Dollar’s broad based rally continues in Asian session today and looks set to have a strong close for the week. Talking about weekly performance, Yen is following the greenback as the next strongest. New Zealand Dollar and Australian Dollar are competing for the worst performing spot. European majors are mixed with Euro, Sterling and Swiss Franc trading in range against each other too.

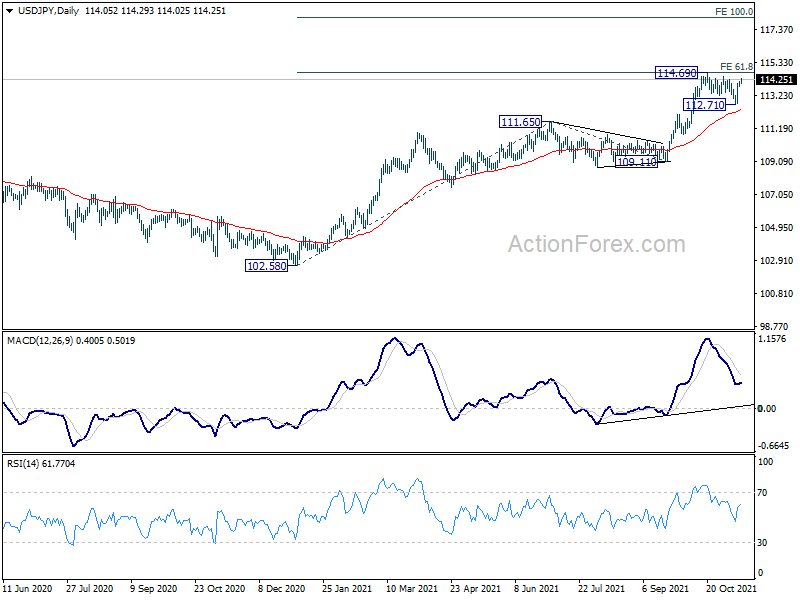

Technically, we’re still waiting for USD/JPY to break through 114.69 high to resume the medium term up trend for next projection target at 118.18. But given Yen’s strength elsewhere, it might take some more time for the pair to accomplish this breakout. That might also need a strong upside breakout in benchmark US yield to give it a hand.

{kind=link}

In Asia, at the time of writing, Nikkei is up 1.01%. Hong Kong HSI is up 0.22%. China Shanghai SSE is down -0.01%. Singapore Strait Times is down -0.01%. Japan 10-year JGB yield is up 0.0072 to 0.078.

SNB Maechler: We are still in a territory where the Swiss franc is high

SNB Board member Andrea Maechler said yesterday that “we are still in a territory where the Swiss franc is high.” “The reality is, we continue to have a safe-haven currency,” she said. “Uncertainties remain high, largely because of the COVID crisis which continues to be there.”

“You’ve seen recently there has been quite an appreciation of the Swiss franc,” Maechler said. “Now if you look at the real exchange rate, it’s still higher than 2015. It is something that we do continue to monitor, and we will continue to do so.”

Maechler reiterated that it’s necessary for the central bank to intervene in the markets.

New Zealand BusinessNZ manufacturing rose to 54.3, recovery from a large hard hit

New Zealand BusinessNZ Performance of Manufacturing Index rose from 51.6 to 54.3 in October. Looking at some details, production rose from 49.8 to 54.0. Employment dropped from 54.2 to 52.1. New orders dropped from 54.1 to 53.9. Finished stocks rose from 50.2 to 54.9. Deliveries rose from 47.9 to 59.9.

BNZ Senior Economist, Doug Steel stated that “even though October’s reading is above average, we’d classify it more in the realm of some recovery from a large hit rather than an indication of outright strength.”

Looking ahead

Swiss will release PPI in European session while Eurozone will release industrial production. US will release U of Michigan consumer sentiment later in the day.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1432; (P) 1.1460; (R1) 1.1477; More…

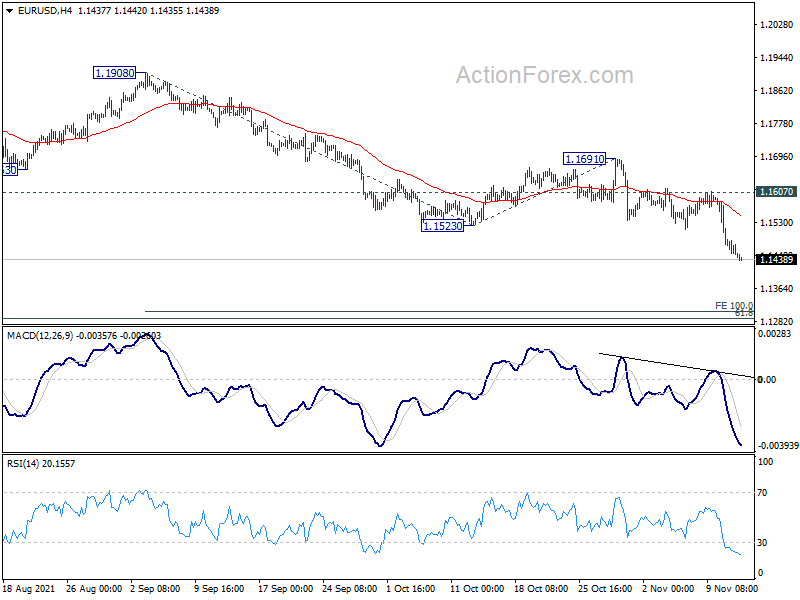

EUR/USD’s fall is still in progress and intraday bias stays on the downside. Current decline should now target 100% projection 1.1908 to 1.1523 from 1.1691 at 1.1453 at 1.1306, which is close to long term fibonacci level at 1.1289. On the upside, break of 1.1607 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

{kind=link}

In the bigger picture, price actions from 1.2348 should at least be a correction to rise from 1.0635 (2020 low). As long as 1.1691 resistance holds, deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289. Nevertheless break of 1.1691 resistance will revive medium term bullishness and turn focus back to 1.2348 high.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | BusinessNZ Manufacturing Index Oct | 54.3 | 51.4 | 51.6 | |

| 7:30 | CHF | Producer and Import Prices M/M Oct | 0.20% | |||

| 7:30 | CHF | Producer and Import Prices Y/Y Oct | 4.50% | |||

| 10:00 | EUR | Eurozone Industrial Production M/M Sep | -0.50% | -1.60% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Nov P | 72.5 | 71.7 |