Euro tumbled broadly overnight, riding on dovish comments from ECB President Christine Lagarde. In short, Lagarde continued to talk down the need of early stimulus withdrawal and warned of the hurt to recovery for doing so. Swiss Franc is currently the second weakest, followed by Yen. On the other hand, commodity currencies are the stronger one as led by Aussie, even though stock rally attempt faltered overnight.

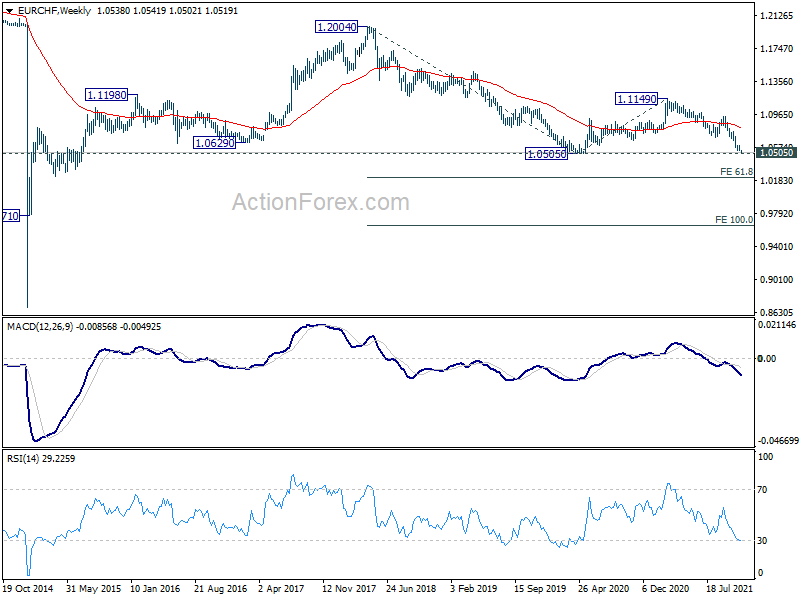

Technically, EUR/USD is now approaching a key target and support level at around 1.13 handle. EUR/CHF is also pressing 1.0505 key support level of 2020 low. We’d pay attention to bottoming signals around these two levels, at least on first attempt. However, sustained break of the levels in both pairs will carry large bearish implication and could prompt even steeper, broad based, selloff for the medium term.

{kind=link}

In Asia, at the time of writing, Nikkei is trading up 0.06%. Hong Kong HSI is up 0.94%. China Shanghai SSE is down -0.18%. Singapore Strait Times is down -0.01%. Japan 10-year JGB yield is up 0.0114 at 0.079. Overnight, DOW dropped -0.04%. S&P 500 dropped -0.00%. NASDAQ dropped -0.04%. 10-year yield rose 0.041 to 1.623.

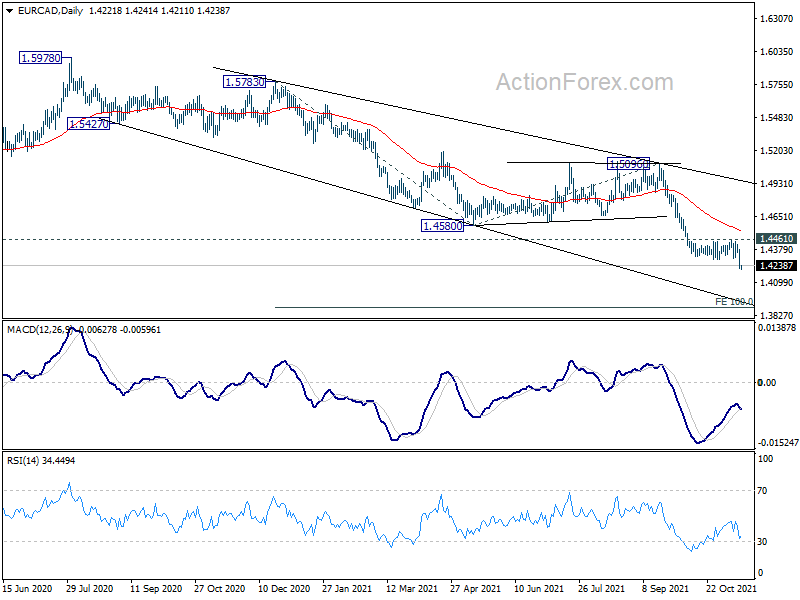

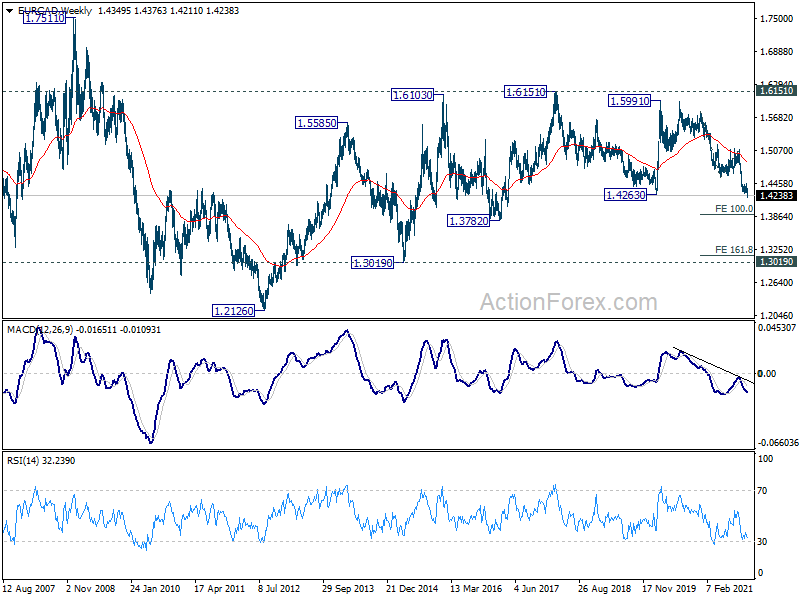

EUR/CAD downside breakout on broad Euro weakness

EUR/CAD’s down trend finally resumed this week, following broad based selloff in Euro, and hit as low as 1.4211 so far. Current fall is part of the down trend from 1.5991. Next target is 100% projection of 1.5783 to 1.4580 from 1.5096 at 1.3893. For now, outlook will stay bearish as long as 1.4661 resistance holds, even in case of recovery.

Also, it should be noted that 1.4263 key support (2020 low) is now taken out by the cross. Fall from 1.5991 would extend through 1.3782 support before bottoming. Yet, we’re not seeing a strong bearish scenarios for pushing through 1.3019 yet. We’ll see how the downside momentum develops in the medium term.

{kind=link}

{kind=link}

Fed Barkin: It’s helpful to have a few months to evaluate

Richmond Fed President Tom Barkin said yesterday that it’s helpful to have “a few more months” to evaluate to see “where reality is in this economy, and if the need to act is there”. He added that “we’re not going to hesitate” to accelerate tapering to get ahead of inflation is needed”.

But, “I personally think it’s very helpful for us to have a few more months to evaluate, is inflation going to come back to more normal levels? Is the labor market going to open up as people spend through some of this savings?”

RBA Lowe: Still plausible that rate won’t be raised before 2024

In a speech, RBA Governor Philip Lowe reiterated, “the latest data and forecasts do not warrant an increase in the cash rate in 2022.” Also, it’s “still plausible that the first increase in the cash rate will not be before 2024” even if underlying inflation hits 2.5%.

He said, the central scenario is that underlying inflation will reach “middle of the target by the end of 2023”. That would be the first time in nearly seven years that inflation is at the mid-point. And, “this, by itself, does not warrant an increase in the cash rate.”

For rate hike, RBA would like to see inflation “well within the 2–3 per cent range”, and, ” have a reasonable degree of confidence that it will not fall back again”. The “trajectory” is important, “with a slow drift up in underlying inflation having different policy implications to a sharp rise.”

Another important consideration will be developments in the labor market. wages growth is used as one of the “guideposts” and “it is likely that wages will need to be growing at 3 point something per cent to sustain inflation around the middle of the target band.”

Looking ahead

UK employment data will be a major focus in European session. Eurozone will also release GDP and employment change. Later in the day, US retail sales will take center stage, with import price, industrial production, business inventories and NAHB housing index featured too. Canada will release housing starts.

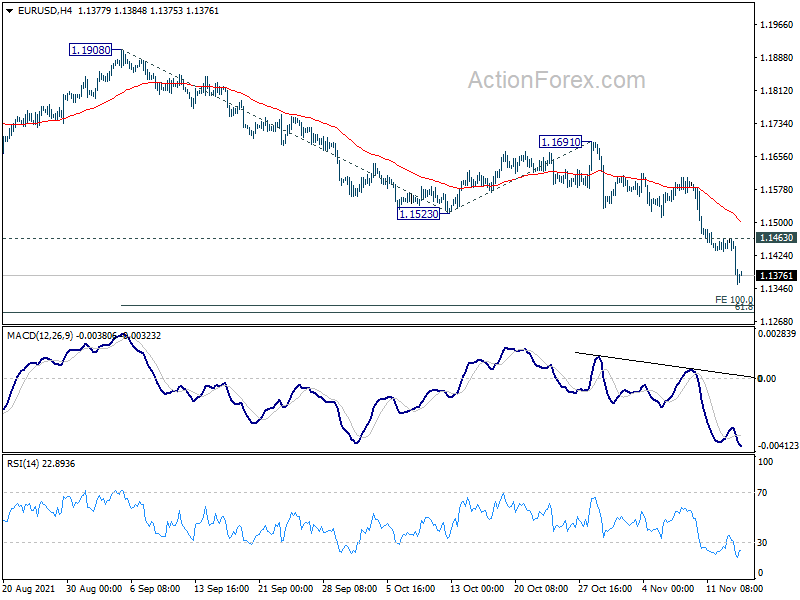

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1329; (P) 1.1396; (R1) 1.1437; More…

EUR/USD’s decline reaccelerates to as low as 1.1355 so far today. Intraday bias remains on the downside for 100% projection 1.1908 to 1.1523 from 1.1691 at 1.1453 at 1.1306, which is close to long term fibonacci level at 1.1289. We’d pay attention to bottoming signal there. Break of 1.1463 minor resistance should now suggest short term bottoming and bring rebound back to 1.1523/1691 resistance zone first. However, decisive break there will pave the way to 161.8% projection at 1.1068 next.

{kind=link}

In the bigger picture, there are various ways of interpreting the fall from 1.2348 (2021 high). It could be a correction to rise from 1.0635 (2020 low), the fourth leg of a sideway pattern from 1.0339 (2017 low), or resuming long term down trend. In any case, outlook will now stay bearish as long as 1.1703 support turned resistance holds. Sustained break of 61.8% retracement of 1.0635 to 1.2348 at 1.1289 could pave the way back to 1.0635.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | RBA Minutes | ||||

| 02:30 | AUD | RBA’s Governor Lowe speech | ||||

| 04:30 | JPY | Tertiary Industry Index M/M Sep | 0.5% | 0.90% | -1.70% | -1.1% |

| 07:00 | GBP | Claimant Count Change Oct | -51.1K | |||

| 07:00 | GBP | ILO Unemployment Rate (3M) Sep | 4.50% | 4.50% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Sep | 6.00% | 6.00% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Sep | 7.00% | 7.20% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 2.20% | 2.20% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 P | 0.60% | 0.70% | ||

| 13:15 | CAD | Housing Starts Y/Y Oct | 265K | 251K | ||

| 13:30 | USD | Retail Sales M/M Oct | 1.20% | 0.70% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Oct | 1.00% | 0.80% | ||

| 13:30 | USD | Import Price Index M/M Oct | 1.00% | 0.40% | ||

| 14:15 | USD | Industrial Production M/M Oct | 0.90% | -1.30% | ||

| 14:15 | USD | Capacity Utilization Oct | 75.90% | 75.20% | ||

| 15:00 | USD | Business Inventories Sep | 0.50% | 0.60% | ||

| 15:00 | USD | NAHB Housing Market Index Nov | 80 | 80 |