Euro turns softer in a quiet Asian session together with Swiss Franc, but Yen is even weaker. On the other hand, Aussie is ticking up slightly together with Loonie and Dollar. Overall, trading is rather subdued with major Asian stock indexes treading water in tight range, and Japan is on holiday. Focuses will turn to Fed chair Jerome Powell’s testimony, and US inflation data later in the week, which should bring the markets back to life.

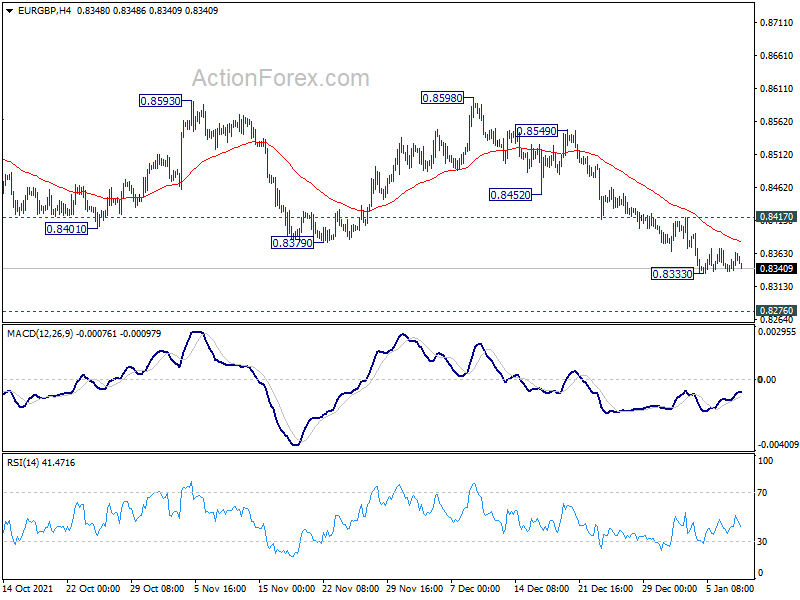

Technically, we’ll keep an eye on Sterling. EUR/GBP is staying bearish, and it looks ready to resume the medium term down trend through 0.8333 temporary low any time. GBP/JPY is also still on track to retest 158.19 resistance, and resume larger up trend. Meanwhile, if GBP/USD could build up more momentum above 1.3570 support turned resistance, that would solidify the case of near term bullish reversal for 1.3833 resistance next.

{kind=link}

In Asia, at the time of writing, Hong Kong HSI is up 0.71%. China Shanghai SSE is up 0.21%. Singapore Strait Times is up 0.78%. Japan is on holiday.

IMF Blog: Faster Fed hike could rattle financial markets

In an blog post, senior IMF officials said the continued to expect “robust US growth”. Inflation will “likely moderate” late this year as supply disruptions ease and fiscal contraction weighs on demand. Fed’s indication that it would raise interest rate more quickly “did not cause a substantial market reassessment of the economic outlook”.

“Should policy rates rise and inflation moderate as expected, history shows that the effects for emerging markets are likely benign if tightening is gradual, well telegraphed, and in response to a strengthening recovery,” the post noted.

However, “broad-based US wage inflation or sustained supply bottlenecks could boost prices more than anticipated and fuel expectations for more rapid inflation”.

“Faster Fed rate increases in response could rattle financial markets and tighten financial conditions globally. These developments could come with a slowing of US demand and trade and may lead to capital outflows and currency depreciation in emerging markets.”

ECB Schnabel: Rising energy prices may require a departure from a looking through policy

ECB Executive Board member Isabel Schnabel warned in a speech on Saturday, “monetary policy, for its part, cannot afford to look through energy price increases if they pose a risk to medium-term price stability.”

“This could be the case if prospects of persistently rising energy prices contribute to a deanchoring of inflation expectations, or if underlying price pressures threaten to lift inflation above our 2% target as rising carbon prices and the associated shifts in economic activity boost rather than suppress growth, employment and aggregate demand over the medium term.”

WTI oil back below 80 as Kazakhstan normalizes production

Oil prices dip mildly in Asian session as Kazakhstan’s largest oil venture Tengizchevroil is gradually normalizing production. Some contractors had disrupted train lines in support of protests in the country last week.

WTI crude oil hit as high as 80.63 last week but fails to sustain above 80 handle so far. Some consolidations could be seen first, but further rally is expected as long as 74.48 support holds. Rally from 62.90 should target 161.8% projection of 62.90 to 73.66 from 66.46 at 83.86, which is close to 85.92 high.

For now, we’re not expecting a break of 85.92 yet. We’d expect at least one more down leg before the corrective pattern from there completes. Hence, we’d look for topping between 83.86/85.92.

{kind=link}

Fed Powell testimony and US inflation to move the markets

Fed Chair Jerome Powell’s testimony before Senate Banking committee will be a main focus of the week. Powell would likely be asked about his views on March rate hike, as well as the timing of off-loading the balance sheet. Additionally, CPI and PPI from the US would be equally market moving while retail sales will be featured. Elsewhere, a batch of data from China, UK and Australia will also catch some attention.

Here are some highlights for the week:

- Monday: Australia MI inflation gauge, building approvals; Eurozone Sentix investor confidence, unemployment rate.

- Tuesday: Australia retail sales, trade balance; Japan leading indicators; Fed chair Powell’s testimony.

- Wednesday: Japan banking lending, current account, Eco watchers sentiment; China CPI, PPI; Eurozone industrial production; US CPI, Fed’s Beige Book.

- Thursday: New Zealand building permits; Japan M2; ECB monthly bulletin; US PPI, jobless claims.

- Friday: China trade balance; Japan PPI; UK GDP, production, trade balance; Eurozone balance; US retail sales, import prices, industrial production, U of Michigan sentiment.

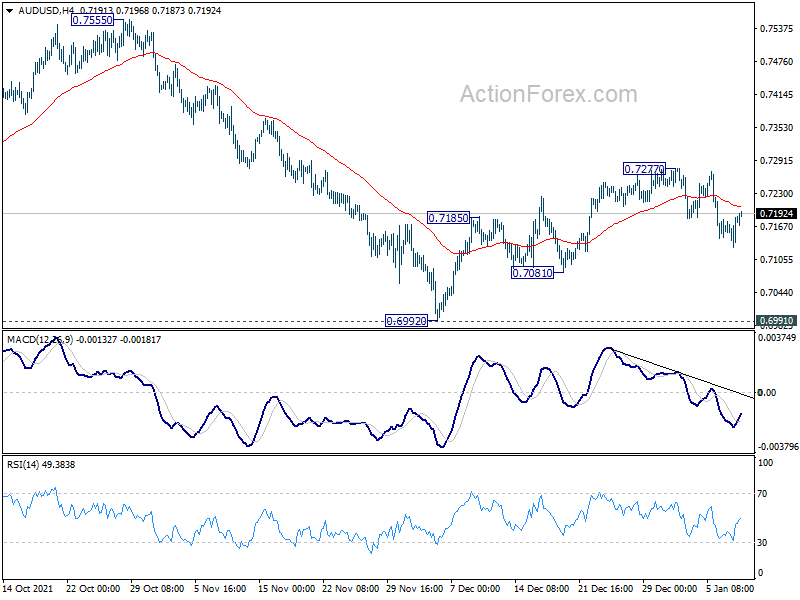

AUD/USD Daily Report

Daily Pivots: (S1) 0.7145; (P) 0.7167; (R1) 0.7203; More…

AUD/USD recovers mildly today but stays in range of 0.7081/7277. Intraday bias remains neutral for the moment. On the downside, break of 0.7081 support will indicate that corrective rebound from 0.6992 has completed with three waves up to 0.7277, after hitting 55 day EMA. Intraday bias will be back on the downside for retesting 0.6991/2 key support zone. Firm break there will resume larger down trend from 0.8006. On the upside, though, break of 0.7277 will turn bias to the upside to resume the rebound.

{kind=link}

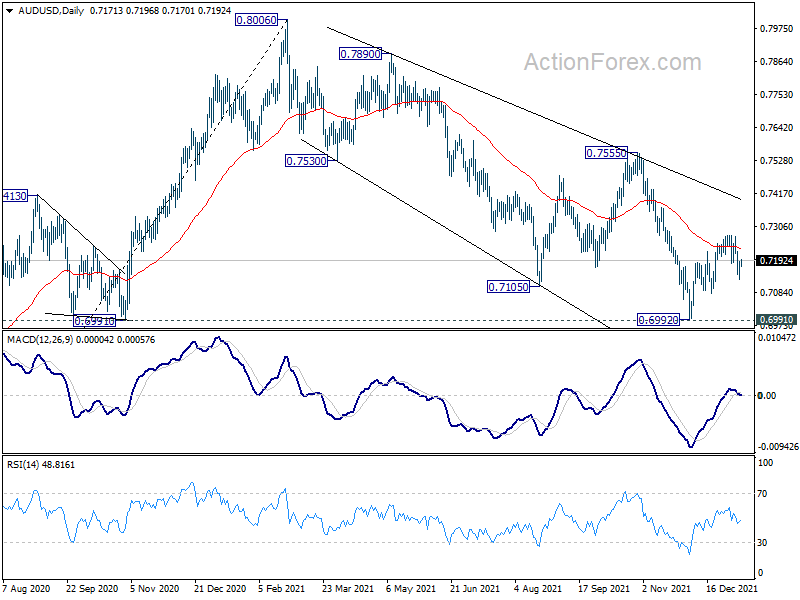

In the bigger picture, strong rebound from 0.6991 key structural support will retain medium term bullishness. That is, whole up trend from 0.5506 is still in progress. Firm break of 0.7555 resistance will target 0.8006 high and above. However, sustained break of 0.6991 will argue that the whole up trend from 0.5506 might be finished at 0.8006, after rejection by 0.8135 long term resistance. Deeper decline would then be seen back to 61.8% retracement of 0.5506 to 0.8006 at 0.6461.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | TD Securities Inflation M/M Dec | 0.20% | 0.30% | ||

| 00:30 | AUD | Building Permits M/M Nov | 3.60% | 3.20% | -12.90% | |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Jan | 12 | 13.5 | ||

| 10:00 | EUR | Eurozone Unemployment Rate Nov | 7.20% | 7.30% | ||

| 15:00 | USD | Wholesale Inventories Nov F | 1.20% | 1.20% |