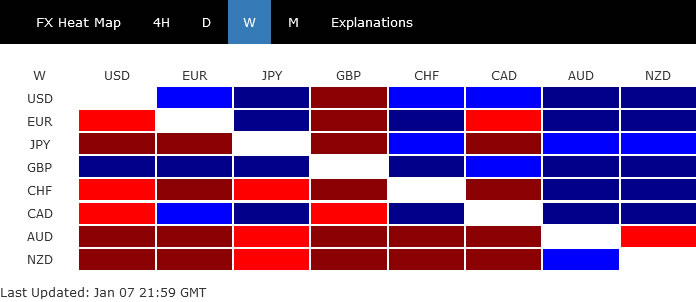

It was a roller coaster ride as traders came back for the new year. Markets were in full risk-on mode as worries over Omicron faded. Yet, sentiment turned after more hawkish than expected FOMC minutes. Major stock indexes were than in deep pull back. Major global benchmark treasury yields powered through key resistance level.

In the currency markets, Sterling was the surprised winner. Dollar, ended as the second strongest, has indeed failed to ride on hawkish Fed and surging yields. The greenback was more mixed than the currency heat map suggested. Yen regained some ground ground after initial selloff. Aussie and Kiwi were the worst performer, and would be guided by overall risk sentiment ahead.

{kind=link}

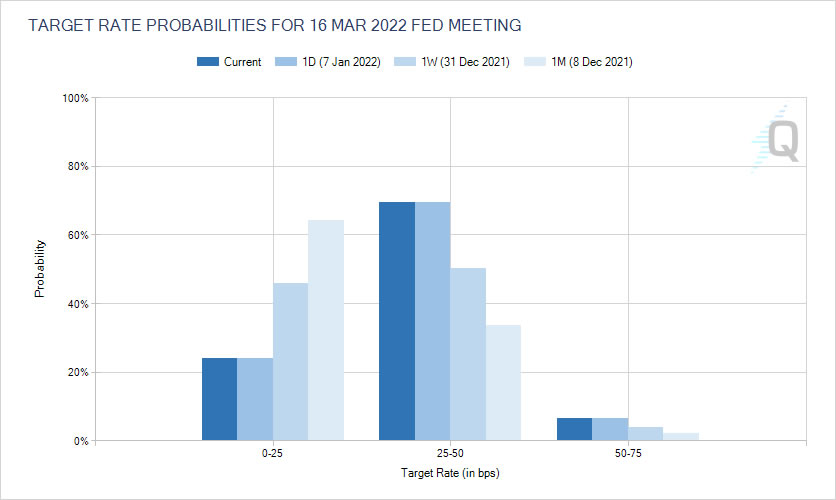

Markets adding more bets to March Fed hike

The surprisingly hawkish minutes of December FOMC meeting were the main driver of market volatility last week. Fed is not only seen as ready to raise interest rate as early as in March. It’s even starting to thinking about shrinking the balance sheet soon after rate lift off.

The December non-farm payroll report might disappointed the markets with the much weaker than expected job growth. Yet, unemployment is back below 4% at 3.9%. Wage growth accelerated with average hourly earnings gaining an impressive 0.6% mom. The set of data indicated tightness in the labor market which would continue to put upward pressure on wages and thus inflation. Fed should have came out in a stronger position for stimulus remove.

Indeed Fed funds futures are now pricing in nearly 76% of a rate hike in March, comparing to 65% a week ago, and 36% a month ago.

{kind=link}

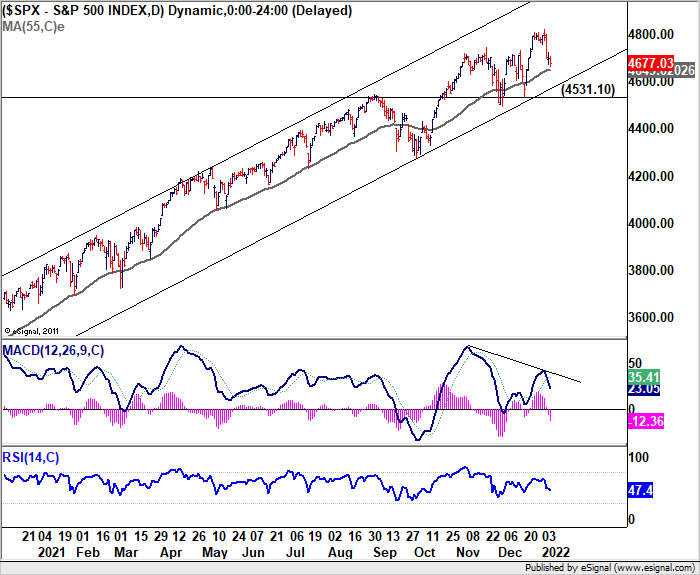

S&P 500 staying in up trend despite deep pull back

Stocks had a rather deep pull back on hawkish Fed, but there was no disaster. S&P 500 is losing upside momentum as seen in daily MACD. But there is no clear sign of major topping yet, with the index staying above 55 day EMA and well inside the medium term rising channel. Current up trend is still on track to 5000 handle, and even further to 138.2% projection of 2191.86 to 3588.11 from 3233.94 at 5163.55.

Nevertheless sustained trading below 55 day EMA (now at 4649.02) will be the first warning of reversal. Further break of 4531.10 support will indicate the start of a medium term correction.

{kind=link}

{kind=link}

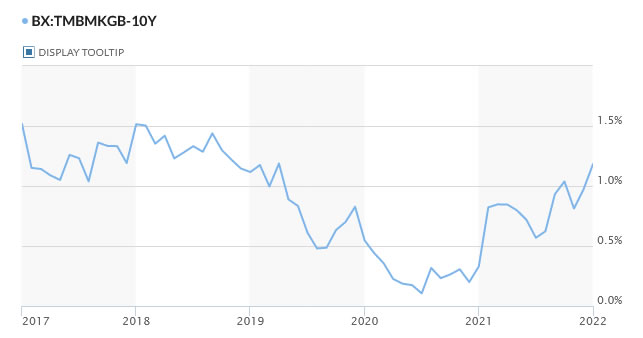

10-year yield resumes medium term up trend towards 2% and above

10-year yield surged through 1.765 key resistance to close at 1.771. The development should confirm resumption of whole up trend from 0.398. The strong support from 55 week EMA also affirm medium term bullishness. TNX should target 2% handle, and possibly above.

The next critical zone will be at 61.8% retracement of 3.248 to 0.398 at 2.159, which is close to 61.8% projection from 0.398 to 1.765 from 1.343 at 2.187. Some defining development would need to happen before we see TNX pushing with this resistance zone with conviction.

{kind=link}

{kind=link}

The rally in US treasury yield lost much of the impact on Dollar, as other global benchmark yields were catching up quickly. Germany 10-year bund yield rose to close at -0.04, hitting the highest level since 2019, and looks set to turn positive soon. UK 10-year gilt yield also rose to close at 1.182, highest since 2019. Even Japan 10-year JGB yield surged to 0.135, back above 0.1% handle in nearly a year.

{kind=link}

{kind=link}

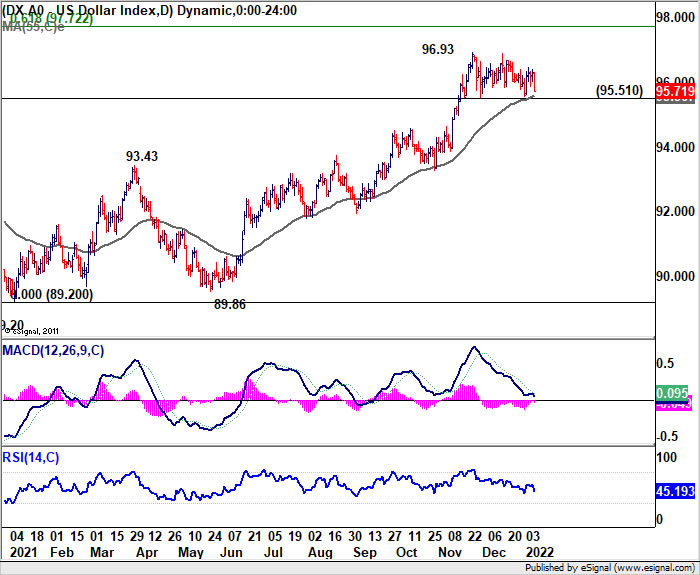

Dollar staying bullish in consolidation… for now

Dollar index stayed in range below 96.93 last week and outlook is unchanged. Further rise is expected as long as 95.51 support holds. The rally from 89.20 should extend to 61.8% retracement of 102.99 to 89.20 next. However, firm break of 96.93 would bring deeper pull back towards 55 week EMA (now at 93.72) instead.

{kind=link}

{kind=link}

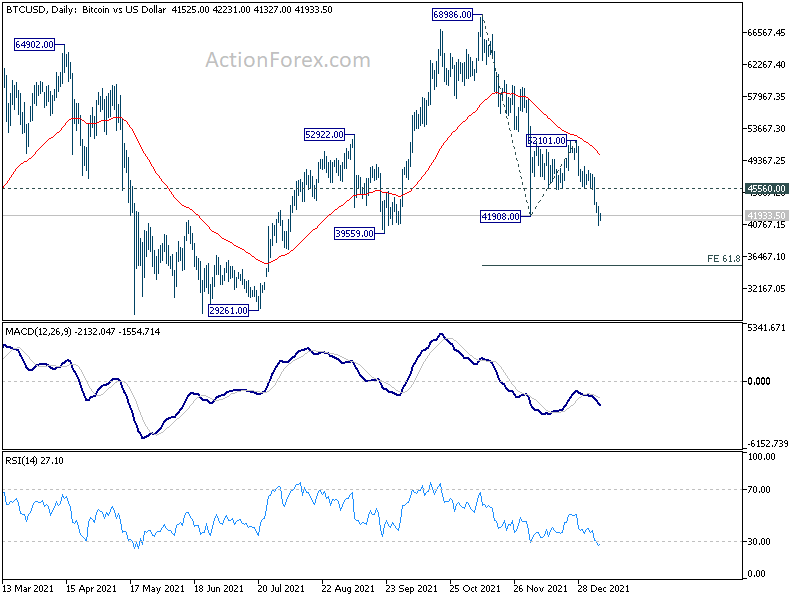

Bitcoin to extend down trend towards 35k

Some other markets seemed to have much more committed response to Fed. For example, Bitcoin dived through 41908 low to resume the decline from 68986. Such fall is seen as at the same degree as the rise from 29161 to 68986. While there might be some support around 39559, which is close to 40k handle, to bring recovery. Upside should be limited by 45560 support turned resistance. Bitcoin should have a take on 61.8% projection of 68986 to 41908 from 52101 at 35366 before forming a bottom.

{kind=link}

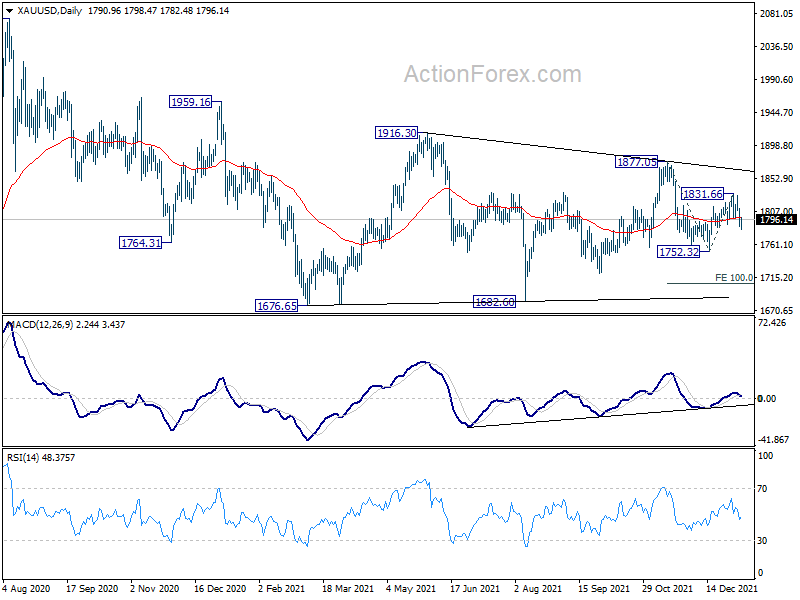

Gold might have completed recovery, heading back to 1700

Gold’s decline argues that recovery from 172.32 has completed at 1831.66. Fall from 1877.05, as the fourth leg of the pattern from 1676.65, is probably ready to resume. Sustained trading below 55 day EMA (now at 1798.60) will target 1752.32 support. Break will confirm this bearish case and target 100% projection of 1877.05 to 1752.32 from 1831.66 at 1706.93.

{kind=link}

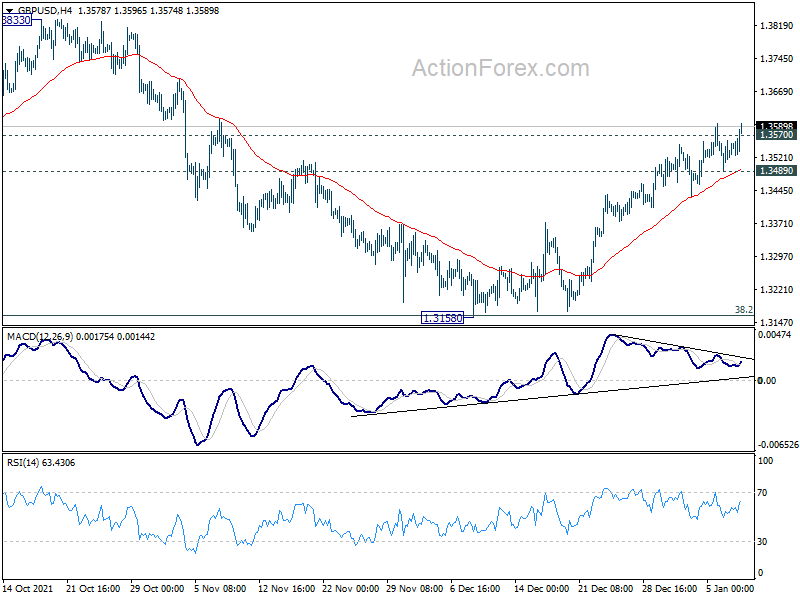

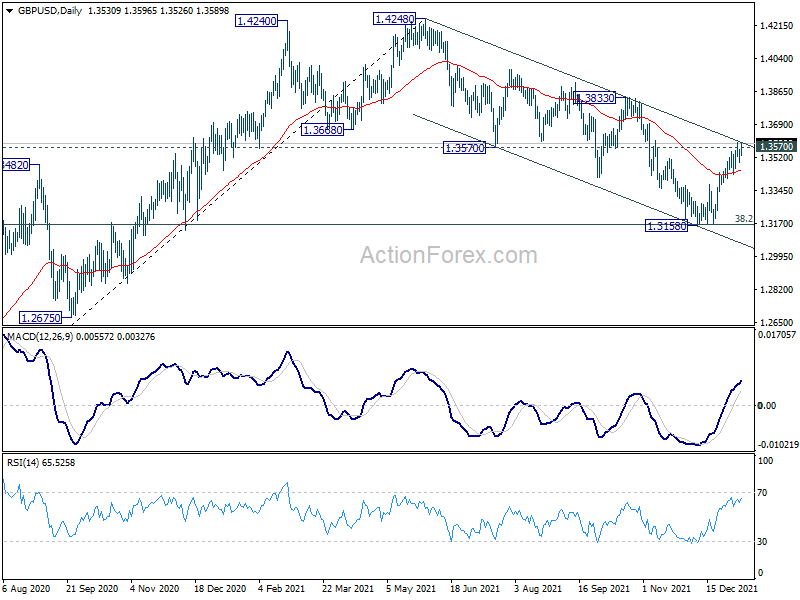

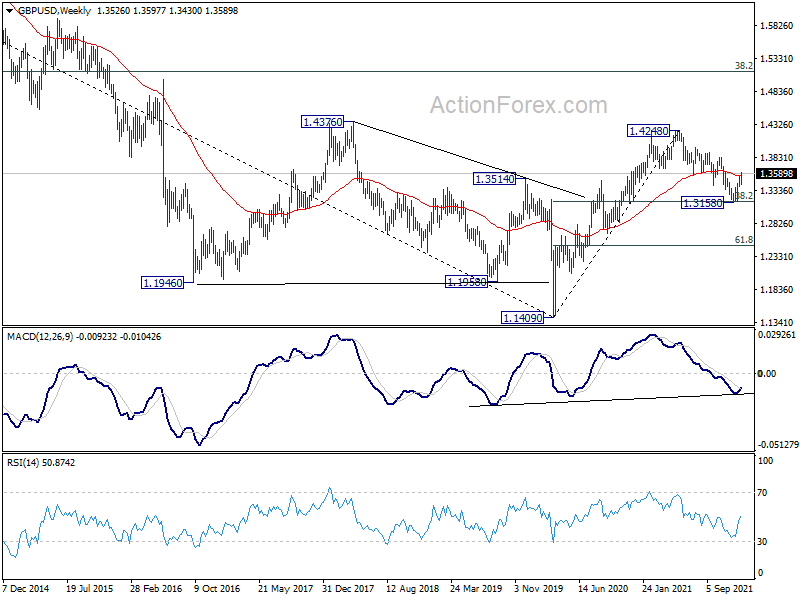

GBP/USD Weekly Outlook

GBP/USD’s rebound from 1.3158 extended higher last week and breached 1.3570 support turned resistance. The development affirms the view that corrective fall from 1.4248 as complete with three waves down to 1.3158, after hitting 1.3164 medium term fibonacci level. Sustained trading above 1.3570 will pave the way to 1.3833 resistance next. On the downside, though, break of 1.3489 minor support will mix up the outlook and turn intraday bias neutral first.

{kind=link}

In the bigger picture, strong support was seen from 38.2% retracement of 1.1409 to 1.4248 at 1.3164. The development suggests that up trend from 1.1409 (2020 low) is still in progress. On resumption, next target will be 38.2% retracement of 2.1161 to 1.1409 at 1.5134. Nevertheless sustained break of 1.3164 will argue that whole rise from 1.1409 has completed and bring deeper fall to 61.8% retracement at 1.2493.

{kind=link}

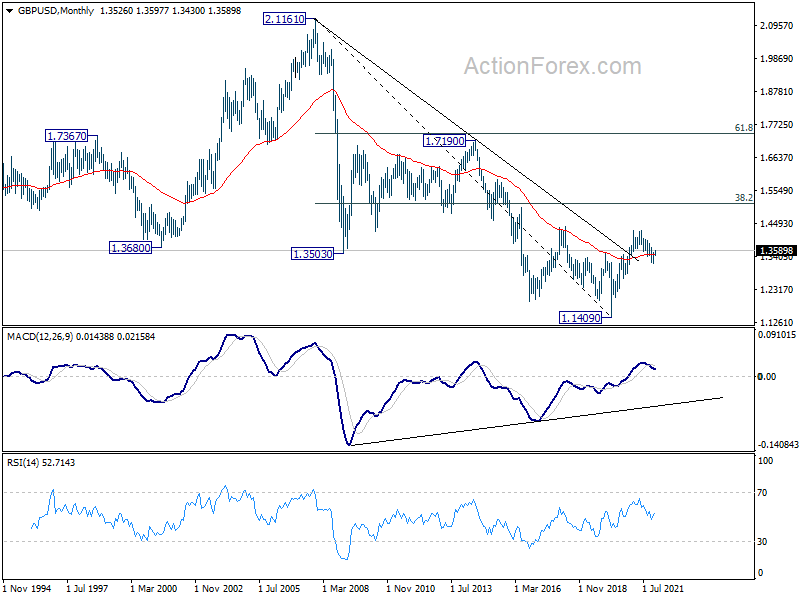

In the longer term picture, a long term bottom should be in place at 1.1409, on bullish convergence condition in monthly MACD. Rise from there would target 38.2% retracement of 2.1161 to 1.1409 at 1.5134. Reaction from there would reveal whether rise from 1.1409 is just a correction, or developing into a long term up trend.

{kind=link}

{kind=link}