Dollar surges sharply against Yen today and maintains gain after better than expected job data. Though, the greenback is retreating mildly against other major currencies, as traders are probably lightening up their positions first ahead of tomorrow’s non-farm payrolls. Comments from ECB and BoE officials gave Euro and Sterling some support. But they’re not enough to trigger a notable rebound. Meanwhile, commodity currencies turned mixed. European stock indexes are trading in slight black but US futures are mixed.

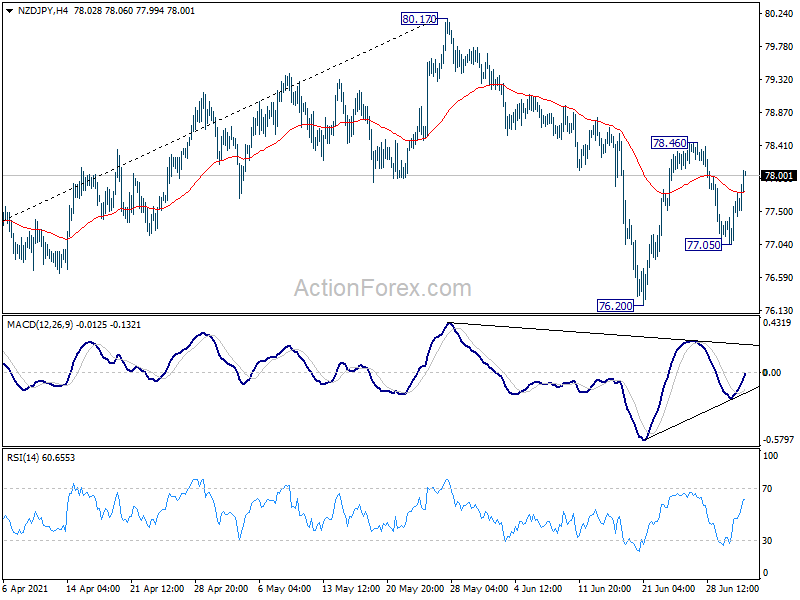

Technically, some focuses are turning back to Yen crosses. EUR/JPY would be eyeing 132.68 resistance against, and break could pave the way to retest 134.11 high. AUD/JPY also rebounds after hitting 82.79 and could be heading back to 84.24. Break will resume the rise from 82.11 for retesting 85.78 high. NZD/JPY looks even stronger and break of 78.46 will resume the rise from 76.20 for retesting 80.17 high.

{kind=link}

In Europe, at the time of writing, FTSE is up 0.70%. DAX is up 0.17%. CAC is up 0.44%. Germany 10-year yield is up 0.0023 at -0.202. Earlier in Asia, Nikkei dropped -0.29%. Hong Kong and China were on holiday. Singapore Strait Times dropped -0.20%. Japan 10-year JGB yield dropped -0.0192 to 0.040.

US initial jobless claims dropped to 364k, better than expected

US initial jobless claims dropped -51k to 364k in the week ending June 26, better than expectation of 382k. That’s the lowest level since March 14, 2020. Four-week moving average of initial claims dropped -6k to 392.75k, lowest since March 14, 2020.

Continuing claims rose 56k to 3469k in the week ending June 19. Four-week moving average of continuing claims dropped -75k to 3482k, lowest since March 21, 2020.

ECB Lagarde: Vaccination reduced probability of severe scenarios

ECB President Christine Lagarde said “the improved economic outlook on the back of rapid progress in vaccination campaigns has reduced the probability of severe scenarios.” But, “the nascent recovery still faces uncertainty also due to the spread of virus mutations.”

Meanwhile, the European Systemic Risk Board warned in a report that spillover effects from higher US bonds yields “could weigh on EU economic activity if the steepening of the yield curve were to perceptibly precede the economic recovery in the EU.”

“A perceptibly-stronger-than-currently-observed rise in European sovereign bond yields could have an adverse impact on debt dynamics, most notably in countries that already entered the COVID-19 crisis with an elevated debt burden,” the ESRB added.

Eurozone unemployment rate dropped to 7.9% in May, EU down to 7.3%

Eurozone unemployment rate dropped to 7.9% in May, down from 8.1%, better than expectation of 8.0%. EU unemployment dropped to 7.3%, down from 7.4%. It’s estimated that 15.278 million men and women in the EU, of whom 12.792 million in the euro area, were unemployed in May.

Eurozone PMI manufacturing finalized at record 63.4 in Jun

Eurozone PMI Manufacturing was finalized at 63.4 in June, up from May’s 63.1. The index also set fresh record for a fourth successive month. Markit said production increased sharply whilst job growth hit survey peak. Prices also rose at record rates as supply-side constraints persisted.

Looking at the member states, PMI manufacturing of the Netherlands dropped to 2-month low at 68.8. Austria hit record high at 67.0. Germany (65.1), Ireland (64.0), Italy (62.2), Spain (60.4) France (59.0) and Greece (58.6) all posted strong readings.

BoE Bailey: It’s important not to over-react to temporarily strong growth and inflation

BoE Governor Andrew Bailey urged in a speech that, “it is important not to over-react to temporarily strong growth and inflation, to ensure that the recovery is not undermined by a premature tightening in monetary conditions.”

Though, he admitted, “it is also important that we watch the outlook for inflation very carefully, which of course we do at all times, particularly for signs of more persistent pressure and for a move of medium term inflation expectations to a higher level.”

“And if we see those signs, we are prepared to respond with the tools of monetary policy,” he pledged.

UK PMI manufacturing finalized at 63.9 in June, record price increases

UK PMI Manufacturing was finalized at 63.9 in June, down from may’s record high of 65.6. Markit said supply-chain stresses led to record price increases. Robust growth of output, new orders and employment continued.

From Swiss, retail sales rose 2.8% yoy in May. CPI slowed to 0.1% mom, 0.6% yoy in June, SVME PMI dropped to 66.7, down from 69.9, missed expectation of 70.2.

Australia trade surplus widened to AUD 9.68B, AiG manufacturing rose to record 63.2

Australia goods and services exports rose 6% mom or AUD 2443m to AUD 42.23B in May. Goods and services rose 3% mom or AUD 919m to AUD 32.55B. Trade surplus widened to AUD 9.68B, up from AUD 8.16B, smaller than expectation of AUD 10.50B.

AiG Performance of Manufacturing Index rose to new record high at 63.2 in June, up from 61.8. That’s also the ninth consecutive month of rise. Looking at some more details, production dropped -3.8 to 60.7. Employment dropped -1.0 to 60.3. New orders jumped 5.7 to 70.6. Supplier deliveries rose 6.7 to 58.3. Exports rose 11.3 to 60.2. Input prices dropped -3.3 to 78.8. Selling prices rose 5.3 to 63.6.

Japan Tankan large manufacturing rose index to 14 in Q2, highest since 2018

Japan Tankan large manufacturing index rose to 14 in Q2, up from 5, missed expectation of 15. That’s the best level since 2018, and the fourth straight quarter of improvement. Large manufacturing output rose to 13, up from 4, below expectation of 18. Non-manufacturing index rose to 1, up from -1, below expectation of 3. Non-manufacturing outlook rose to 3, up from -1, missed expectation of 8. Large all industry capex rose 9.6%, above expectation of 7.2%.

PMI Manufacturing was finalized at 52.4 in June, down from May’s 53.0. Markit said output and new orders both rose at softest rates for five months. Input prices rose at fastest pace in over 10 years. Optimism was strongest on record.

China Caixin PMI manufacturing dropped to 51.3, gradually returned to normal

China Caixin PMI Manufacturing dropped to 51.3 in June, down from 52.0, below expectation of 51.8. Markit noted increase in output was softest for 15 months. Total new order growth slowed as export sales stagnated. Employment continued to inc rea sew while cost pressures eased.

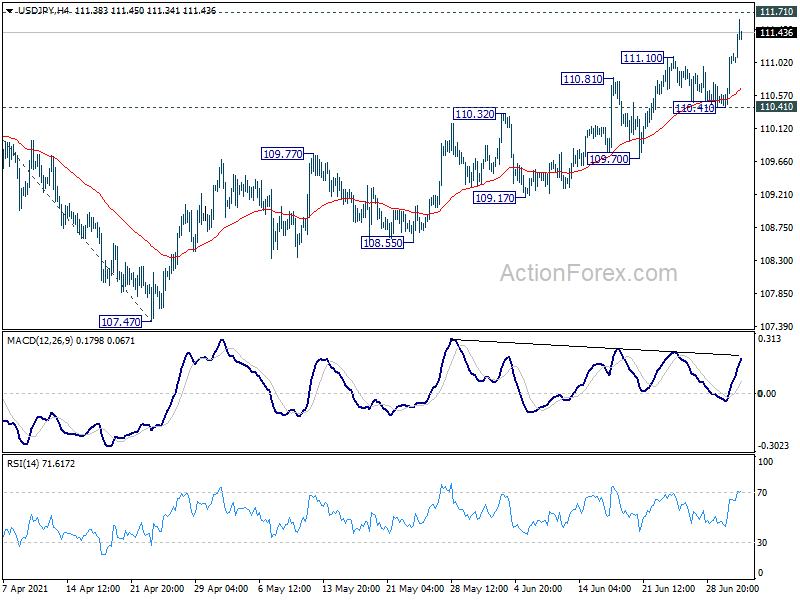

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.65; (P) 110.88; (R1) 111.35; More…

Intraday bias in USD/JPY remains on the upside for 111.71 resistance. Sustained break there will carry larger bullish implication. Next target is 61.8% projection of 102.58 to 110.95 from 107.47 at 112.64. On the downside, break of 110.41 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

{kind=link}

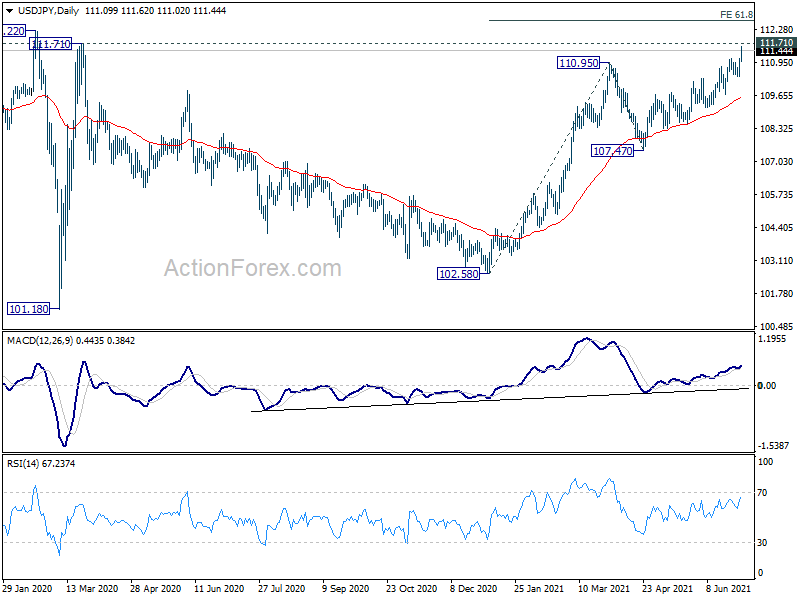

In the bigger picture, medium term outlook is staying neutral with 111.71 resistance intact. Though, as notable support was seen from 55 day EMA, rise from 102.58 is mildly in favor to extend higher. Decisive break of 111.71/112.22 resistance will suggest medium term bullish reversal. Rise from 101.18 could then target 118.65 resistance (Dec 2016) and above. However, sustained break of 55 day EMA would revive some medium term bearishness, and open up deep fall to 61.8% retracement of 102.58 to 110.95 at 105.77 and below.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Mfg Index Jun | 63.2 | 61.8 | ||

| 22:45 | NZD | Building Permits M/M May | -2.80% | 4.80% | 5.10% | |

| 23:50 | JPY | Tankan Large Manufacturing Index Q2 | 14 | 15 | 5 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q2 | 13 | 18 | 4 | |

| 23:50 | JPY | Tankan Non – Manufacturing Index Q2 | 1 | 3 | -1 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q2 | 3 | 8 | -1 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q2 | 9.60% | 7.20% | 3.00% | |

| 00:30 | JPY | Manufacturing PMI Jun F | 52.4 | 51.5 | 51.5 | |

| 01:30 | AUD | Trade Balance (AUD) May | 9.68B | 10.50B | 8.03B | 8.16B |

| 01:45 | CNY | Caixin Manufacturing PMI Jun | 51.3 | 51.8 | 52 | |

| 06:00 | EUR | Germany Retail Sales M/M May | 4.20% | 5.00% | -5.50% | |

| 06:30 | CHF | Real Retail Sales Y/Y May | 2.80% | 35.70% | 37.70% | |

| 06:30 | CHF | CPI M/M Jun | 0.10% | 0.20% | 0.30% | |

| 06:30 | CHF | CPI Y/Y Jun | 0.60% | 0.70% | 0.60% | |

| 07:30 | CHF | SVME PMI Jun | 66.7 | 70.2 | 69.9 | |

| 07:45 | EUR | Italy Manufacturing PMI Jun | 62.2 | 62.2 | 62.3 | |

| 07:50 | EUR | France Manufacturing PMI Jun F | 59 | 58.6 | 58.6 | |

| 07:55 | EUR | Germany Manufacturing PMI Jun F | 65.1 | 64.9 | 64.9 | |

| 08:00 | EUR | Italy Unemployment May | 10.50% | 10.70% | 10.70% | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun F | 63.4 | 63.1 | 63.1 | |

| 08:30 | GBP | Manufacturing PMI Jun | 63.9 | 64.2 | 64.2 | |

| 09:00 | EUR | Eurozone Unemployment Rate May | 7.90% | 8.00% | 8.00% | 8.10% |

| 11:30 | USD | Challenger Job Cuts Y/Y Jun | -88.00% | -93.80% | ||

| 12:30 | USD | Initial Jobless Claims (Jun 25) | 364K | 382K | 411K | 415K |

| 13:45 | USD | Manufacturing PMI Jun F | 62.6 | 62.6 | ||

| 14:00 | USD | ISM Manufacturing PMI Jun | 61.5 | 61.2 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jun | 89.8 | 88 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Jun | 50.9 | |||

| 14:00 | USD | Construction Spending M/M May | 0.40% | 0.20% | ||

| 14:30 | USD | Natural Gas Storage | 68B | 55B |