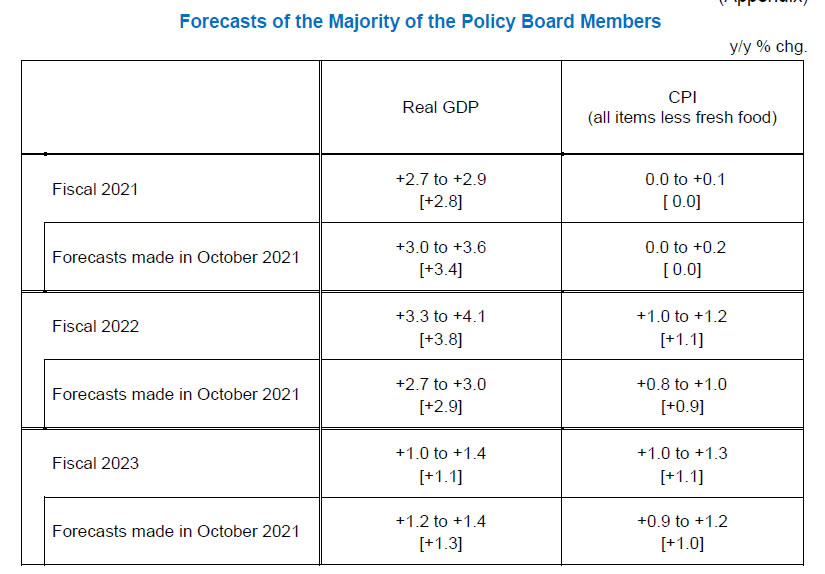

BoJ stands pat, upgrades 2022, 2023 inflation forecasts

BoJ left monetary policy unchanged. Under the yield curve control, short-term policy interest rate is held unchanged at -0.1%. BoJ will also buy a “necessary amount” of JGB bonds to keep 10-year yield at around 0%.

BoJ maintained the pledge to continue with QQE with yield curve control, “aiming to achieve the price stability target of 2 percent, as long as it is necessary for maintaining that target in a stable manner”. It will also continue expanding the monetary base “until the year-on-year rate of increase in the observed consumer price index (CPI, all items less fresh food) exceeds 2 percent and stays above the target in a stable manner.”

In the new economic projections, comparing to October forecasts:

- Fiscal 2021 real GDP growth downgraded from 3.4% to 2.8%.

- Fiscal 2022 real GDP growth upgraded from 2.9% to 3.8%

- Fiscal 2023 real GDP growth downgraded from 1.3% to 1.1%.

- Fiscal 2021 core CPI unchanged at 0.0%.

- Fiscal 2022 core CPI upgraded from 0.9% to 1.1%.

- Fiscal 2023 core CPI upgraded from 1.0% to 1.1%.

{kind=link}

Downbeat New Zealand business confidence, strong inflation pressures

In the The latest NZIER Quarterly Survey of Business Opinion, a net 34.4% of New Zealand businesses expect a deterioration in general economic conditions over the coming months, much worse than prior quarter’s 11.1%. Trading activity for the next three months dropped slightly from 8.7 to 8.3.

Regarding inflation, a net 61% reported increased costs in Q4, highest since 2008. A net 65% expect further increase in prices in the next quarter. NZIER said, “these results point to inflation pressures in the New Zealand economy remaining strong over the coming year.”

Looking ahead

UK employment data will be a focus in European session while Germany ZEW economic sentiment is another. Swiss will release PPI while Italy will release trade balance. Later in the day, Canada housing starts, US Empire state manufacturing and NAHB housing index will be featured.

USD/JPY Daily Outlook

Daily Pivots: (S1) 114.29; (P) 114.47; (R1) 114.79; More…

USD/JPY’s rebound from 113.47 accelerated higher today. While further rise cannot be ruled out, we’re not expecting a break of 116.34 for now. Instead, the corrective pattern from there should extend with another falling leg. On the downside, break of 114.30 minor support will turn bias to the downside for 113.47. Break there will target 112.52 structural support.

{kind=link}

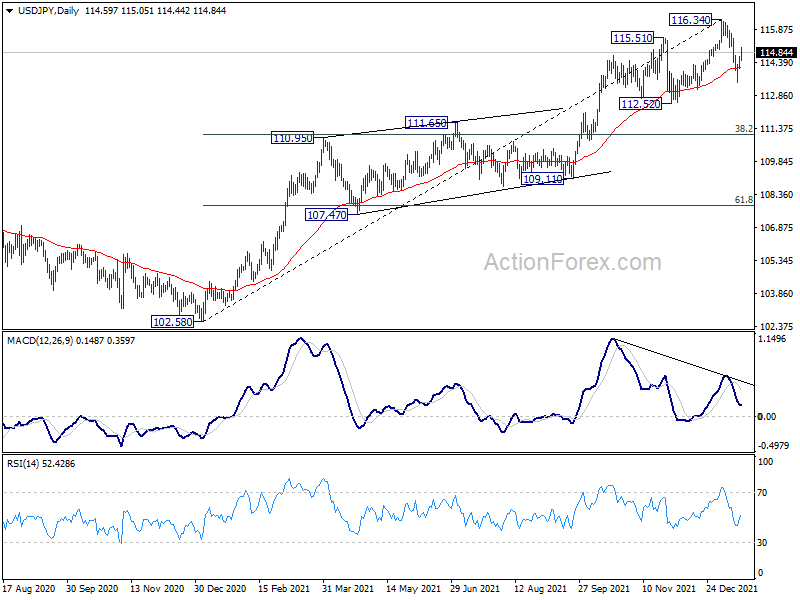

In the bigger picture, no change in the view that rise from 102.58 is the third leg of the up trend from 101.18 (2020 low). Such rally should target a test on 118.65 (2016 high). Sustained break there will pave the way to 120.85 (2015 high) and raise the chance of long term up trend resumption. However, firm break of 112.52 support will dampen this bullish case and we’ll assess the outlook based on subsequent price actions later.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | NZIER Business Confidence Q4 | -28 | -11 | ||

| 03:00 | JPY | BoJ Rate Decision | -0.10% | -0.10% | -0.10% | |

| 04:30 | JPY | Industrial Production M/M Nov F | 7.00% | 7.20% | 7.20% | |

| 07:00 | GBP | ILO Unemployment Rate (3M) Nov | 4.20% | 4.20% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Nov | 4.20% | 4.90% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Nov | 3.80% | 4.30% | ||

| 07:00 | GBP | Claimant Count Change Dec | -38.6K | -49.8K | ||

| 07:30 | CHF | Producer and Import Prices M/M Dec | 0.40% | 0.50% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Dec | 5.80% | |||

| 09:00 | EUR | Italy Trade Balance (EUR) Nov | 4.23B | 3.89B | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Jan | 32.7 | 29.9 | ||

| 10:00 | EUR | Germany ZEW Current Situation Jan | -7.5 | -7.4 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Jan | 29.2 | 26.8 | ||

| 13:15 | CAD | Housing Starts Dec | 234K | 301K | ||

| 13:30 | USD | Empire State Manufacturing Index Jan | 28 | 31.9 | ||

| 15:00 | USD | NAHB Housing Market Index Jan | 84 | 84 |