Dollar and Yen dropped sharply overnight on strong risk-on market, as NASDAQ finally caught up and made new record high. The greenback is additionally pressured by the delayed buying in Euro after ECB post-meeting press conference. For now, Canadian Dollar is the third weakest, following the retreat in oil price. On the other hand, Aussie is the strongest one for the week on speculation that RBA would pull ahead rate hikes, while Swiss Franc and Kiwi follow.

Technically, we’re not too convinced by Euro’s buying yet, even though EUR/USD did resumed near term rebound. There is no sign in bottoming in EUR/CHF as recent fall from 1.0936 is extending. EUR/AUD is kept below 1.5598 minor resistance. Nevertheless, EUR/GBP is now pressing 0.8467 minor resistance while EUR/CAD is pressing 1.4439. Break of these two levels could sign that Euro’s rebound is more broad based. But, we’ll see.

{kind=link}

In Asia, Nikkei closed up 0.03%. Hong Kong HSI is down -0.52%. China Shanghai SSE is up 0.64%. Singapore Strait Times is up 0.52%. Japan 10-year JGB yield is up 0.0072 at 0.095. Overnight, DOW rose 0.68%. S&P 500 rose 0.98%. NASDAQ rose 1.39% to new record at 15448.11. 10-year yield rose 0.039 to 1.568.

Japan industrial production dropped -5.4% mom in Sep, but expected to bounce back strongly ahead

Japan industrial production dropped sharply by -5.4% mom in September, much worse than expectation of -2.4% mom. The seasonally adjusted index of production at factories and mines dropped for the third straight month to 89.5, against the 2015 100 base of 100.

But looking ahead, the Ministry of Economy, Trade and Industry said output would bounce back by 6.4% in October, and then 5.7% in November, based on a poll of manufacturers. An official said, “output may have hit bottom in September since economic activities have been returning to normal in countries such as Vietnam and Malaysia since late September, and a recovery is expected, mainly in the auto industry.”

Also released, unemployment was unchanged at 2.8% in September, matched expectations. Housing starts rose 4.3% yoy, versus expectation of 7.5% yoy. Consumer confidence dropped to 39.2, below expectation of 40.4. In October, Tokyo CPI core was unchanged at 0.10% yoy, below expectation of 0.3% yoy.

Australia retail sales rose 1.3% mom in Sep, vary by state

Australia retail sales rose 1.3% mom in September, much better than expectation of 0.2% mom. That’s the first monthly growth since May. For the 12-month, sales rose 1.7% yoy.

“Retail turnover continues to vary by state, based on whether restrictions were imposed, removed or extended. Queensland sales rose to their highest level ever, up 5.2 per cent, with no lockdowns in September,” Ben James, Director of Quarterly Economy Wide Statistics said.

“New South Wales also experienced a rise of 2.3 per cent despite having lockdowns, as some restrictions were eased or lifted. However, turnover for New South Wales remains 11.9 per cent lower than May 2021, the month before the most recent lockdown began.”

Also released, PPI came in at 1.1% qoq, 2.9% qoq in Q3, versus expectation of 0.6% qoq, 3.2% yoy. Price sector credit rose 0.6% mom in September, matched expectations.

France GDP grew 3.0% qoq in Q3, almost back to pre-crisis level

France GDP rose 3.0% qoq in Q3, above expectation of 2.4% qoq. GDP has almost returned to pre-crisis level, just -0.1% below Q4 2019 level.

Final internal demand (excluding inventory changes) contributed positively to GDP growth this quarter (+3.3 points, after +1.5 points in Q2): in particular, households’ consumption expenditure accelerated very strongly (+5.0% after +1.3%), and contributed for +2.5 points to GDP growth this quarter. Gross fixed capital formation (GFCF) was almost stable (-0.1% after +2.5% in the previous quarter).

Exports accelerated this quarter (+2.3% after +1.2% in the previous quarter) while imports were stable (–0.1% after +1.7%). Foreign trade remained largely below its pre-crisis level, but its contribution to GDP growth was positive this quarter: +0.6 points, after –0.2 points in the previous quarter. Finally, the contribution of inventory changes to GDP growth was negative this quarter (–0.9 points after +0.0 points in the previous quarter).

Looking ahead

Eurozone GDP and CPI flash, Germany GDP and Italy GDP will be released in European session. UK will release mortgage approvals and M4 money supply. Swiss will release retail sales and KOF economic barometer.

Later in the data, Canada will release GDP, IPPI and RMPI. US will release personal income and spending, and PCE inflation.

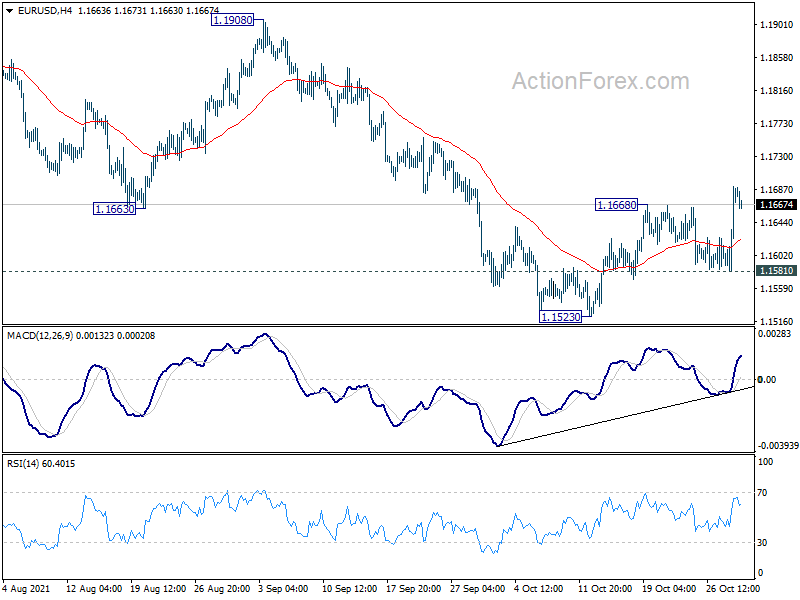

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1614; (P) 1.1653; (R1) 1.1724; More…

EUR/USD’s rebound from 1.1523 resumed by breaking 1.1668 temporary top. Intraday basis back on the upside for further rally. Sustained break of 55 day EMA (now at 1.1690) will be a sign that larger correction from 1.2348 has completed. Stronger rally would be seen to 1.1908 resistance for confirmation. On the downside, though, break of 1.1581 minor support will turn bias back to the downside for 1.1523 low instead.

{kind=link}

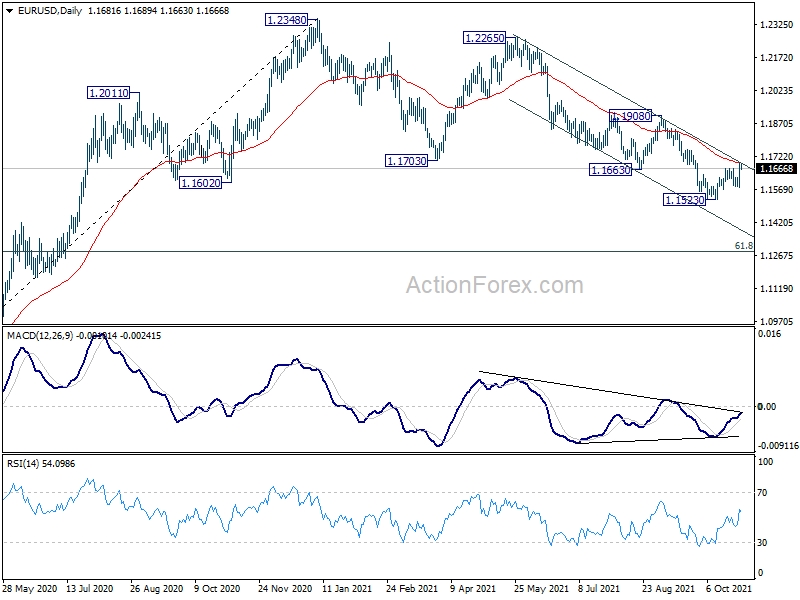

In the bigger picture, price actions from 1.2348 should at least be a correction to rise from 1.0635 (2020 low). As long as 1.1908 resistance holds, deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289. Nevertheless break of 1.1908 resistance will revive medium term bullishness and turn focus back to 1.2348 high.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Oct | 0.10% | 0.30% | 0.10% | |

| 23:30 | JPY | Unemployment Rate Sep | 2.80% | 2.80% | 2.80% | |

| 23:50 | JPY | Industrial Production M/M Sep P | -5.40% | -2.40% | -3.60% | |

| 0:30 | AUD | Private Sector Credit M/M Sep | 0.60% | 0.60% | 0.60% | |

| 0:30 | AUD | Retail Sales M/M Sep | 1.30% | 0.20% | -1.70% | |

| 0:30 | AUD | PPI Q/Q Q3 | 1.10% | 0.60% | 0.70% | |

| 0:30 | AUD | PPI Y/Y Q3 | 2.90% | 3.20% | 2.20% | |

| 5:00 | JPY | Housing Starts Y/Y Sep | 4.30% | 7.50% | 7.50% | |

| 5:30 | EUR | France Consumer Spending M/M Sep | -0.20% | 0.50% | 1.00% | 0.70% |

| 5:30 | EUR | France GDP Q/Q Q3 P | 3.00% | 2.40% | 1.10% | |

| 6:30 | CHF | Real Retail Sales Y/Y Sep | 0.50% | |||

| 7:00 | CHF | KOF Leading Indicator Oct | 108 | 110.6 | ||

| 8:00 | EUR | Italy GDP Q/Q Q3 P | 2.00% | 2.70% | ||

| 8:00 | EUR | Germany GDP Q/Q Q3 P | 2.20% | 1.60% | ||

| 8:30 | GBP | Mortgage Approvals Sep | 73K | 74K | ||

| 8:30 | GBP | M4 Money Supply M/M Sep | 0.50% | 0.50% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 2.10% | 2.20% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Oct P | 3.70% | 3.40% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct P | 1.90% | 1.90% | ||

| 12:30 | CAD | GDP M/M Aug | 0.70% | -0.10% | ||

| 12:30 | CAD | Industrial Product Price M/M Sep | -0.30% | |||

| 12:30 | CAD | Raw Material Price Index Sep | -2.40% | |||

| 12:30 | USD | Personal Income M/M Sep | 0.10% | 0.20% | ||

| 12:30 | USD | Personal Spending M/M Sep | 0.60% | 0.80% | ||

| 12:30 | USD | PCE Price Index M/M Sep | 0.30% | 0.40% | ||

| 12:30 | USD | PCE Price Index Y/Y Sep | 4.70% | 4.30% | ||

| 12:30 | USD | Core PCE Price Index M/M Sep | 0.20% | 0.30% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Sep | 3.70% | 3.60% | ||

| 12:30 | USD | Employment Cost Index Q3 | 0.90% | 0.70% | ||

| 13:45 | USD | Chicago PMI Oct | 63 | 64.7 | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Oct F | 71.4 | 71.4 |