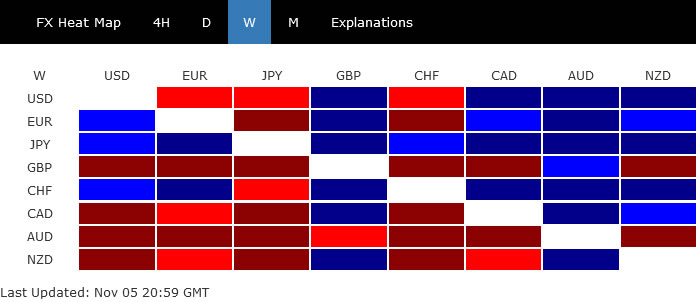

The developments last week were a bit confounding, as both stocks and bonds rallied notably. Yen and Swiss Franc followed the path of falling yields and rose as the biggest winner of the week.

Dollar was not much helped by Fed’s tapering and solid job data. Australia Dollar ignored broad risk-on sentiment, and ended as the worst performer after RBA hinted that it’s in no rush for rate hike. Sterling was the second worst after BoE disappointed those who expected an imminent hike.

The path ahead could depend on how far stocks would go, and how deep yields would fall, and the balance of the impacts on the currency markets. That would also very much depend on the upcoming inflation data from the US.

{kind=link}

Major benchmark yields tumbled

Major benchmark treasury yields tumbled sharply, reversing most of October’s gains. The moves came after central banks pushed back on market expectations on rate hikes. Even BoE refrained from raising interest rate despite recent rhetorics. Fed also still sounded patient after delivering tapering plan.

Germany 10-year bund yield closed at -0.278, comparing to October’s high at -0.060.

{kind=link}

UK 10-year gilt yield closed at 0.847, comparing to October’s high at 1.222.

{kind=link}

Japan 10-year JGB yield also dropped to close at 0.064, after hitting as high as 0.115 earlier this month.

{kind=link}

In the US, 10 year yield broke through 55 day EMA to close at 1.453. The development confirmed short term topping at 1.691. The consolidation pattern from 1.765 should be in the third leg and deeper decline could be seen in TNX to 61.8% retracement of 1.128 to 1.691 at 1.343, and possibly below. But we’re not expecting a break of 1.128 key support.

{kind=link}

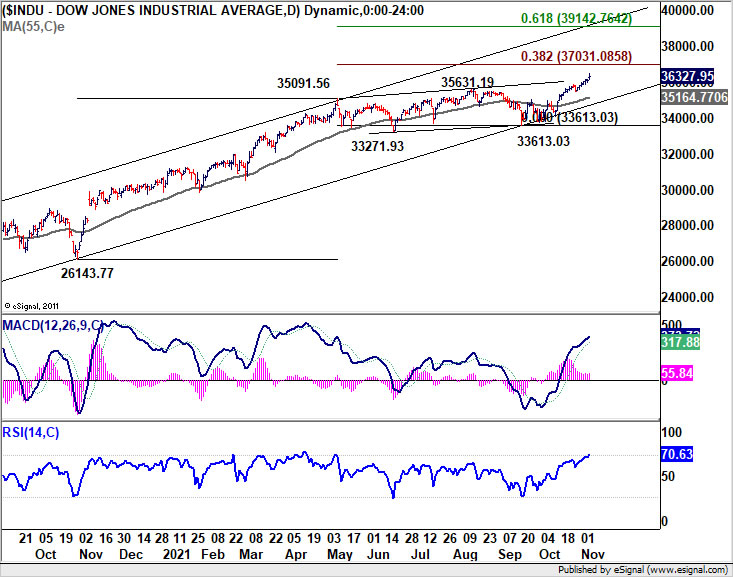

Major stock indexes surged to new records

On the other hand, major stock indexes in US and Europe surged to new record highs last week, including DOW, S&P 500, NASDAQ, DAX and CAC 40.

DOW extended record runs to close at 36327.95. For now, as long as last week’s low at 35797.97 holds, further rally should be seen to 38.2% projection of 26143.77 to 35091.56 from 33613.03 at 37031.08. Firm break there would push DOW further to 61.8% projection at 39142.76, which is close to 40k handle, in the early months of next year.

{kind=link}

Dollar index struggled to extend rally again

In spite of Fed’s tapering and a set of solid non-farm payroll data, Dollar struggled to extend gain, capped by risk-on sentiment and falling yields. Even EUR/USD’s break of 1.1523 low was half-hearted. Dollar index also failed to sustain above 94.46 fibonacci level again.

For now, near term outlook will stay bullish as long as 93.27 support holds. Sustained trading above 38.2% retracement of 102.99 to 89.20 at 94.46 should confirm medium term bullish reversal, and target 61.8% retracement at 97.72 next. However, break of 93.27 support will confirm rejection by 94.46, which retains medium term bearishness. Deeper fall would then be seen back towards 89.20.

{kind=link}

{kind=link}

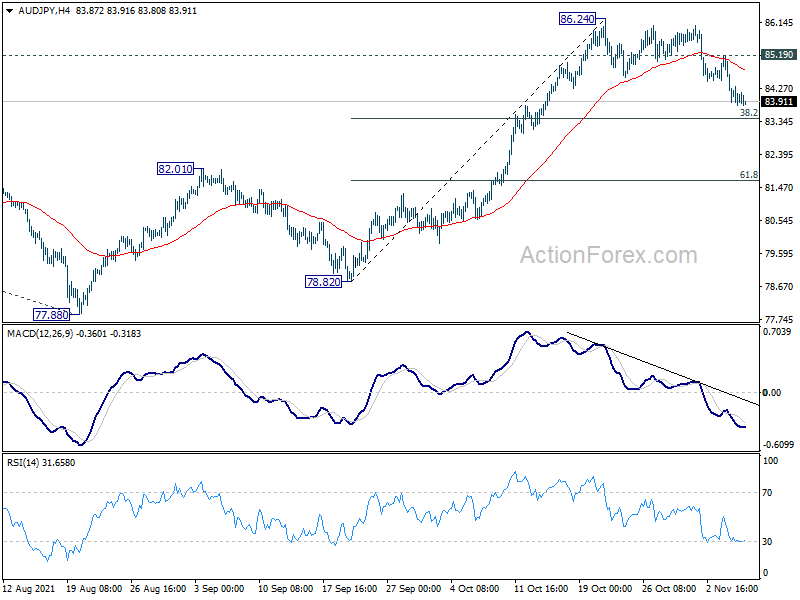

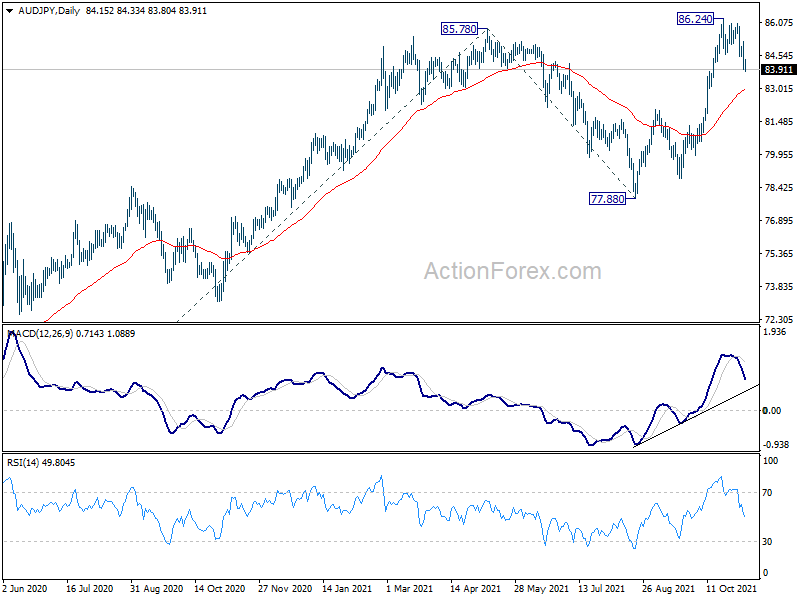

AUD/JPY extended near term correction

AUD/JPY was the biggest mover last week, extending the decline from 86.24 lower to close at 83.91. For now, such decline is still seen as a corrective move only. While further fall cannot be ruled out, we’d look for strong support from 38.2% retracement of 78.82 to 86.24 at 83.40 to contain downside and bring rebound.

Break of 85.19 will bring retest of 86.24 and then resumption of medium term up trend. That could come when the decline in treasury yield slows, or when Yen crosses recouple with risk-on sentiment. However, firm break of 83.50 will bring deeper fall towards 82.01 resistance turned support, and signal a broader change in overall sentiments.

{kind=link}

{kind=link}

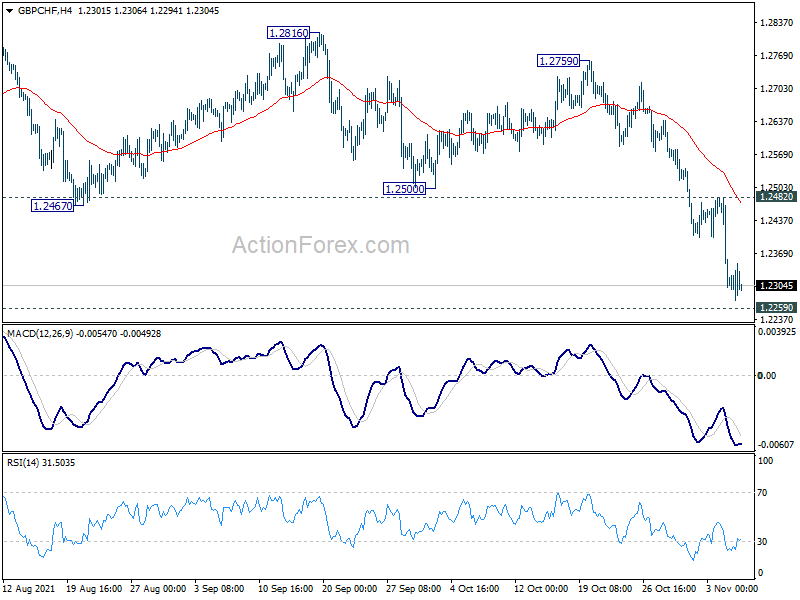

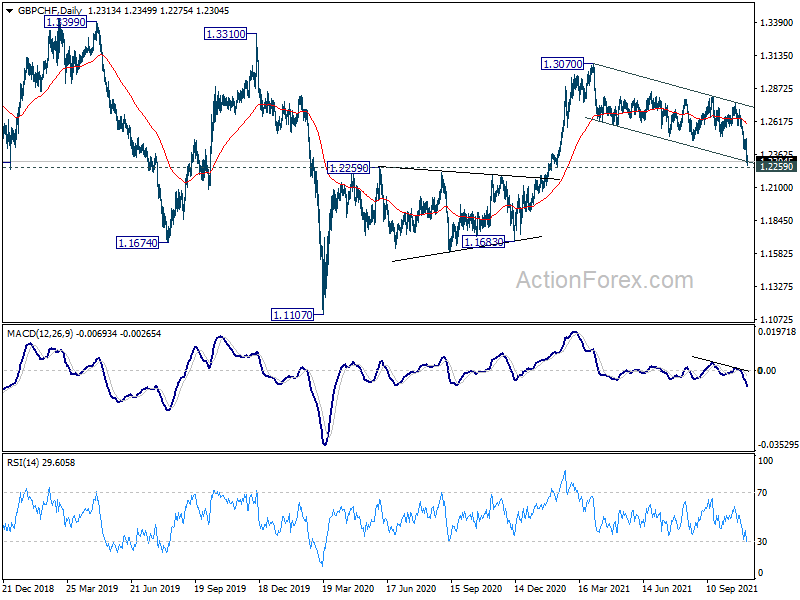

GBP/CHF eyes 1.2259 key support after steep fall

GBP/CHF was also one of the top movers, diving after BoE missed the rate hike expectation that it set the markets up. The downside acceleration is mixing the outlook a bit, and focus is immediately on 1.2259 key resistance turned support.

Strong rebound from 1.2259, followed by break of 1.2482 resistance should defend the case that fall from 1.3070 is merely a corrective move. Rise from 1.1107 low should still be in progress for resumption at a later stage.

However, sustained break of 1.2259 would argue that the medium term trend has reversed. There could even be some downside acceleration to follow to 1.1683 support next.

{kind=link}

{kind=link}

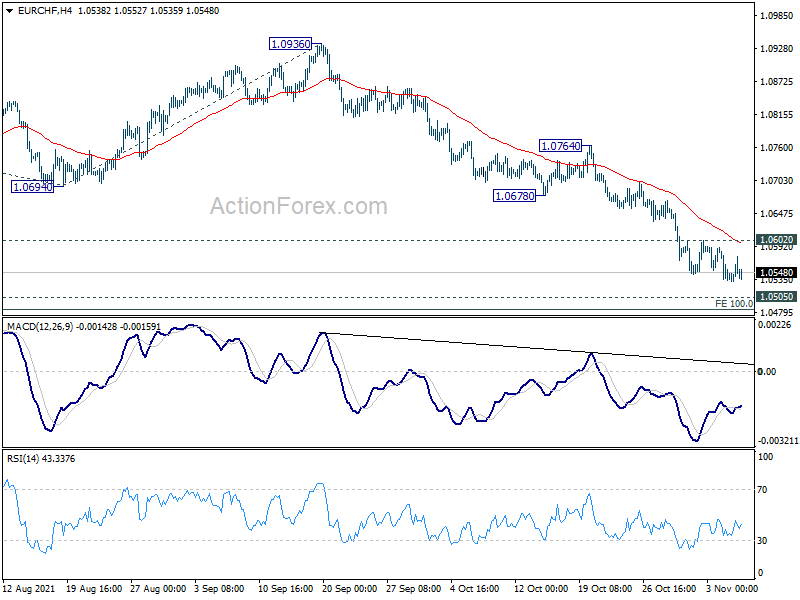

EUR/CHF Weekly Outlook

EUR/CHF dropped further to 1.0532 last week. Downside momentum diminished slightly but there is no sign of bottoming yet. Further fall is expected this week as long as 1.0602 resistance holds. Current down trend from 1.1159 would target 100% projection of 1.1149 to 1.0694 from 1.0936 at 1.0481. On the upside, however, break of 1.0602 will turn bias to the upside for stronger rebound back towards 1.0678 support turned resistance.

{kind=link}

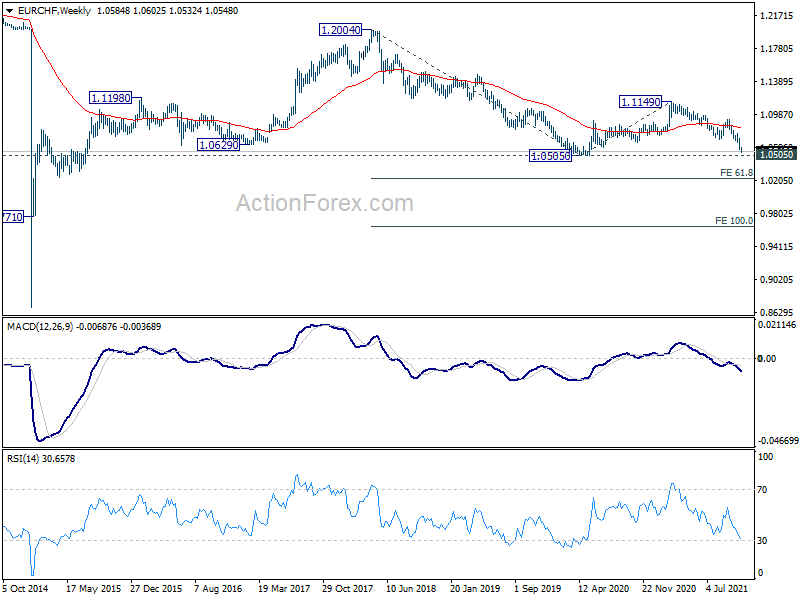

In the bigger picture, current downside momentum argues that fall from 1.1149 is probably resuming the down trend from 1.2004 (2018 high). Next focus is 1.0505 (2020 low). Decisive break there will confirm this bearish case and target 61.8% projection of 1.2004 to 1.0505 to 1.1149 at 1.0223 next. Strong support from 1.0505 will bring rebound first. But outlook will stay bearish as long as 1.0936 resistance holds.

{kind=link}

In the long term picture, rejection by 55 month EMA (now at 1.1015) maintains long term bearishness. Break of 1.0505 low will resume the down trend from 1.2004 to 61.8% projection of 1.2004 to 1.0505 to 1.1149 at 1.0223. Firm break there will target 100% projection at 0.9650.

{kind=link}

{kind=link}