Sterling and Euro are trading broadly higher today, together with Aussie. On the other hand, Yen and Dollar are both under some selling pressure. Rebound in Europe yield is a factor in driving the markets. We’ll see if there is further rally in stocks before holidays that could push Dollar and Yen further lower.

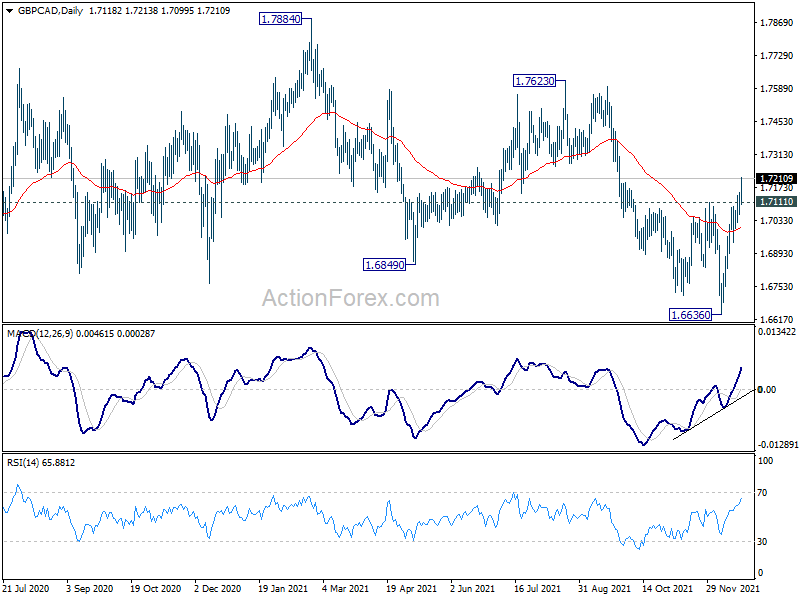

Technically, GBP/CAD’s rally today should confirm that 1.7111 resistance is firmly taken out. Whole fall from 1.7884 has completed with three waves down to 1.6636. Further rally should be seen to 1.7623 resistance first, and possibly further to retest 1.7884. We’ll see if GBP/USD would follow and break through 1.3373 resistance.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.02%. DAX is down -0.05%. CAC is up 0.04%. Germany 10-year yield is up 0.0144 at -0.291. Earlier in Asia, Nikkei rose 0.16%. Hong Kong HSI rose 0.57%. China Shanghai SSE dropped -0.07%. Singapore Strait Times rose 0.08%. Japan 10-year JGB yield rose 0.0079 to 0.063.

US Q3 GDP growth finalized at 2.3% annualized

US Q3 GDP growth rate was finalized at 2.3% annualized, revised up from 2.1%. The update primarily reflects upward revisions to personal consumption expenditures (PCE) and private inventory investment that were partly offset by a downward revision to exports. Imports, which are a subtraction in the calculation of GDP, were revised down.

UK GDP growth finalized at 1.1% qoq in Q3

UK Q3 GDP growth was finalized at 1.1% qoq, revised down from first estimate of 1.3% increased. The level of GDP remained -1.5% below pre-coronavirus level in Q4 2019. Annual GDP in 2020 is now estimated to have fallen by -9.4%. Net borrowing position with the rest of the world lowered to -4.3% of GDP from Q2’s -2.4%.

ECB Schnabel: A week Q4 to spillover to beginning of next year

ECB Executive Board member Isabel Schnabel said in an interview, “in general, I think the recovery continues”. But due to new wave of infections, “we are seeing headwinds in the short term”. ECB is looking at a “weaker fourth quarter” which is “likely to spill over to the beginning of next year”. But she expected “a strong rebound thereafter”. So, “we see the recovery as being delayed rather than derailed.”

She added that the factors that pushed up inflation are “likely to either reverse or at least become less pronounced over the coming year”, including supply bottlenecks, energy prices and base effects. Inflation is going to “decline over the course of next year”, but ECB is “less certain about how fast and how strong the decline will be”.

Schnabel also said ECB is taking a “step-by-step approach to normalization” of monetary policy”. The pace can be adjusted to the incoming data. And, “we need to retain optionality to make sure that we sustainably reach our 2% target.”

BoJ minutes: members discussed impact of Yen’s depreciation

In the minutes of October 27-28 meeting, BoJ said “yen had depreciated somewhat significantly against both the U.S. dollar and the euro, mainly due to rises in U.S. and European interest rates”. Members have discussed the impact of the yen’s depreciation.

Some members said, “the depreciation had positively affected Japan’s economy as a whole through an increase in profits from business conducted overseas and a rise in stock prices, although its effect of pushing up exports had declined.”

One member said, “the effect of the depreciation on each economic entity was uneven, depending on industry and size”. Another member noted, “while prices had increased recently, triggered mainly by the yen’s depreciation, it was unlikely at present that heightened inflationary pressure would reduce the economic welfare of Japan as a whole.”

Australia Westpac leading index rose to -0.2%, Omicron not derailing recovery

The six month annualized growth rate in Westpac-Melbourne Institute Leading Index rose from -0.5% to -0.2% in November. The index has been in negative territory for three consecutive months, partly reflecting the lockdowns in New South Wales and Victoria. Nevertheless, reopening rebounds should eventually lift growth back above trend.

Westpac said both itself and the RBA “currently believe that Omicron will not derail the recovery although the next month will determine the extent of the delay and uncertainty.”

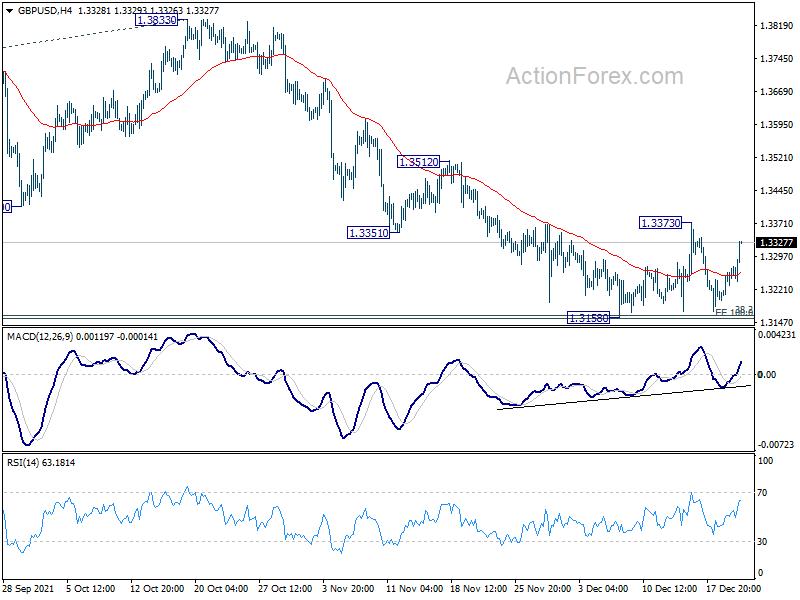

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3221; (P) 1.3246; (R1) 1.3294; More…

GBP/USD rebounds strongly today but stays below 1.3373 resistance. Intraday bias remains neutral at this point. On the upside, break of 1.3373 will resume the rebound from 1.3158 to to 55 day EMA (now at 1.3423). Sustained break there will be an early sign of bullish reversal and target 1.3570 support turned resistance next. On the downside, however, firm break of 1.3164 medium term fibonacci level will carry larger bearish implication. Fall from 1.4248 should resume and target 161.8% projection of 1.4248 to 1.3570 from 1.3833 at 1.2736.

{kind=link}

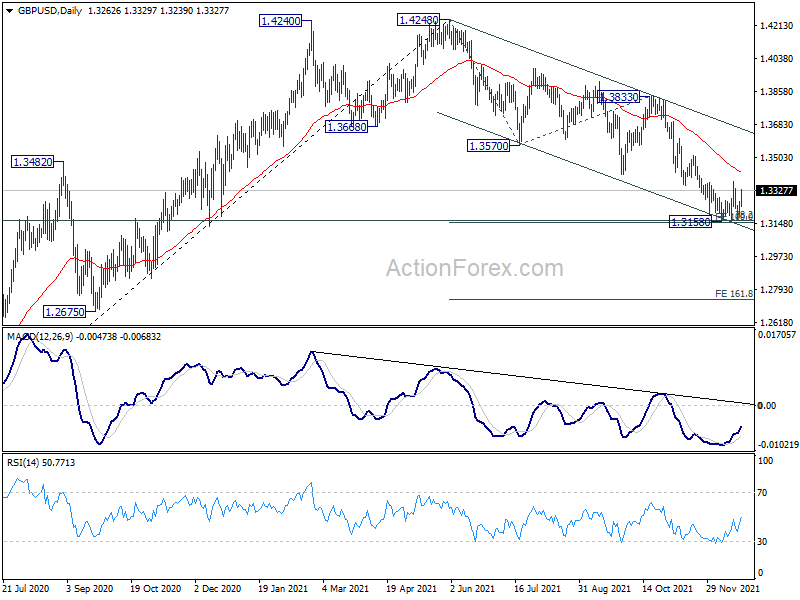

In the bigger picture, focus remains on 38.2% retracement of 1.1409 to 1.4248 at 1.3164. Sustained break there will argue that whole rise from 1.1409 has completed at 1.4248, after rejection by 1.4376 long term resistance. That will revive some medium term bearishness and and target 61.8% retracement at 1.2493. However, strong rebound from current level will revive argue that up trend from 1.1409 is still in progress, and probably ready to resume.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/MNov | 0.10% | 0.20% | 0.30% | |

| 23:50 | JPY | BoJ Minutes | ||||

| 07:00 | GBP | GDP Q/Q Q3 F | 1.10% | 1.30% | 1.30% | |

| 07:00 | GBP | Current Account (GBP) Q3 | -24.4B | -15.6B | -8.6B | |

| 13:30 | USD | GDP Annualized Q3 F | 2.30% | 2.10% | 2.10% | |

| 13:30 | USD | GDP Price Index Q3 F | 6.00% | 5.90% | 5.90% | |

| 14:00 | CHF | SNB Quarterly Bulletin Q4 | ||||

| 15:00 | USD | Existing Home Sales M/M Nov | 6.5M | 6.34M | ||

| 15:00 | USD | Consumer Confidence Dec | 111.1 | 109.5 | ||

| 15:30 | USD | Crude Oil Inventories | -2.4M | -4.6M |