US futures turn south after much weaker than expected ADP job data. Yen regains much growth as risk sentiment turn cautious again. Though, as for today, Kiwi and Aussie are still the strongest. Canadian Dollar is currently the worst performing as dragged down by weakness in oil price. Dollar is following as the next weakest and looks vulnerable, in particular against European majors and Yen.

Technically, Gold jumps sharply in early US session. Solid support is seen in 4 hour 55 EMA, which affirms near term bullishness. Focus is now on 1833.91 resistance. Break will resume the rebound from 1750.49 to 61.8% retracement of 1916.30 to 1750.39 at 1852.96. If happens, that should be accompanied by break of 1.1907 resistance in EUR/USD, to resume the rebound from 1.1751.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.23%. DAX is up 0.53%. CAC is up 0.31%. Germany 10-year yield is down -0.024 at -0.503. Earlier in Asia, Nikkei dropped -0.21%. Hong Kong HSI rose 0.88%. China Shanghai SSE rose 0.85%. Singapore Strait Times rose 1.07%. 10-year JGB yield dropped -0.0048 to 0.005.

US ADP employment grew just 330k, uneven progress slowed

US ADP employment grew just 330k in July, well below expectation of 680k. By company size, small businesses added 91k jobs, medium businesses 132k, large businesses 106k. By sector, goods-producing job grew 12k while service-providing jobs rose 318k.

“The labor market recovery continues to exhibit uneven progress, but progress nonetheless. July payroll data reports a marked slowdown from the second quarter pace in jobs growth,” said Nela Richardson, chief economist, ADP.

“For the fifth straight month the leisure and hospitality sector is the fastest growing industry, though gains have softened. The slowdown in the recovery has also impacted companies of all sizes. Bottlenecks in hiring continue to hold back stronger gains, particularly in light of new COVID-19 concerns tied to viral variants. These barriers should ebb in coming months, with stronger monthly gains ahead as a result.”

ECB Kazaks: Current forward guidance not tying out hands too much

ECB Governing Council member Martins Kazaks said, “given the uncertainty, given how much time is left, there is no need to decide on” what to do with the PEPP purchases after next March. He added, “we will discuss it, but at the moment it would still be premature.”

“It’s quite unlikely that we will come out in late March 2022 and say this is it, we’ve done our job and we terminate it,” Kazaks added. “We would like to warn the markets in advance — but only as much as it’s reasonably possible.”

Kazaks defended ECB’s new forward guidance, and said, it’s “a balanced view on how we may react when we see inflation approaching 2%.” “Is this tying our hands too much or too far into the future? I don’t think so,” He said. “If we find that this is not appropriate for the given economic situation then we can adjust our forward guidance.”

Eurozone retail sales rose 1.5% mom in Jun, EU up 1.2% mom

Eurozone retail sales rose 1.5% mom in June, below expectation of 1.9% mom. The volume of retail trade increased by 3.8% for automotive fuels and by 3.4% for non-food products, while it decreased by 1.5% for food, drinks and tobacco.

EU retail sales rose 1.2% mom. Among Member States for which data are available, the highest monthly increases in total retail trade were registered in Ireland (+9.4%), Germany and Latvia (both +4.2%) and Lithuania (+2.0). The largest decreases were observed in Malta (-3.0%), Austria (-2.7%) and Croatia (-2.6%).

Eurozone PMI composite finalized at record 60.2, GDP growth accelerates in Q3

Eurozone PMI Services was finalized at 59.8 in July, up from 58.3, highest since June 2006. PMI Composite was finalized at 60.2, up from 59.5, a new record high.

Chris Williamson, Chief Business Economist at IHS Markit said: “Europe’s service sector is springing back into life. Easing virus restrictions and further vaccination progress are boosting demand for a wide variety of activities….Alongside the sustained elevated growth recorded in the manufacturing sector, the impressive strength of the service sector’s expansion in July means the eurozone should see GDP growth accelerate in the third quarter.

“Worries about the Delta variant have become more widespread, however, subduing activity in some instances and raising concerns about the possibility of virus restrictions being tightened again…. Furthermore, up to now companies have generally seen little resistance from customers to higher prices, but this could change after the current rebound from lockdown restrictions has passed.”

Germany PMI Services was finalized at 61.8, up from June’s 57.5, surpassing previous record high set some 15 years ago. PMI Composite rose to record high of 62.4, up from 60.1.

France PMI Services was finalized at 56.8 in July, down from June’s 57.8. PMI Composite was finalized at 56.6, down from July’s 57.4.

UK PMI composite finalized at 59.2, re-acceleration of growth looks unlikely

UK PMI Services was finalized at 59.6 in July, down from June’s 62.4. PMI Composite dropped to 59.2, down from 62.2. Markit said there was weakest rise in business activity since March, but strongest input cost inflation in 25 years of data collection. Staff shortages constrained business capacity and recruitment.

Tim Moore, Economics Director at IHS Markit: “UK economy has slowed… More businesses are experiencing growth constraints from supply shortages of labour and materials, while on the demand side we’ve already seen the peak phase of pent up consumer spending… Any re-acceleration of growth in August looks unlikely.. as new orders increased at a much-reduced pace at the start of the third quarter… business expectations softened again.

Australia AiG construction dropped to 48.7 on outbreaks and restrictions

Australia AiG Performance of Construction Index dropped -6.8 to 48.7 in July, recording the first contraction since September 2020. Looking at some details, activity dropped -14.4 to 40.4. Employment rose 2.5 to 60.8. New orders dropped -6.6 to 49.5. Supplier deliveries dropped -7.6 to 43.3. Input prices dropped -1.1 to 97.2. Selling prices dropped -4.0 to 81.2. Average wages rose 6.7 to 77.1.

Ai Group Head of Policy, Peter Burn, said: “With Australia’s two largest states affected by COVID-19 outbreaks and associated restrictions, the construction industry slipped into contraction in July after a robust nine-month expansion. The negative national result masked continued growth outside of NSW and Victoria and further expansions in both house building and commercial construction…

“The outlook over the next couple of months will depend heavily on the paths of the COVID-19 outbreaks and the extent of restrictions.”

Australia retail sales dropped -1.8% mom in Jun, led by Victoria and NSW

Australia retail sales dropped -1.8% mom in June, unchanged from preliminary reading. Over the June quarter, sales rose 0.8% qoq.

ABS said: “States under longer periods of restrictions for the month saw a larger fall in their June turnover. The largest falls were in Victoria (-4.0 per cent), New South Wales (-2.0 per cent), and Queensland (-0.9 per cent). Other states and territories that saw stay-at-home orders for a least one day of the month included Western Australia (0.1 per cent), and the Northern Territory (-1.8 per cent).”

New Zealand unemployment rate dropped to 4.0%

New Zealand employment rose 1.0% in Q2, above expectation of 0.7%. It’s also the lowest since Q4 2019. Employment rate rose 0.5% to 67.6%. Unemployment rate dropped from 4.6% to 4.0%, much better than expectation of 4.5%. Labor force participation rate rose 0.1% to 70.5%. Labor cost index rose 0.9% qoq, above expectation of 0.7% qoq.

“The fall in unemployment is largely in line with other labour market indicators, including declining numbers of benefit recipients and increased job vacancies, and recent media reports of labour shortages and skills mismatches,” work, wealth, and wellbeing statistics senior manager Sean Broughton said.

China Caixin PMI services rose to 54.9, but still faces enormous downward pressure

China Caixin PMI Services rose from 50.3 to 54.9 in July, well above expectation of 54.9. PMI Composite rose from 50.6 to 53.1.

Wang Zhe, Senior Economist at Caixin Insight Group said: “As the July surveys of Caixin China PMIs were conducted after the epidemic in Guangdong province was brought under control, and before Covid-19 resurged in Jiangsu province, the services sector expanded rapidly, though the manufacturing sector was slightly weaker.

The resurgence of the epidemic in some parts of China at the end of July is expected to hurt August’s PMI readings. China’s official second-quarter economic figures were in line with expectations, but the Caixin China PMIs in July suggest that the economic recovery is not on sure footing. The economy still faces enormous downward pressure, and we need to ensure business owners remain confident.”

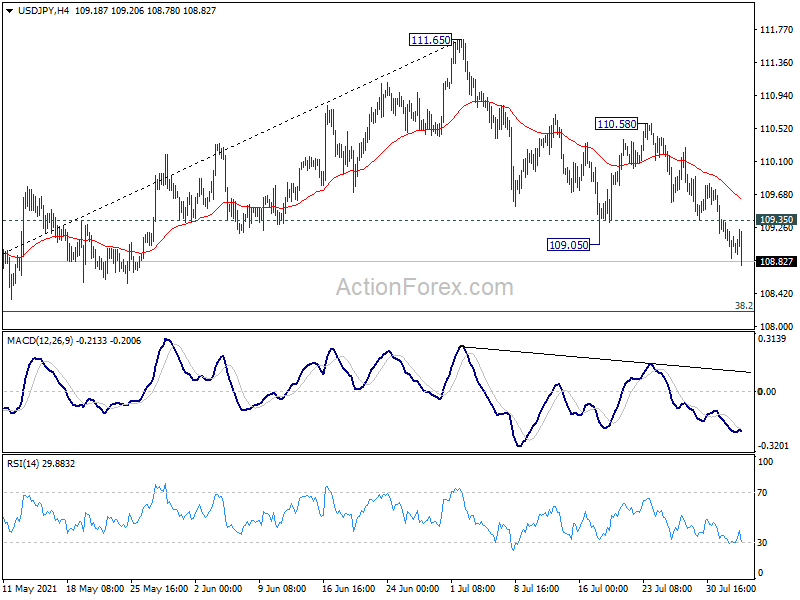

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.83; (P) 109.08; (R1) 109.29; More…

USD/JPY’s fall form 111.65 is still in progress and intraday bias stays on the downside for 38.2% retracement of 102.58 to 111.65 at 108.18. Sustained break there will target 61.8% retracement at 107.89 next. On the upside, above 109.35 minor resistance will turn intraday bias neutral first. But risk will remain on the downside as long as 110.58 resistance holds, in case of recovery.

{kind=link}

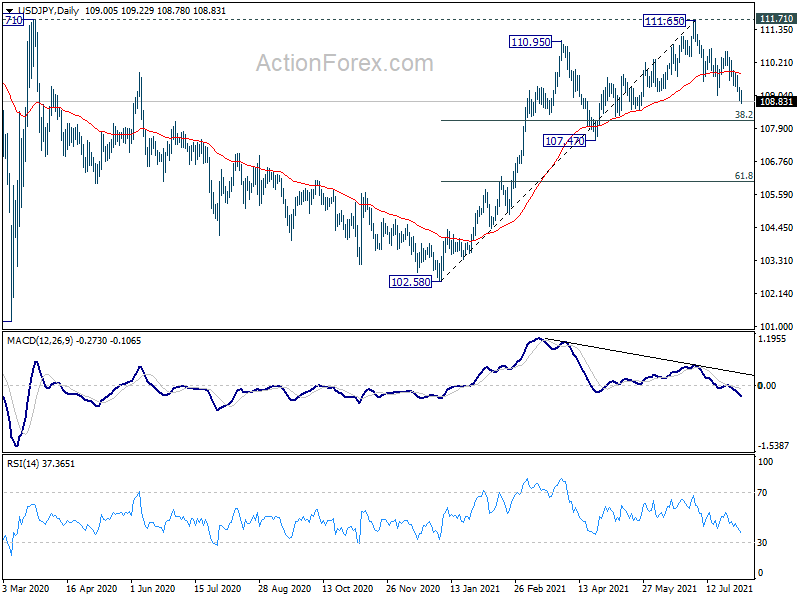

In the bigger picture, medium term outlook is staying neutral with 111.71 resistance intact. Firm break of 107.47 will argue that pattern from 101.18 has started another falling leg already. Deeper decline could be seen back to 101.18/102.58 support zone. For now, outlook won’t turn bullish as long as 111.71 resistance holds, even in case of strong rebound.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Construction Index Jul | 48.7 | 55.5 | ||

| 22:45 | NZD | Employment Change Q2 | 1.00% | 0.70% | 0.60% | |

| 22:45 | NZD | Unemployment Rate Q2 | 4.00% | 4.50% | 4.70% | 4.60% |

| 22:45 | NZD | Labour Cost Index Q/Q Q2 | 0.90% | 0.70% | 0.40% | |

| 01:30 | AUD | Retail Sales M/M Jun | -1.80% | -1.80% | -1.80% | |

| 01:45 | CNY | Caixin Services PMI Jul | 54.9 | 50.6 | 50.3 | |

| 07:45 | EUR | Italy Services PMI Jul | 58 | 58.2 | 56.7 | |

| 07:50 | EUR | France Services PMI Jul F | 56.8 | 57 | 57 | |

| 07:55 | EUR | Germany Services PMI Jul F | 61.8 | 62.2 | 62.2 | |

| 08:00 | EUR | Eurozone Services PMI Jul F | 59.8 | 60.4 | 60.4 | |

| 08:00 | EUR | Italy Retail Sales M/M Jun | 0.70% | 0.30% | 0.20% | -0.10% |

| 08:30 | GBP | Services PMI Jul F | 59.6 | 57.8 | 57.8 | |

| 09:00 | EUR | Eurozone Retail Sales M/M Jun | 1.50% | 1.90% | 4.60% | |

| 12:15 | USD | ADP Employment Change Jul | 330K | 680K | 692K | 680K |

| 12:30 | CAD | Building Permits M/M Jun | 6.90% | 6.00% | -14.80% | |

| 13:45 | USD | Services PMI Jul F | 59.8 | 59.8 | ||

| 14:00 | USD | ISM Services PMI Jul | 60.4 | 60.1 | ||

| 14:00 | USD | ISM Services Employment Jul | 49.3 | |||

| 14:30 | USD | Crude Oil Inventories | -3.2M | -4.1M |