Dollar’s rally resumes after brief consolidation as focus now turns to non-farm payroll report. While some Fed officials might sound optimistic on their expectation on tapering later this year, it’s certain that Fed won’t move unless upbeat outlook is realized in economic data. Successive solid job growth for a few months is needed to give them the confidence that recovery is already on solid ground. As we’re approaching the end of the week, Dollar is currently the strongest, followed by Yen and Euro. Australian Dollar is worst performing, followed by New Zealand and Canadian.

Technically, Dollar’s momentum is so far solid against Euro, Sterling, Aussie and Swiss Franc. In particular, USD/JPY is now inside key resistance zone around 111/112. Sustained break there will carry larger bullish implications. USD/CAD is lagging behind others. We’d like to see USD/CAD breaking through 1.2485 resistance sooner rather than later to affirm the overall near term bluishness in the greenback.

In Asia, Nikkei closed up 0.27%. Hong Kong HSI is down -1.93%. China Shanghai SSE is down -1.93%. Singapore Strait Times is up 0.08%. Japan 10-year JGB yield is up 0.0079 at 0.048. Overnight, DOW rose 0.38%. S&P 500 rose 0.52%. NASDAQ rose 0.13%. 10-year yield rose 0.037 to 1.480.

IMF upgrades US GDP forecast to 7% this year

IMF raised US growth forecast for this year sharply higher from 4.6% to 7.0%. 2022 GDP growth forecast was also upgraded from 3.5% to 4.9%. Managing Director Kristalina Georgieva said the two fiscal stimulus packages will “add to near-term demand” and raises GDP by a cumulative 5.25% over 2022 to 2024.

IMF also said Fed would probably need to start raising interest rates in late 2022 or early 2023. Tapering could start in the first half of 2022. “Managing this transition — from providing reassurance that monetary policy will continue to deliver powerful support to the economy to preparing for an eventual scaling back of asset purchases and a withdrawal of monetary accommodation — will require deft communications under a potentially tight timeline,” IMF said.

Fed Harker wants to start tapering sooner than later

Philadelphia President Patrick Harker told WSJ that he’s “in the camp of starting the tapering process.” Asked if tapering should start this year, he said “yes”

“I would like to see tapering begin. I’d like to see it happen sooner rather than later,” he added. “I’d like to see it being a slow, methodical process.”

DOW could take on 35k again on solid NFP

US Non-Farm Payroll employment is a major focus today. Markets are expecting 675k job growth in June. Unemployment rate is expected to drop from 5.8% to 5.6%. Average hourly earnings are expected to grow 0.4% mom.

Looking at related data, ADP employment showed solid 692k growth in private sector jobs, centered in service-providing companies, across sizes. Four-week moving average of initial claims dropped from 428k to 393k. ISM manufacturing employment ticked back into contraction at 49.9. But right now, we don’t have ISM services employment yet, and that’s a key to how NFP would perform. There is prospect of some surprises.

S&P 500 and NASDAQ contained to made successive new record highs this week. But DOW is somewhat lagging behind. Nevertheless, developments are still promising that consolidation from 35091.56 has probably completed at 33271.93 already, after brief breach of medium term channel support.

Solid data in NFP could help lift DOW further towards 35091.56 high this week, setting the stage for an upside breakout in the coming days. That could also push Yen crosses generally higher. In particular, USD/JPY could follow and break through 111/112 key long term resistance zone decisively.

{kind=link}

Elsewhere

Japan monetary base rose 19.1% yoy in June, below expectation of 24.3% yoy. Eurozone will release PPI in European session. Canada will release building permits and trade balance. US will release NFP, trade balance and factory orders.

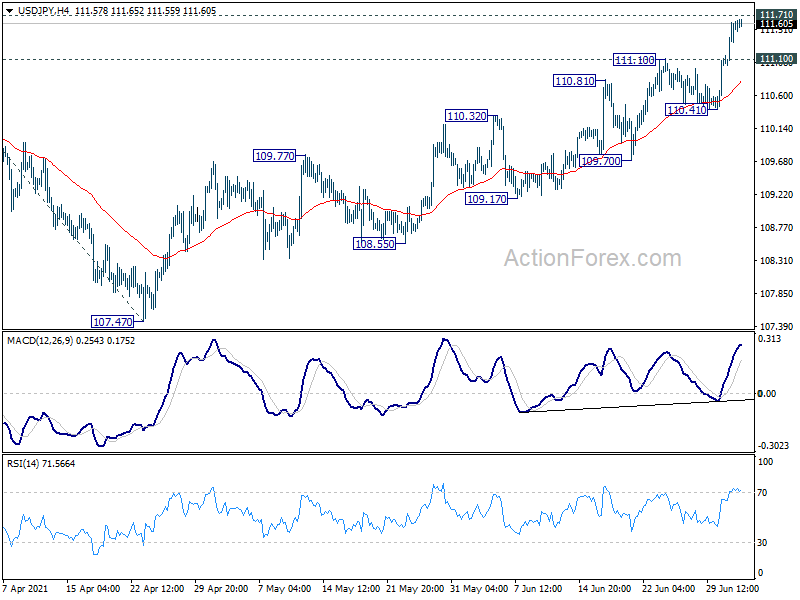

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.17; (P) 111.40; (R1) 111.78; More…

No change in USD/JPY’s outlook and intraday bias stays on the upside for 111.71 resistance. Sustained break there will carry larger bullish implication. Next target is 61.8% projection of 102.58 to 110.95 from 107.47 at 112.64. On the downside, below 111.10 minor support will turn intraday bias neutral first. But break of 110.41 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

{kind=link}

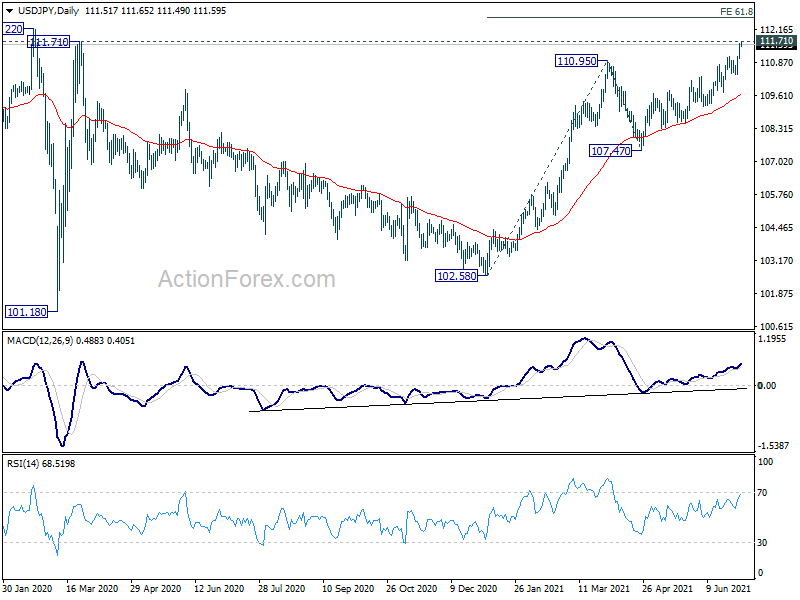

In the bigger picture, medium term outlook is staying neutral with 111.71 resistance intact. Though, as notable support was seen from 55 day EMA, rise from 102.58 is mildly in favor to extend higher. Decisive break of 111.71/112.22 resistance will suggest medium term bullish reversal. Rise from 101.18 could then target 118.65 resistance (Dec 2016) and above. However, sustained break of 55 day EMA would revive some medium term bearishness, and open up deep fall to 61.8% retracement of 102.58 to 110.95 at 105.77 and below.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Jun | 19.10% | 24.30% | 22.40% | |

| 9:00 | EUR | Eurozone PPI M/M May | 1.20% | 1.00% | ||

| 9:00 | EUR | Eurozone PPI Y/Y May | 9.50% | 7.60% | ||

| 12:30 | CAD | Building Permits M/M May | -0.50% | |||

| 12:30 | CAD | Trade Balance (CAD) May | 0.6B | |||

| 12:30 | USD | Nonfarm Payrolls Jun | 675K | 559K | ||

| 12:30 | USD | Unemployment Rate Jun | 5.60% | 5.80% | ||

| 12:30 | USD | Average Hourly Earnings M/M Jun | 0.40% | 0.50% | ||

| 12:30 | USD | Trade Balance (USD) May | -71.0B | -68.9B | ||

| 14:00 | USD | Factory Orders M/M May | 1.40% | -0.60% |