The market opened the month with mildly positive sentiment, with major Asian indexes trading higher. But there is little reaction in the currency markets. Commodity currencies are generally soft for now, with slight losses in particular in Kiwi and Loonie. On the other hand, Dollar, Yen and Euro are trading mildly higher. Overall, however, there are no big moves yet as traders are awaiting a very busy week ahead, with two central bank meetings, and lots of heavy weight data releases.

Technically, one key question is that whether Dollar would solidify last week’s decline into general near term bearish reversal. In particular, EUR/USD needs to break through 1.1907 temporary top to resume the rebound from 1.1751 low first. Then, follow through buying is needed to push the pair through 1.2 handle decisively. We’ll if that would happen.

In Asia, at the time of writing, Nikkei is up 1.68%. Hong Kong HSI is up 1.26%. China Shanghai SSE is up 1.50%. Singapore Strait Times is down -0.27%. Japan 10-year JGB yield is up 0.0008 at 0.021.

Australia AiG manufacturing dropped to 60.8, further easing ahead

Australia AiG Performance of Manufacturing Index dropped -2.4 pts to 60.8 in July. Looking at some details, production rose 1.1 to 61.8. Employment rose 0.5 to 60.8. New orders dropped sharply by -8.1 to 62.5. Exports dropped -6.6 to 53.6. Input prices rose 5.8 to 84.6. Selling prices rose 1.1 to 64.7.

Ai Group Chief Executive Innes Willox said: “While COVID-19 outbreaks and associated restrictions in some states undoubtedly dampened the upswing in activity and shook confidence, the manufacturing sector recorded another strong month of expansion in July…. The slower pace of the manufacturing upswing in July and the slower pace of growth in new orders suggest further easing in the months ahead. A significant headwind for the sector is that Sydney’s toughest restrictions relate to local government areas where there is a concentration of manufacturing sites and the manufacturing workforce.”

Japan PMI manufacturing finalized at 53.0 in Jul, sharp rise in cost burdens

Japan PMI Manufacturing was finalized at 53.0 in July, up from June’s 52.4. Markit said output and new orders rose at faster rates. There were sharp rise in cost burdens amid supply chain disruption. Businesses reported softer optimism regarding future output.

Usamah Bhatti, Economist at IHS Markit, said: “The Japanese manufacturing sector continued to see an improvement in operating conditions… the pace of expansion quickened as firms recorded stronger growth in both output and new orders… supply chain disruption continued to impact activity within the sector, with firms recording the second greatest deterioration in lead times in over a decade. Material shortages and logistical disruption contributed to a rapid rise in average cost burdens, as input prices rose at the fastest pace since September 2008.

China Caixin PMI manufacturing dropped to 50.3 in Jul, recovery not yet solid

China Caixin PMI Manufacturing dropped to 50.3 in July, down from 51.3, below expectation of 51.0. Caixin said output growth slowed amid slight drop in new orders. Staffing levels were broadly unchanged while inflationary pressures eased.

Wang Zhe, Senior Economist at Caixin Insight Group said: “China’s official second-quarter economic figures were in line with expectations, but the Caixin China manufacturing PMI in July and relevant data suggested the recovery of the economy is not yet solid. The economy is still facing huge downward pressure, and we need to ensure entrepreneurs’ confidence.”

RBA and BoE to meet, US to release ISMs and NFP

Two central banks will meet this week. Given recent surge in delta variants and accompanying lockdowns, RBA is generally expected to reverse it’s tapering decision made just a month ago. For the very least, it’s likely that asset purchases would continue at a weekly pace of AUD 5B starting September. There are also speculations that RBA could indeed raise the pace to AUD 6B to show it’s flexibility and commitment.

BoE is widely expected to keep monetary policy unchanged, even though some officials have openly voiced concerns about inflation. The MPC would instead wait and see how the economy cope with fiscal tightening, as government support schemes come to an end. Nevertheless, new quarterly economic projections would still trigger some volatility in the Pound.

On the data front, US ISMs and non-farm payrolls will take center stage. Also watched include Canada employment, New Zealand employment, and China PMIs. Here are some highlights for the week:

- Monday: Australia AiG manufacturing, MI inflation gauge; Japan PMI manufacturing final, consumer confidence; China Caixin PMI manufacturing; Germany retail sales; Swiss CPI, retail sales, PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing final; US ISM manufacturing, construction spending.

- Tuesday: RBA rate decision; building approvals; Japan Tokyo CPI, monetary base; Swiss SECO consumer climate; Eurozone PPI; Canada PMI manufacturing; US factory orders.

- Wednesday: Australia retail sales, AiG construction; New Zealand employment; China Caixin PMI services; Eurozone PMI services final, retail sales; UK PMI services final; Canada building permits; US ADP employment; ISM services.

- Thursday: Australia trade balance; Germany factory orders; France industrial production; ECB monthly bulletin; UK PMI construction, BoE rate decision; Canada trade balance; US Challenger job cuts, jobless claims, trade balance.

- Friday: Australian AiG services; Japan household spending, average cash earnings, leading indicators; Germany industrial production; France trade balance; Swiss foreign currency reserves; Italy industrial production; Canada employment, Ivey PMI; US non-farm payrolls.

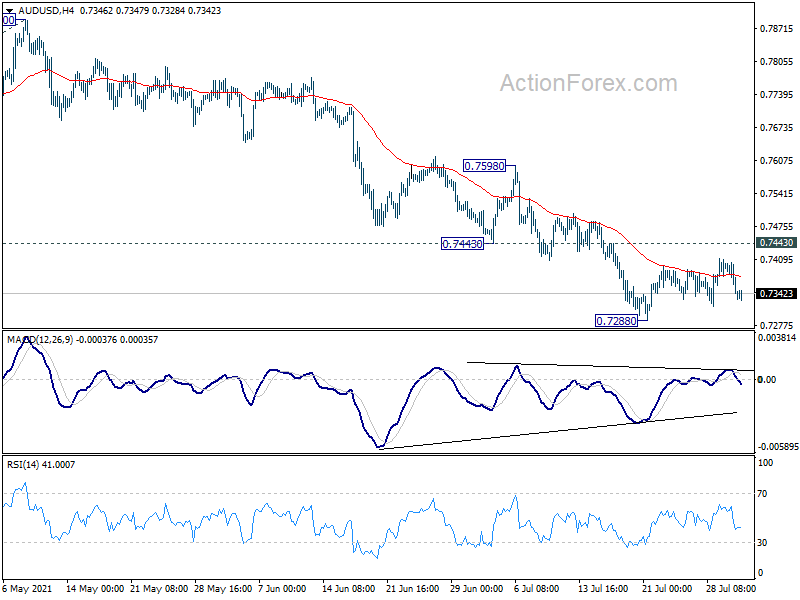

AUD/USD Daily Report

Daily Pivots: (S1) 0.7317; (P) 0.7361; (R1) 0.7391; More…

Intraday bias in AUD/USD remains neutral for the moment, as consolidation from 0.7288 is extending. Near term outlook stays bearish with 0.7443 support turned resistance intact, and further decline is in favor. On the downside, break of 0.7288 will resume the whole fall from 0.8006 and target 161.8% projection of 0.8006 to 0.7530 from 0.7890 at 0.7120 next. On the upside, break of 0.7443 will bring stronger rebound to 0.7530 support turned resistance instead.

{kind=link}

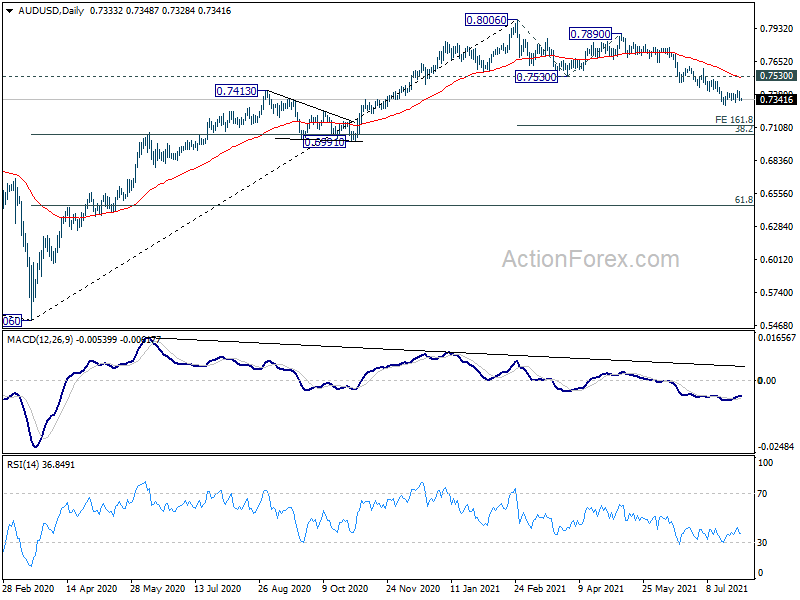

In the bigger picture, rise from 0.5506 medium term bottom could have completed at 0.8006, after failing 0.8135 key resistance. Correction from there could target 0.6991 cluster support (38.2% retracement of 0.5506 to 0.8006 at 0.7051). We’d look for strong support from there to bring rebound. However, sustained break of this level would argue that the whole medium term trend has indeed reversed.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Manufacturing Index Jul | 60.8 | 63.2 | ||

| 00:30 | JPY | Manufacturing PMI Jul F | 53 | 52.2 | 52.2 | |

| 01:00 | AUD | TD Securities Inflation M/M Jul | 0.50% | 0.40% | ||

| 01:45 | CNY | Caixin Manufacturing PMI Jul | 50.3 | 51 | 51.3 | |

| 05:00 | JPY | Consumer Confidence Index Jul | 36 | 37.4 | ||

| 06:00 | EUR | Germany Retail Sales M/M Jun | 2.00% | 4.20% | ||

| 06:30 | CHF | Real Retail Sales Y/Y Jun | 3.40% | 2.80% | ||

| 06:30 | CHF | CPI M/M Jul | -0.10% | 0.10% | ||

| 06:30 | CHF | CPI Y/Y Jul | 0.70% | 0.60% | ||

| 07:30 | CHF | SVME PMI Jul | 66 | 66.7 | ||

| 07:45 | EUR | Italy Manufacturing PMI Jul | 61.5 | 62.2 | ||

| 07:50 | EUR | France Manufacturing PMI Jul F | 58.1 | 58.1 | ||

| 07:55 | EUR | Germany Manufacturing PMI Jul F | 65.6 | 65.6 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jul F | 62.6 | 62.6 | ||

| 08:30 | GBP | Manufacturing PMI Jul F | 60.4 | 60.4 | ||

| 13:45 | USD | Manufacturing PMI Jul F | 63.1 | 63.1 | ||

| 14:00 | USD | ISM Manufacturing PMI Jul | 60.8 | 60.6 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jul | 93.2 | 92.1 | ||

| 14:00 | USD | ISM Manufacturing Employment Jul | 49.9 | |||

| 14:00 | USD | Construction Spending M/M Jun | 0.30% | -0.30% |