Sterling rises broadly today with help from solid job data, which eased the concerns over the impact of end of furlough scheme. Dollar is also firm as supported by better than expected retail sales sales. Euro is trying to digest some losses but stays weak on dovish ECB expectations. On the other hand, commodity currencies are turning softer on mixed risk sentiments.

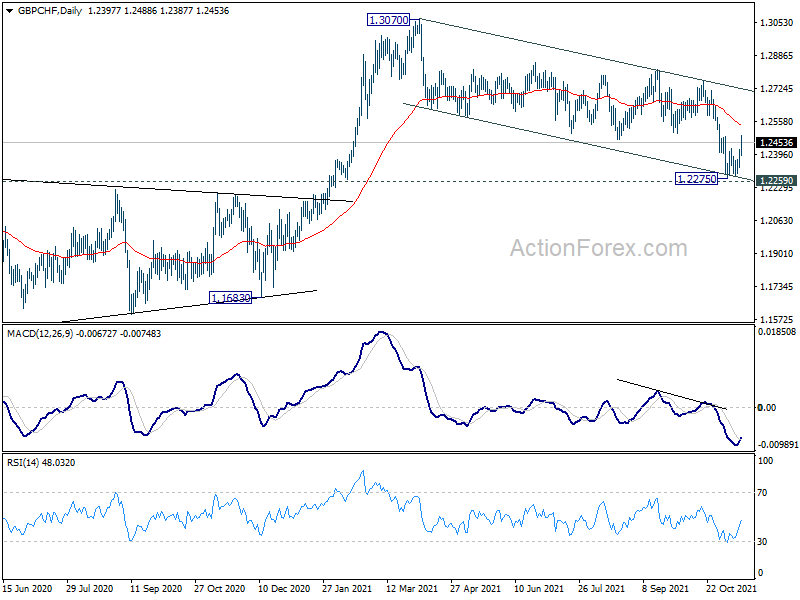

Technically, GBP/CHF’s strong rebound today argues that 1.2259 key resistance turned support was well defended, for now. Focus is now on 55 day EMA (now at 1.2542). Sustained break there will raise the chance that medium term correction from 1.3070 has completed and affirms underlying resilience of the Pound.

{kind=link}

In Europe, at the time of writing, FTSE is down -0.07%. DAX is up 0.40%. CAC is up 0.34%. Germany 10-year yield is down -0.007 at -0.233. Earlier in Asia, Nikkei rose 0.11%. Hong Kong HSI rose 1.27%. China Shanghai SSE dropped -0.33%. Singapore Strait Times dropped -0.05%. Japan 10-year JGB yield rose 0.0076 to 0.076.

US retail sales rose 1.7% mom in Oct, ex-auto sales up 1.7% mom

US retail sales rose 1.7% mom in to USD 638.2B in October, above expectation of 1.2% mom. Total sales for the August through October period were up 15.4% from the same period a year ago.

Ex-auto sales rose 1.7% mom, above expectation of 1.2% mom. Ex-gasoline sales rose 1.5% mom. Ex-auto, ex-gasoline sales rose 1.4% mom.

Import price index rose 1.2% mom, versus expectation of 1.0% mom.

Eurozone GDP grew 2.2% qoq in Q3, EU rose 2.1% qoq

According to flash estimate, Eurozone GDP grew 2.2% qoq in Q3, 3.7% yoy. Employment grew 0.9% qoq, 2.0% yoy.

EU GDP grew 2.1% qoq, 3.9% yoy. Employment grew 0.9% qoq, 2.1% yoy.

UK unemployment rate dropped to 4.3%, employment rate rose to 75.4%

UK unemployment rate dropped to 4.3% in the three months to September, down from 4.5%, better than expectation of 4.5%. Employment rate rose 0.4% to 75.4%, “driven by a record high net flow from unemployment to employment”. Payrolled employment rose 160k.

Wage growth disappointed, however, with average earnings excluding bonus up 4.9% 3moy versus expectation of 6.0%. Average earnings including bonus rose 5.8% 3moy, versus expectation of 7.0%. in October, claimant count dropped -14.9k.

RBA Lowe: Still plausible that rate won’t be raised before 2024

In a speech, RBA Governor Philip Lowe reiterated, “the latest data and forecasts do not warrant an increase in the cash rate in 2022.” Also, it’s “still plausible that the first increase in the cash rate will not be before 2024” even if underlying inflation hits 2.5%.

He said, the central scenario is that underlying inflation will reach “middle of the target by the end of 2023”. That would be the first time in nearly seven years that inflation is at the mid-point. And, “this, by itself, does not warrant an increase in the cash rate.”

For rate hike, RBA would like to see inflation “well within the 2–3 per cent range”, and, ” have a reasonable degree of confidence that it will not fall back again”. The “trajectory” is important, “with a slow drift up in underlying inflation having different policy implications to a sharp rise.”

Another important consideration will be developments in the labor market. wages growth is used as one of the “guideposts” and “it is likely that wages will need to be growing at 3 point something per cent to sustain inflation around the middle of the target band.”

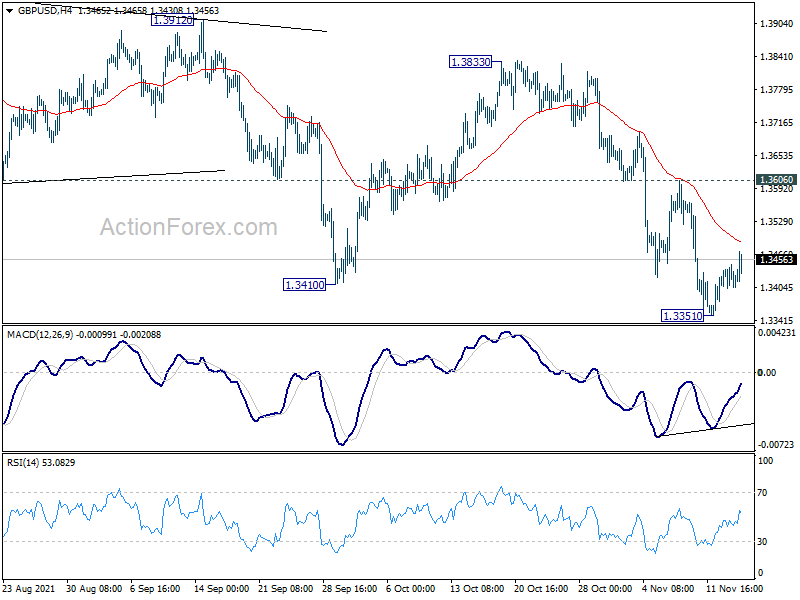

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3394; (P) 1.3422; (R1) 1.3440; More…

GBP/USD’s recovery from 1.3351 extends higher today but outlook is unchanged. Intraday bias remains neutral first. Upside of recovery should be limited below 1.3606 resistance to bring down trend resumption. On the downside, break of 1.3351 will extend the decline from 1.4248 to 1.3164 fibonacci level next.

{kind=link}

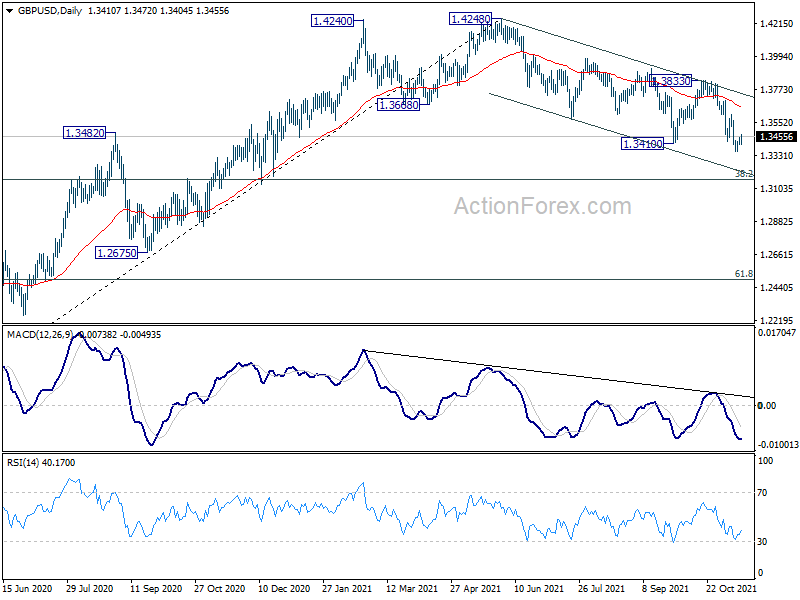

In the bigger picture, the structure of the fall from 1.4248 suggests that it’s a correction to the up trend from 1.1409 (2020 low) only. While deeper fall cannot be ruled out yet, downside should be contained by 38.2% retracement of 1.1409 to 1.4248 at 1.3164, at least on first attempt, to bring rebound. On the upside, firm break of 1.4376 key resistance (2018 high) will add to the case of long term bullish reversal. However, sustained trading below 1.3164 will revive some medium term bearishness and target 61.8% retracement at 1.2493.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | RBA Minutes | ||||

| 02:30 | AUD | RBA’s Governor Lowe speech | ||||

| 04:30 | JPY | Tertiary Industry Index M/M Sep | 0.50% | 0.90% | -1.70% | -1.10% |

| 07:00 | GBP | Claimant Count Change Oct | -14.9K | -51.1K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Sep | 4.3 | 4.50% | 4.50% | |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Sep | 4.90% | 6.00% | 6.00% | |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Sep | 5.80% | 7.00% | 7.20% | |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 2.20% | 2.20% | 2.20% | |

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 P | 0.90% | 0.60% | 0.70% | |

| 13:15 | CAD | Housing Starts Y/Y Oct | 237K | 265K | 251K | 250K |

| 13:30 | USD | Retail Sales M/M Oct | 1.70% | 1.20% | 0.70% | |

| 13:30 | USD | Retail Sales ex Autos M/M Oct | 1.70% | 1.00% | 0.80% | |

| 13:30 | USD | Import Price Index M/M Oct | 1.20% | 1.00% | 0.40% | |

| 14:15 | USD | Industrial Production M/M Oct | 0.90% | -1.30% | ||

| 14:15 | USD | Capacity Utilization Oct | 75.90% | 75.20% | ||

| 15:00 | USD | Business Inventories Sep | 0.50% | 0.60% | ||

| 15:00 | USD | NAHB Housing Market Index Nov | 80 | 80 |