Dollar jumps sharply in after data shows strong rise in retail sales, versus expectation of a decline. The data also raises optimism that it’s just the start of resurgence in consumer demand, as the world is exiting the pandemic with fast vaccinations. Canadian Dollar is following closely as the second strongest for the day. On the other hand Euro and Swiss Franc are suffering steep decline.

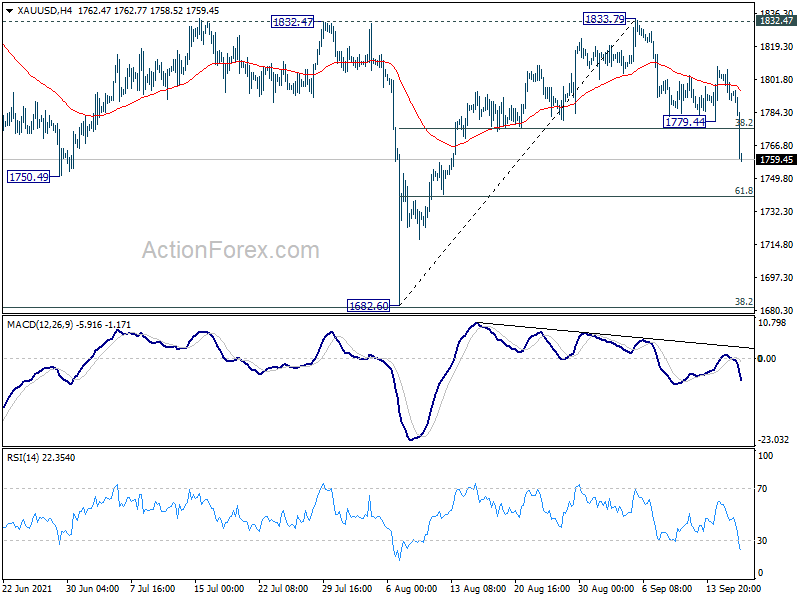

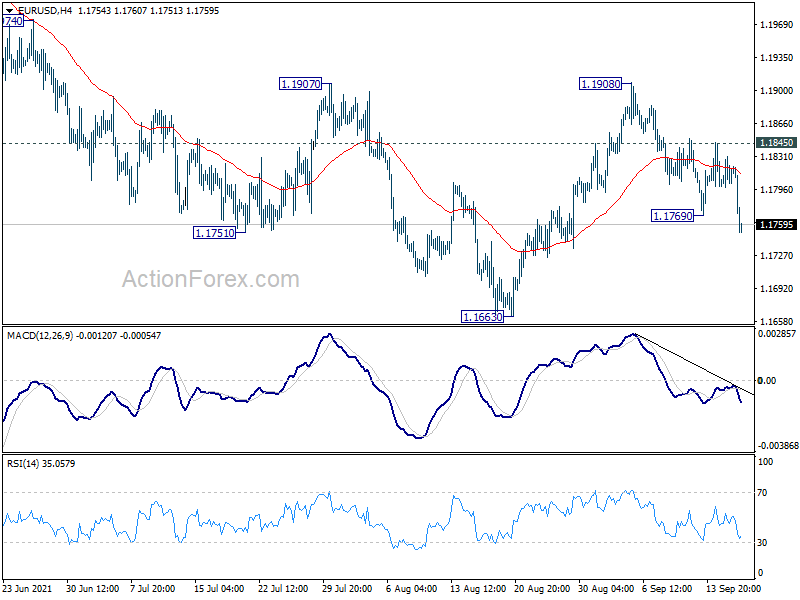

Technically, EUR/USD’s break of 1.1769 suggests resumption of fall from 1.1908 for retesting 1.1663 low. USD/CHF is pressing 0.9273 resistance and firm break there will resume whole rise from 0.8925. USD/JPY’s strong rebound also suggests that 109.10 support is well defended. At the same times, gold drops sharply through 1779.44 today, and it’s heading back to 61.8% retracement of 1682.60 to 1833.79 at 1740.35. These developments affirm Dollar’s underlying buying together.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.48%. DAX is up 0.74%. CAC is up 1.17%. Germany 10-year yield is up 0.0183 at -0.286, above -0.3 handle. Earlier in Asia, Nikkei dropped -0.62%. Hong Kong HSI dropped -1.46%. China Shanghai SSE dropped -1.34%. Singapore Strait Times rose 0.19%. Japan 10-year JGB yield rose 0.0092 to 0.045.

US retail sales rose 0.7% in Aug, ex-auto sales jumped 1.8%

US retail sales rose 0.7% mom to USD 618.7B in August, much better than expectation of -0.7% decline. Ex-auto sales rose 1.80% mom, versus expectation of -0.1% decline. Ex-gasoline sales rose 0.8% mom. Ex-auto, ex-gasoline sales rose 2.0% mom. Total sales for the June 2021 through August 2021 period were up 16.3% from the same period a year ago

US initial jobless claims rose 20k to 332k

US initial jobless claims rose 20k to 332k in the week ending September 11, above expectation of 316k. Four-week moving average of initial claims dropped -4k to 336k, lowest since March 14, 2020.

Continuing claims dropped -187k to 2665k in the week ending September 4, lowest since March 14, 2020. Four-week moving average of initial claims dropped -50k to 2808k, lowest since March 21, 2020.

Also released, Philly Fed manufacturing survey jumped to 30.7 in September, versus expectation of 18.9.

Canada housing starts dropped to 260k in August. Wholesale sales dropped -2.1% mom in July. ADP employment rose 39.4k in August.

ECB Rehn confidence to ensure favorable financing conditions when exiting crisis measures

ECB Governing Council member Olli Rehn said while growth in Eurozone is robust, supported is still needed. The outlook is clouded by bottlenecks as well as coronavirus variants.

The central bank is expected to debate in December on timing and the way to wind down the PEPP purchases. Rehn said he’s confident to find a ” viable and meaningful way of ensuring favorable financing conditions when we start our very gradual transition from the crisis measures to the next normal.”

He also urged governments to prepare for the eventual rise in borrowing cost even though a rate hike is “not yet within sight”. “It will nevertheless one day take place,” Rehn said. “This should be taken into account in budgetary planning in all the euro area countries.”

Eurozone exports rose 11.4% yoy in Jul, imports rose 17.1% yoy

Eurozone exports of goods to the rest of the world rose 11.4% yoy in July to EUR 206.0B. Imports rose 17.1% yoy to EUR 185.3B. As a result, Eurozone recorded a EUR 20.7B surplus in trade, Intra-Eurozone trade rose 16.8% yoy to EUR 179.7B.

In seasonally adjusted term, Eurozone exports rose 1.0% mom while imports rose 0.3%. Trade surplus widened from EUR 119.0B to EUR 13.4B, below expectation of EUR 16.8B. Intra-Eurozone trade rose from EUR 175.5B to EUR 178.0B.

SECO downgrades Swiss 2021 GDP forecast to 3.2%

SECO downgraded Swiss GDP growth forecast to 3.2% in 2021, comparing to June forecast of 3.6%. Growth is projected to further accelerate to 3.4% in 2022. It added that “the economic recovery is set to continue as expected, though growth is initially less dynamic than forecast previously.” Nevertheless, “economic activity is likely to have exceeded pre-crisis levels during the summer.”

SECO added, “highly exposed sectors such as international tourism are likely to emerge from the crisis more hesitantly”. But, “provided that severely restrictive measures such as business lockdowns are not imposed in the coming months, the economic recovery should continue uninterrupted.”

Japan: Economy’s pace weakened in severe pandemic situation

Japanese Government’s Cabinet office maintained that the economy “remains in picking up”, but added that “pace has weakened in a severe situation due to the Novel Coronavirus” In particular, “some weakness s seen recently” in industrial production, even though it’s still “picking up”.

Other assessments are largely unchanged, with private consumption showing weakness further. Business is picking up while exports continue to increase moderately. Corporate profits are also picking up with some weakness in non-manufacturers. Employment situation shows steady movements in some components.

Japan exports grew 26.2% yoy in Aug, imports rose 44.7% yoy

Japan’s export grew 26.2% yoy to JPY 6605B in August. That’s the sixth straight month of double-digit annual growth, as boosted by strong demand for chip-making equipment. By destination, exports to China, the largest trading partner, grew 12.6% yoy. Exports to Asia as a whole rose 26.1% yoy. Exports to the US rose 22.8% yoy. Exports to EU rose 29.9% yoy.

Imports jumped 44.7% yoy to JPY 7241B, due to stronger demand for fuel and medical goods. Trade balance came in at JPY -635B deficit, the largest shortfall since December 2021.

In seasonally adjusted term, exports rose 0.8% mom to JPY 7104B. Imports rose 4.6% mom to JPY 7276B. Trade deficit came in at JPY -272B versus expectation of JPY 80B surplus.

Australia employment dropped -146.3k in Aug, people also dropping out of labor force

Australia employment dropped -146.3k in August, even worse than expectation of -70.0k. Full-time jobs dropped -68k while part-time jobs dropped -78.2k.

Unemployment rate, on the other hand, dropped -0.1% to 4.6%, versus expectation 4.9%. But that’s due to a sharp fall in participation rate by -0.8% to 65.2%. Monthly hours worked dropped -66m hours or -3.7% mom.

Bjorn Jarvis, head of labour statistics at the ABS, said: “The fall in the unemployment rate reflects a large fall in participation during the recent lockdowns, rather than a strengthening in labour market conditions.

“Throughout the pandemic we have seen large falls in participation during lockdowns — a pattern repeated over the past few months. Beyond people losing their jobs, we have seen unemployed people drop out of the labour force, given how difficult it is to actively look for work and be available for work during lockdowns.

New Zealand GDP grew 2.8% qoq in Q2, well above expectation

New Zealand GDP grew 2.8% qoq in Q2, well above expectation of 1.2% qoq. Growth was led by service industries, which rose 2.8% qoq. Primary industries rose 5.0% qoq. Goods producing industries rose 1.3% qoq.

“The June 2021 quarter experienced fewer COVID-19 restrictions than previous quarters affected by COVID-19. Many industries experienced activity at or above pre-COVID-19 levels, while some remained below,” national accounts senior manager Paul Pascoe said.

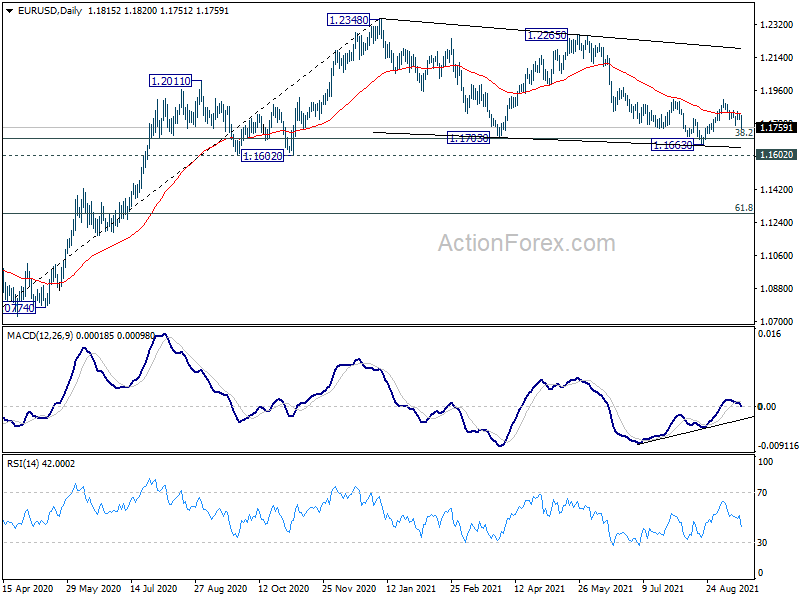

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1799; (P) 1.1816; (R1) 1.1832; More…

EUR/USD’s fall from 1.1908 resumes by breaking 1.1769 and intraday bias is back on the downside for 1.1663 low first. Break there will resume the fall from 1.2265, as well as the pattern from 1.2348. Next target is 1.1602 key support level. On the upside, above 1.1845 minor resistance will turn bias back to the upside for 1.1908 resistance instead.

{kind=link}

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally remains in favors long as 1.1602 support holds, to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). However sustained break of 1.1602 will argue that the rise from 1.0635 is over, and turn medium term outlook bearish again. Deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289 and below.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q2 | 2.80% | 1.20% | 1.60% | 1.40% |

| 23:50 | JPY | Trade Balance (JPY) Aug | -0.27T | 0.08T | 0.05T | -0.01T |

| 01:00 | AUD | Consumer Inflation Expectations Sep | 4.40% | 3.30% | ||

| 01:30 | AUD | Employment Change Aug | -146.3K | -70.0K | 2.2K | 3.1K |

| 01:30 | AUD | Unemployment Rate Aug | 4.50% | 4.90% | 4.60% | |

| 01:30 | AUD | RBA Bulletin Q2 | ||||

| 05:45 | CHF | SECO Economic Forecasts | ||||

| 08:00 | EUR | Italy Trade Balance (EUR) Jul | 8.76B | 6.22B | 5.68B | 5.67B |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jul | 13.4B | 16.8B | 12.4B | |

| 12:15 | CAD | Housing Starts Y/Y Aug | 260K | 270K | 272K | |

| 12:30 | CAD | ADP Employment Change Aug | 39.4K | 221.3K | ||

| 12:30 | CAD | Wholesale Sales M/M Jul | -2.10% | -2.00% | -0.80% | |

| 12:30 | USD | Retail Sales M/M Aug | 0.70% | -0.70% | -1.10% | -1.80% |

| 12:30 | USD | Retail Sales ex Autos M/M Aug | 1.80% | -0.10% | -0.40% | -1.00% |

| 12:30 | USD | Initial Jobless Claims (Sep 10) | 332K | 316K | 310K | 312K |

| 12:30 | USD | Philadelphia Fed Manufacturing Sep | 30.7 | 18.9 | 19.4 | |

| 14:00 | USD | Business Inventories Jul | 0.50% | 0.80% | ||

| 14:30 | USD | Natural Gas Storage | 76B | 52B |