Forex news for North American traders on July 30, 2021.

The North American session started with concerns about the stock market and lingering fears above Covid. The earnings from Amazon after the close showed revenues less than expectations and revenue guidance going forward also lower. That came after Facebook the day before also scared the market with a less than rosy outlook. The NASDAQ was leading the way to the downside with the Core PCE data ahead.

That key inflation data (a favorite of the Fed) came in better than expected with YoY inflation at 3.5% versus 3.7% expected. The monthly increase also came in less than expectations at 0.4% vs 0.6% expected. Phew!

Is the inflation peak in? Will inflation levels start to move back down?

Ford Motor came out today and forecasts car prices to move back down after the chip shortage is fixed. That makes sense as most carmakers have been building, but have a backlog of unfinished cars without chips. One can foresee, there would be a glut of auto’s when the final chip piece is added.

This transient inflation sentiment continues to be one that Fed Chair Powell reiterated this week after the FOMC decision.

On the other end of the Fed spectrum is Fed’s Bullard (St. Louis Fed President and hawk) who got back on his soapbox after the end of the “quiet period”. He said today that he still expects 7% growth in 2021 and above trend growth for “quite some time”. He added that he expects inflation to remain above the Fed target this year and next year, making up for the years below the level, and proposes tapering both government and MBS purchases at the same time – ending the taper process in early 2022. Bullard is a voting member in 2022 and is one of the Fed members who sees hikes in 2022.

It is too early to see how the cards play, but next week, employment statistics will be the major event that may further sway the markets. The expectations are for a solid gain of 925K versus 850K last month.

Other economic data today showed University of Michigan consumer sentiment rising to 81.2 versus 80.8 expected (that was the preliminary as well). Expectations rose to 79.0 from 78.4 – accounted for the gain versus the preliminary estimate. The inflation gauges dipped down to 4.7% from 4.8% for 1 year, and 2.8% from 2.9% for 5-year expectations.

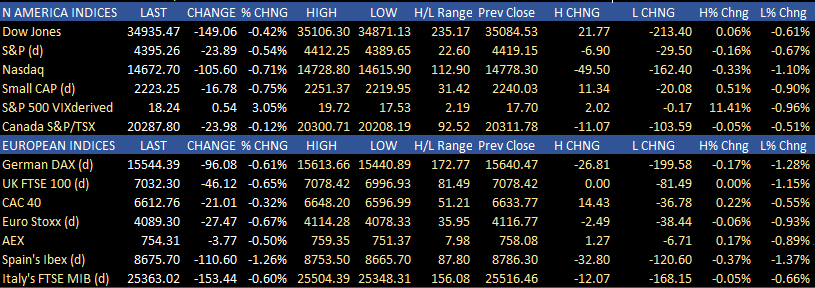

European shares also fell across the board with the UK FTSE 100 down -0.65% and Spain’s Ibex down -1.26%.

Below are the summaries of the changes for the major US and European indices:

In the US debt market today, the yields along the yield curve are closing lower, helped by the weaker then expected core PCE. The 10 year yield was down -4.3 basis points and closed just off the lows at 1.226%.

The USD did not take is clues from the lower rates or lower inflation (and move lower). Instead it moved higher in reaction to flight to safety flows. The CHF and the USD are ending the day higher (traditional flight to safety currencies) and are the strongest of the majors. The AUD and NZD are the weakest. That is also consistent with flight to safety/move out of risk flows. Below are the rankings of the major currencies and the % changes of the majors vs each other.

As mentioned next week the US and Canada employment statistics will be released on Friday. Before then ISM/PMI data will dominate the economic releases in Europe and the US.

Thank you all for your support. Have a terrific weekend and look forward to next week’s trading.