Souring risk sentiment continues to support Swiss Franc and Yen today, while Dollar is also trying to catch up. Commodity currencies are still the weakest ones. In particular, New Zealand Dollar tumbles on talks that RBNZ could refrain from delivering the highly anticipated rate hike tomorrow, as the country returned to pandemic lockdown. Fresh selling is also seen in Euro and Sterling, we markets enter into US session.

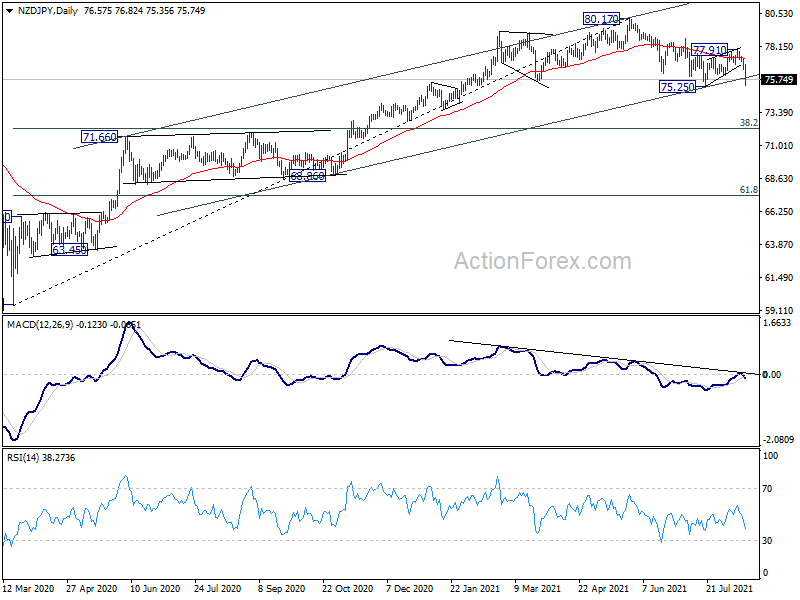

Technically, NZD/JPY is now eyeing 75.25 support with today’s steep fall. Break there will resume the corrective decline from 80.17, to 38.2% retracement of 59.49 to 80.17 at 72.27. Theoretically, such development should also come with break of 0.6879 in NZD/USD, to resume the fall from 0.7463.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.22%. DAX is down -0.09%. CAC is down -0.45%. Germany 10-year yield is down -0.013 at -0.478. Earlier in Asia, Nikkei dropped -0.36%. Hong Kong HSI dropped -1.66%. China Shanghai SSE dropped -2.00%. Singapore Strait Times dropped -0.86%. Japan 10-year JGB yield dropped -0.0071 to 0.009.

US retail sales dropped -1.1% mom in Jul, ex-auto sales dropped -0.4% mom

US retail sales dropped -1.1% mom in July to USD 61.7B, worse than expectation of -0.2% mom. Ex-auto sales dropped -0.4% mom, below expectation of 0.1% mom. Ex-gasoline sales dropped -1.4% mom. Ex-auto, ex-gasoline sales dropped -0.7% mom. Comparing to July 2020, sales were up 15.8% yoy. Total sales for May through July period were up 20.6% from the same period a year ago.

From Canada, housing starts dropped to 272k in July, below expectation of 275k. Foreign securities purchases dropped to CAD 19.63B in June.

Eurozone GDP grew 2.0% qoq in Q2, EU up 1.9% qoq

According to a flash estimate by the Eurostat, Eurozone GDP grew 2.0% qoq in Q2, and 1.9% qoq in the EU. Comparing with the same quarter of the previous year, GDP rose 13.6% yoy in Eurozone, and 13.2% yoy in the EU. Employment grew 0.5% qoq in Eurozone and 0.6% qoq in EU.

UK unemployment rate dropped to 4.7% in Jun, employment rate rose to 75.1

UK unemployment rate dropped slightly to 4.7% in the three months to June, down from 4.8%, better than expectation of 4.8%. That’s still 0.8% higher than before the pandemic, but -0.2% lower than the previous quarter. Employment rates was estimated at 75.1%, up 0.3% by the quarter, but still at -1.5% lower than before the pandemic.

ONS said: “The quarterly increase in employment was mainly driven by an increase in the number of full-time workers, which reached its highest level since before the start of the pandemic. While the number of people working part-time has decreased during the pandemic, in April to June 2021 there was the first quarterly increase in people working part-time since February to April 2020”.

Average earnings including bonus rose 8.8% 3moy, versus expectation of 8.7%. Average earnings excluding bonus rose 7.4% 3moy, matched expectations. In July, claimant count dropped -7.8k.

RBA minutes: Central scenario still for the economy to growth strongly again next year

In the minutes of August 3 meeting, RBA said recent outbreaks of the Delta variant of had “interrupted the recovery”. But the economy entered lockdowns with “more momentum than previously expected”, with fiscal and monetary support already cushion the economic effects. It added, “experience to date had been that, once virus outbreaks were contained, the economy bounced back quickly.” The “central scenario” was still for the economy to “growth strongly again next year”.

Committee members considered the case to delay tapering of asset purchases to AUD 4B a week scheduled for September. But they noted that additional bond purchases would only have a “marginal effect” at present”, but “maximum effect” during the resumption of strong growth in 2022. Also fiscal policy is recognized as a “more appropriate instrument” in response to a “temporary, localized reduction in incomes”. Thus, the Board reaffirmed the previously announced schedule for tapering.

RBA also reiterated that the condition for raising interest rate is not expected to be met before 2024. “Meeting this condition will require the labour market to be tight enough to generate wages growth that is materially higher than it is currently,” it said.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1762; (P) 1.1782; (R1) 1.1795; More…

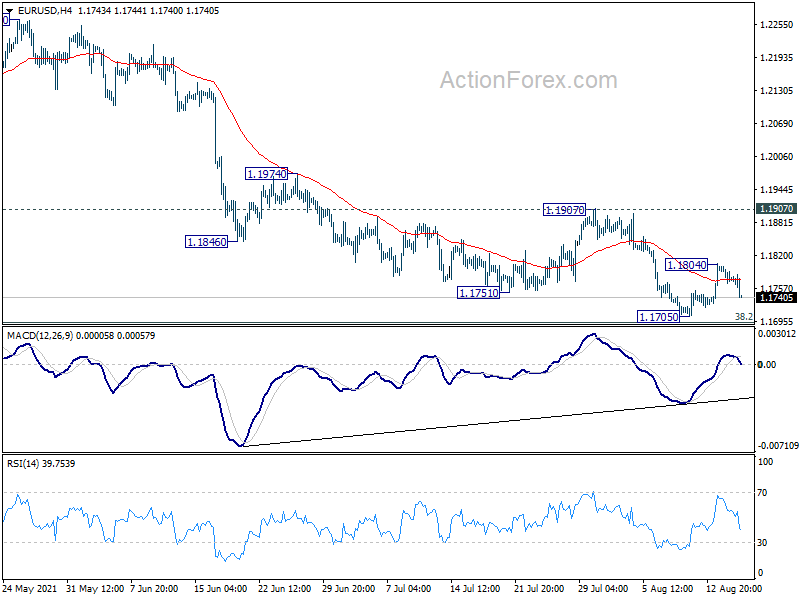

Intraday bias in EUR/USD is turned neutral with the current retreat. On the upside, above 1.1804 will resume the rebound from 1.1705 to 1.1907 near term structural resistance. On the downside, however, break of 1.1705 will resume larger fall to 1.1602/1703 key support zone again. We’d look for strong support from there to rebound, but sustained break will carry larger bearish implication.

{kind=link}

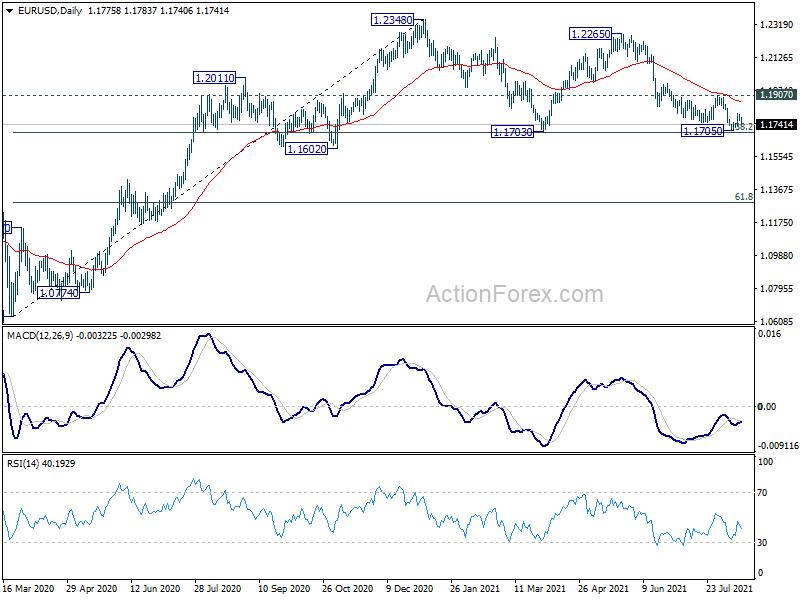

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally remains in favors long as 1.1602 support holds, to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). Reaction from 1.2555 should reveal underlying long term momentum in the pair. However sustained break of 1.1602 will argue that the rise from 1.0635 is over, and turn medium term outlook bearish again.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 04:30 | JPY | Tertiary Industry Index M/M Jun | 2.30% | 1.80% | -2.70% | |

| 06:00 | GBP | Claimant Count Change Jul | -7.8K | -114.8K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Jun | 4.70% | 4.80% | 4.80% | |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jun | 7.40% | 7.40% | 6.60% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jun | 8.80% | 8.70% | 7.30% | 7.40% |

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | 2.00% | 2.00% | 2.00% | |

| 09:00 | EUR | Eurozone Employment Change Q/Q Q2 P | 0.50% | -0.50% | -0.30% | |

| 12:15 | CAD | Housing Starts Jul | 272K | 275K | 282K | 281K |

| 12:30 | CAD | Foreign Securities Purchases (CAD) Jun | 19.63B | 20.79B | 20.81B | |

| 12:30 | USD | Retail Sales M/M Jul | -1.10% | -0.20% | 0.60% | 0.70% |

| 12:30 | USD | Retail Sales ex Autos M/M Jul | -0.40% | 0.10% | 1.30% | 1.60% |

| 13:15 | USD | Industrial Production M/M Jul | 0.40% | 0.40% | ||

| 13:15 | USD | Capacity Utilization Jul | 75.70% | 75.40% | ||

| 14:00 | USD | Business Inventories Jun | 0.80% | 0.50% | ||

| 14:00 | USD | NAHB Housing Market Index Aug | 80 | 80 |