Australian Dollar rises broadly today with support from strong inflation data. But upside is capped by mildly negative investment sentiment in Asia. While DOW and S&P 500 made new records overnight, there is no follow through in risk-on sentiment. Overall currency markets are mixed, with Yen as second strongest so far. Dollar is the weakest followed by Canadian Dollar. The Loonie is looking forward to BoC tapering and forward guidance.

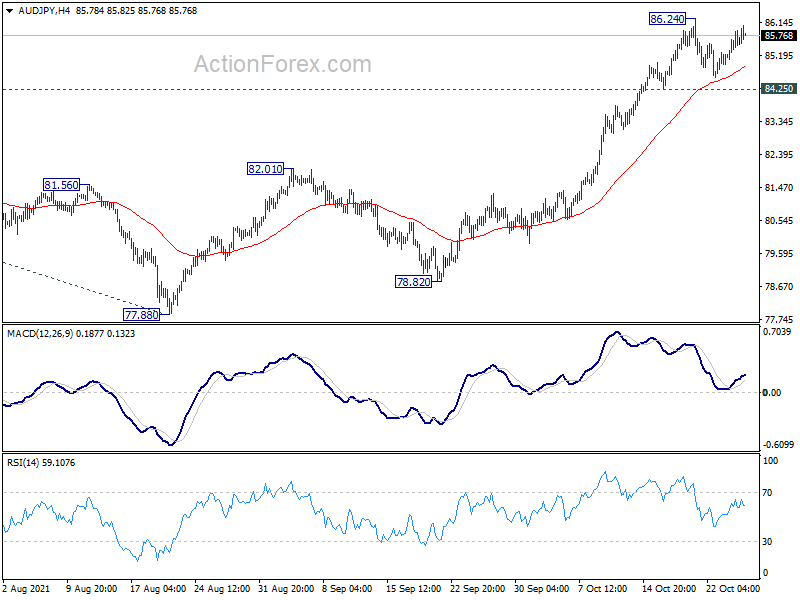

Technically, while Aussie rises, both AUD/USD and AUD/JPY are stuck in near term range. Focus will be on 0.7545 temporary top in AUD/USD and 86.24 in AUD/JPY. Firm break of these levels together should confirm underlying rally in Aussie, that could be seen elsewhere, in particular against Euro.

{kind=link}

In Asia, at the time of writing, Nikkei is down -0.41%. Hong Kong HSI is down -1.46%. China Shanghai SSE is down -0.90%. Singapore Strait Times is up 0.61%. Japan 10-year JGB yield is down -0.0004 at 0.104. Overnight, DOW rose 0.04%. S&P 500 rose 0.18%. NASDAQ rose 0.06%. 10-year yield dropped -0.016 to 1.619.

Australia trimmed mean and weighted median CPI rose to highest in over 5 yrs

Australia CPI rose 0.8% qoq in Q3, matched expectations. Over the 12-month period, headline CPI slowed from 3.8% yoy to 3.0% yoy. Trimmed mean CPI jumped from 1.6% yoy to 2.1% yoy. Weighted median CPI rose from 1.6% yoy to 2.1% yoy too. Both trimmed mean and weighted mean CPI readings were highest in over five years, and the first annual movements above 2% since September 2015 quarter.

Head of Prices Statistics at the ABS, Michelle Marquardt said the most significant price rises in the September quarter were new dwellings (+3.3 per cent) and automotive fuel (+7.1 per cent).

New Zealand reports record imports and trade deficit in Sep

New Zealand goods exports rose 10% yoy or NZD 387B to NZD 4.4B in September. Goods imports rose 30% yoy or NZD 1.5B to NZD 6.6B. Trade deficit came in at NZD -2.2B, versus expectation of NZD -0.8B. The set of data marked the third successive month of record imports, resulting in a record trade deficit.

Exports to China rose 25%, to Australia dropped -8.4%, to US rose 23%, to EU rose -10%, and to Japan dropped -5.5%. Imports from China rose 48%, from EU rose 29%, from Australia rose 28%, from US dropped -2.1%, from Japan rose 41%.

“These three consecutive record months for imports are a reflection of both the higher prices New Zealanders are paying for consumer goods, and strong demand for capital goods such as machinery used in construction, and passenger vehicles,” international trade manager Alasdair Allen said.

New Zealand ANZ business confidence dropped to 13.4 in Oct

New Zealand ANZ Business Confidence was finalized at -13.4 in October, down from September’s -7.2. Own Activity Outlook rose from prior month’s 18.2 to 21.7. Export intentions rose from 7.4 to 8.6. Investment intentions rose from 9.2 to 13.8. Employment intentions dropped from 14.1 to 10.9. Cost expectations rose from 84.2 to 87.2. Pricing expectations rose from 58.1 to 65.5. Inflation expectations rose further from 3.02 to 3.45.

ANZ said: “Despite living week to week to some extent, firms appear to be getting on with it as best they can. There are clearly challenges, with costs extremely high and profits expected to fall, but more positively, activity expectations, investment intentions and employment intentions are holding up. The COVID situation remains unpredictable, however, and we’ll be watching closely for any evidence of that uncertainty derailing plans.”

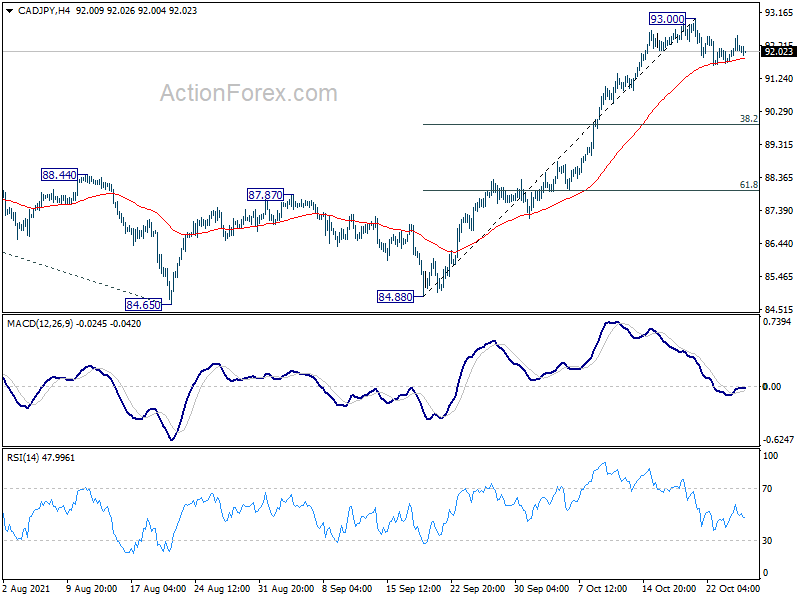

BoC to taper again, CAD/JPY in consolidation but stays bullish

BoC is widely expected to continue tapering today, by announcing to lower weekly asset purchases by CAD 2B to CAD 1B. Also, the central bank would set the plan to end QE in December. Markets are currently pricing in three rate hikes in 2022, and would be eager to see any adjustment in the forward guidance to affirm such expectations. But BoC would probably hold their cards until December, and just reiterate that policy rate would stay at “the effective lower bound until economic slack is absorbed so that the 2 percent inflation target is sustainably achieved”.

Some previews on BoC:

CAD/JPY turned into sideway consolidations after hitting 93.00 last week, but overall bullish outlook is unchanged. Deeper pull back cannot be ruled out. But downside should be contained by 38.2% retracement of 84.88 to 93.00 at 89.89 to bring rebound. Meanwhile, break of 93.00 will resume larger up trend from 73.80. Next target is 61.8% projection of 73.80 to 91.16 from 84.65 at 95.37.

{kind=link}

{kind=link}

Looking ahead

Germany will release Gfk consumer sentiment in European session. Eurozone will release M3 money supply. Swiss will release Credit Suisse economic expectations.

Later in the day, US will release durable goods orders, trade balance and wholesale inventories. Canada will release BoC rate decisions.

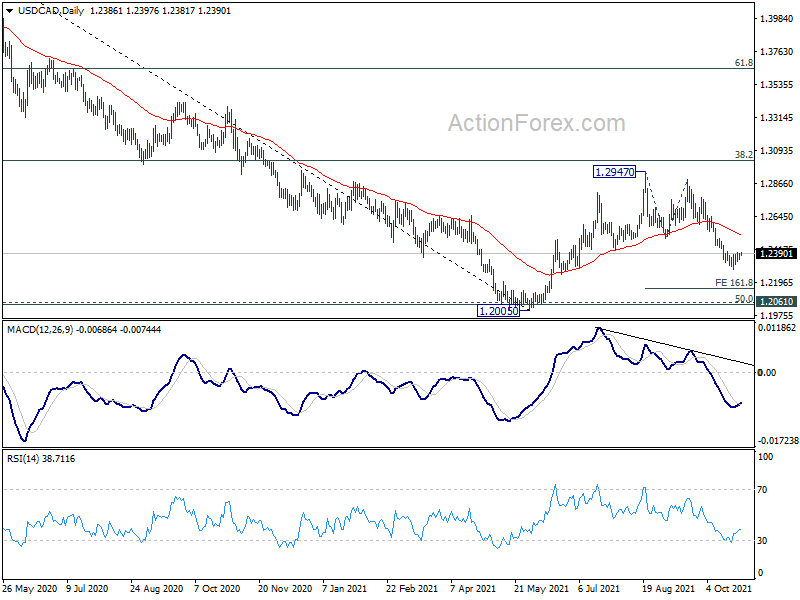

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2360; (P) 1.2379; (R1) 1.2407; More…

Intraday bias in USD/CAD remains neutral at this point, as consolidation form 1.2286 temporary low is extending. Upside of recovery should be limited by 1.2497 resistance to bring fall resumption. On the downside, break of 1.2286 will resume the fall from 1.2947 to 161.8% projection of 1.2947 to 1.2492 from 1.2894 at 1.2158 next.

{kind=link}

In the bigger picture, the rejection by 38.2% retracement of 1.4667 to 1.2005 at 1.3022 argues that rebound from 1.2005 is merely a corrective rise, which is complete. More importantly, the down trend from 1.4667 (2020 high) is not over yet. Sustained break of 1.2005 will extend the down trend to next long term fibonacci level at 61.8% retracement of 0.9406 to 1.4689 at 1.1424. In any case, outlook will not turn bullish as long as 1.2947 resistance holds.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Sep | -2171M | -762M | -2144M | -2139M |

| 23:01 | GBP | BRC Shop Price Index Y/Y Sep | -0.40% | -0.50% | ||

| 0:00 | NZD | ANZ Business Confidence Oct | -13.4 | -8.6 | ||

| 0:30 | AUD | CPI Q/Q Q3 | 0.80% | 0.80% | 0.80% | |

| 0:30 | AUD | CPI Y/Y Q3 | 3.00% | 3.80% | 3.80% | |

| 0:30 | AUD | RBA Trimmed Mean CPI Q/Q Q3 | 0.70% | 0.50% | 0.50% | |

| 0:30 | AUD | RBA Trimmed Mean CPI Y/Y Q3 | 2.10% | 1.60% | 1.60% | |

| 6:00 | EUR | Germany Gfk Consumer Confidence Nov | -0.4 | 0.3 | ||

| 8:00 | CHF | Credit Suisse Economic Expectations Oct | 25.7 | |||

| 8:00 | EUR | Eurozone M3 Money Supply Y/Y Sep | 7.70% | 7.90% | ||

| 12:30 | USD | Durable Goods Orders Sep | -1.10% | 1.80% | ||

| 12:30 | USD | Durable Goods Orders ex Transportation Sep | 0.40% | 0.30% | ||

| 12:30 | USD | Goods Trade Balance (USD) Sep P | -88.2B | -87.6B | ||

| 12:30 | USD | Wholesale Inventories Sep P | 1.00% | 1.20% | ||

| 14:00 | CAD | BoC Interest Rate Decision | 0.25% | 0.25% | ||

| 14:30 | USD | Crude Oil Inventories | -0.4M | |||

| 15:00 | CAD | BoC Press Conference |