The forex markets are generally staying in consolidative mode today, with Euro and Swiss Franc trading mildly higher. Meanwhile, Aussie is leading other commodity currencies for retreats. Dollar is also trying to firm up with 10-year yield breaking above 1.62 handle. Yen, is also mildly higher with help from some pull back in stocks. Overall, the markets could need some more time to digest recent moves, before resuming.

Technically, we’d continue to focus on whether EUR/USD would break through 1.1639 resistance to confirm short term bottoming at 1.1523. Or, it will resume larger fall from 1.2265 through 1.1523. That could provide hint on Dollar’s next move elsewhere. At the same time, we’d also see if EUR/CHF would break through 1.0750 minor resistance, or 1.0678 temporary low. Synchronized rallies in the two pairs will indicate it’s Euro that’s moving instead.

In Europe, at the time of writing, FTSE is down -0.50%. DAX is down -0.80%. CAC is down -0.98%. Germany 10-year yield is up 0.039 at -0.125. Earlier in Asia, Nikkei dropped -0.15%. Hong Kong HSI rose 0.31%. China Shanghai SSE dropped -0.12%. Singapore Strait Times closed flat. Japan 10-year JGB yield rose 0.0154 to 0.096.

ECB Visco: Some flexibility should remain in asset purchases to help against unexpected shocks

Governing Council member Ignazio Visco said even if the inflation pressures in Eurozone “may last for some months and well during the next year”, it’s still “largely transitory”. He added that market expectations for rate hike in late 2022 were “not that consistent” with ECB’s forward guidance.

Visco also said “flexibility should remain” after the emergency PEPP program as. “We certainly have to discuss how to adjust our purchase programs,” he said. “It will help against unexpected shocks, and it will help to avoid fragmentation that may rise again.”

New Zealand CPI rose 2.2% qoq, 4.9% in Q3, highest in over a decade

New Zealand CPI rose 2.2% qoq in Q3, well above expectation of 1.4% qoq. That’s the largest quarterly increase in over a decade since 2010. For the 12-month period, CPI accelerated to 4.9% yoy, up from Q2’s 3.3% yoy, well above expectation of 4.1% yoy too. The annual rise is also the highest since 2011. The strong inflation reading prompted more expectations of more RBNZ rate hikes ahead, following the 25bps increase earlier this month.

China GDP growth slowed to 0.2% qoq, 4.9% yoy in Q3

China GDP grew 4.9% yoy in Q3, below expectation of 5.2% yoy. On a quarterly basis, GDP grew only 0.2% qoq, slowed from Q2’s 1.2% qoq, and missed expectation of 0.5% qoq. In September, retail sales rose 4.4% yoy, above expectation of 3.3% yoy. Industrial production rose 3.1% yoy, below expectation of 4.5% yoy. Fixed asset investment rose 7.3% ytd yoy, below expectation of 7.9%.

“The overall national economy maintained the recovery momentum in the first three quarters … however, we must note that the current uncertainties in the international environment are mounting and the domestic economic recovery is still unstable and uneven,” said NBS spokesman Fu Linghui.

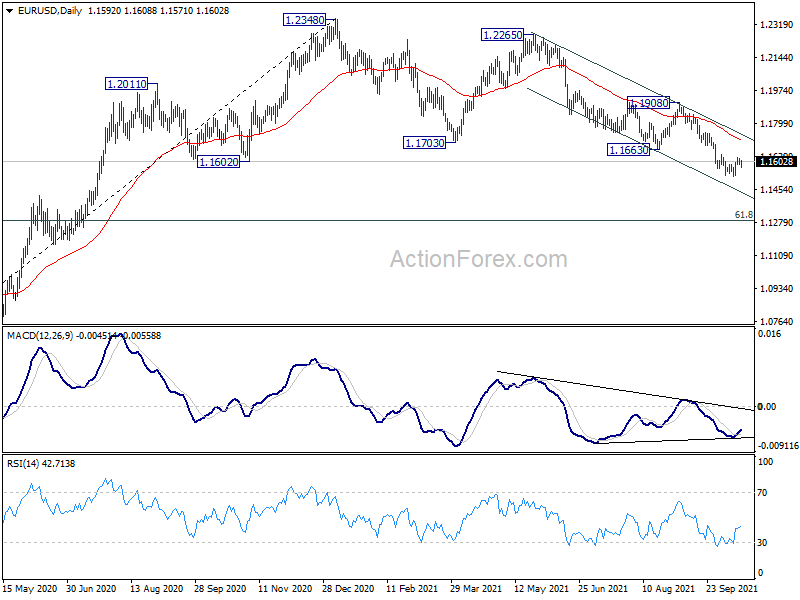

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1585; (P) 1.1602; (R1) 1.1616; More…

EUR/USD is still staying in consolidation from 1.1523 and intraday bias remains neutral. Further decline is still in favor as long as 1.1639 minor resistance holds. Break of 1.1523 will resume larger decline towards 1.1289 medium term fibonacci level. On the upside, break of 1.1639 resistance, however, will indicate short term bottoming. intraday bias will be turned back to the upside for stronger rebound, to 55 day EMA (now at 1.1712).

{kind=link}

In the bigger picture, price actions from 1.2348 should at least be a correction to rise from 1.0635 (2020 low). As long as 1.1908 resistance holds, deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289. Nevertheless break of 1.1908 resistance will revive medium term bullishness and turn focus back to 1.2348 high.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q3 | 2.20% | 1.40% | 1.30% | |

| 21:45 | NZD | CPI Y/Y Q3 | 4.90% | 4.10% | 3.30% | |

| 23:01 | GBP | Rightmove House Price Index M/M Oct | 1.80% | 0.30% | ||

| 02:00 | CNY | GDP Y/Y Q3 | 4.90% | 5.20% | 7.90% | |

| 02:00 | CNY | Retail Sales Y/Y Sep | 4.40% | 3.30% | 2.50% | |

| 02:00 | CNY | Industrial Production Y/Y Sep | 3.10% | 4.50% | 5.30% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Sep | 7.30% | 7.90% | 8.90% | |

| 12:15 | CAD | Housing Starts Y/Y Sep | 251K | 265K | 260K | 263K |

| 12:30 | CAD | Foreign Securities Purchases (CAD) Aug | 26.30B | 14.19B | 14.06B | |

| 13:15 | USD | Industrial Production M/M Sep | 0.20% | 0.40% | ||

| 13:15 | USD | Capacity Utilization Sep | 76.50% | 76.40% | ||

| 14:00 | USD | NAHB Housing Market Index Oct | 75 | 76 | ||

| 14:30 | CAD | BoC Business Outlook Survey |