Dollar and Yen are currently the mildly strong ones this week so far. US stocks ended mixed as S&P 500 and NASDAQ made new record highs, but DOW refused to follow and closed lower. Asian markets are also generally in red. Australian and New Zealand Dollars are notably weaker today, while Sterling is trailing.

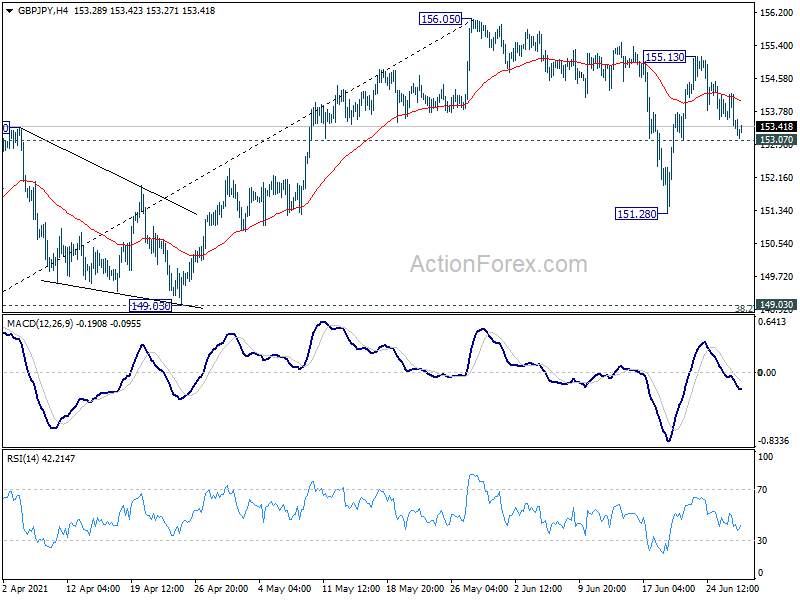

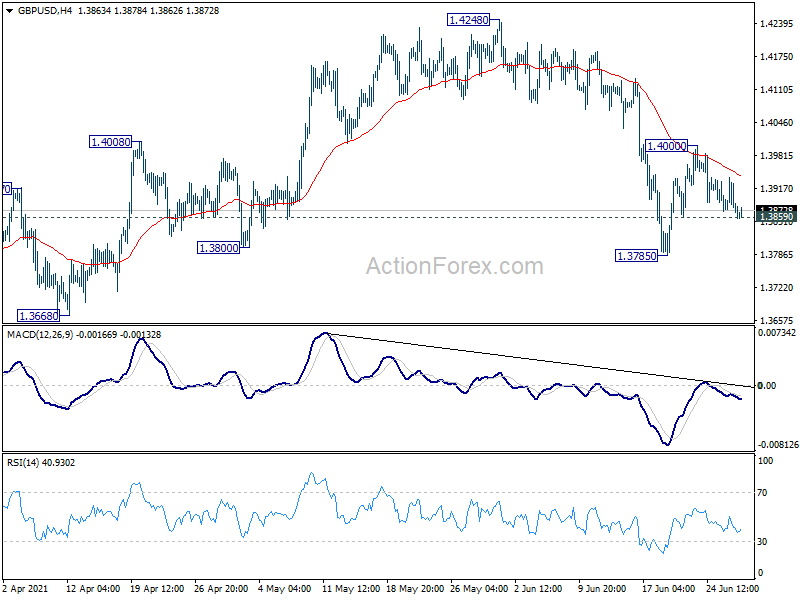

Technically, Sterling is looking vulnerable against Dollar and Yen for the moment. Break of 1.3859 minor support in GBP/USD and 153.07 minor support in GBP/JPY would argue that last week’s rebounds were completed. The pairs could then be heading back to 1.3785 and 151.28 support respectively. If that happens, we’d see if Euro would follow in EUR/USD and EUR/JPY too.

{kind=link}

In Asia, Nikkei closed down -0.85%. Hong Kong HSI is down -0.87%. China Shanghai SSE is down -0.87%. Singapore Strait Times is down -1.00%. Japan 10-year JGB yield is up 0.0002 at 0.061. Overnight, DOW dropped -0.44%. S&P 500 rose 0.23% to 4290.61, new record. NASDAQ rose 0.98% to 14500.50, also a record. 10-year yield dropped -0.058 to 1.478.

Fed Quarles: We’re not behind the curve on inflation

Fed Vice Chair Randal Quarles said that the current high inflation was transitory, due to supply chain imbalances and higher demand. He said, “if a year from now we were not to see inflation settling back down to something that’s closer to our 2% target… we have the tools at the Fed to then begin – as we traditionally would – to increase interest rates, to change our monetary policy in a way that would address that inflation.” He noted that “we’re not behind the curve”.

Separately, Richmond Fed President Thomas Barkin said, “it’s pretty clear to me we have had substantial further progress against our inflation goal”. “I’m pretty optimistic about the labor market. … If the labor market opens as I suggested it might, then I think we’re going to get there in relatively short order.”

“I kind of think let’s look at it next year and see what happens and if the numbers hit, great, if they don’t, we’ve got time because it will show there’s still more time for the economy to grow,” Barkin said.

RBNZ Orr: Policy settings expected to normalize over medium term

RBNZ Governor Adrian Orr said in a Statement of Intent that economic activity in New Zealand is “returning to its pre-COVID-19 levels”, supported by “ongoing favourable domestic health outcomes, and improving global demand and higher prices for New Zealand’s goods and exports”.

“A catch-up in consumer spending and construction activity, supported by substantial monetary and fiscal stimulus is underpinning employment growth,” he added.

“As long as COVID-19 is contained and the global and economic recovery is sustained, eventually economic policy settings can be expected to normalize over the medium term.”

On the data front

Japan unemployment rate rose to 3.0% in May, up from 2.8%, above expectation of 2.9%. Retail sales rose 8.2% yoy i n April, above expectation of 7.9% yoy.

UK mortgage approvals and M4 money supply, Eurozone economic sentiment, and Germany CPI flash will be released in European session. US will release house price index and consumer confidence.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3853; (P) 1.3896; (R1) 1.3922; More….

Intraday bias in GBP/USD remains neutral with focus on 1.3859 minor support. Break will indicate that fall from 1.4248 is likely resuming. Such decline is seen as the third leg of the consolidation pattern from 1.4240, and should target 1.3668 support and possibly below. On the upside, break of 1.4000 will turn bias back to the upside for retesting 1.4240/8 resistance zone instead.

{kind=link}

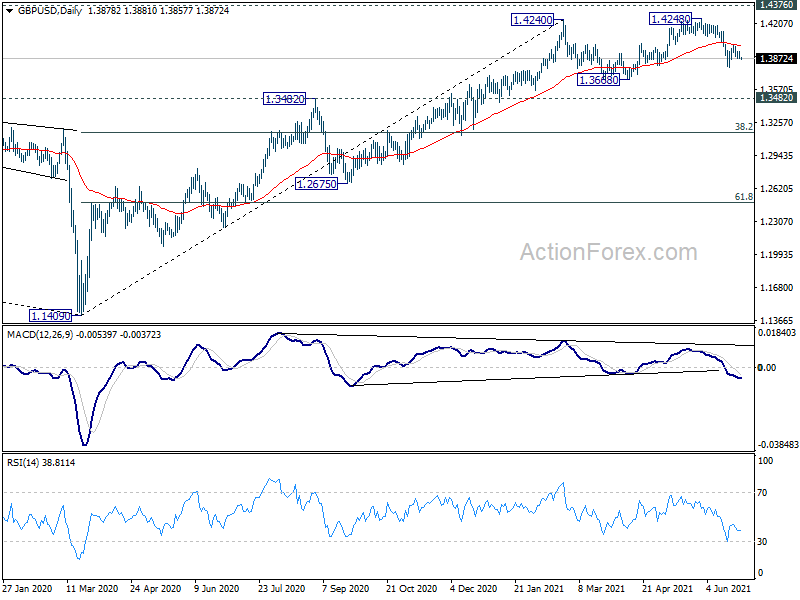

In the bigger picture, as long as 1.3482 resistance turned support holds, up trend from 1.1409 should still continue. Decisive break of 1.4376 resistance will carry larger bullish implications and target 38.2% retracement of 2.1161 (2007 high) to 1.1409 (2020 low) at 1.5134. However, firm break of 1.3482 support will argue that the rise from 1.1409 has completed and bring deeper fall to 1.2675 support and below.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Unemployment Rate May | 3.00% | 2.90% | 2.80% | |

| 23:50 | JPY | Retail Trade Y/Y Apr | 8.20% | 7.90% | 11.90% | |

| 8:30 | GBP | Mortgage Approvals May | 86K | 87K | ||

| 8:30 | GBP | M4 Money Supply M/M May | 0.20% | 0.10% | ||

| 9:00 | EUR | Eurozone Economic Sentiment Indicator Jun | 116.5 | 114.5 | ||

| 9:00 | EUR | Eurozone Services Sentiment Jun | 16 | 11.3 | ||

| 9:00 | EUR | Eurozone Industrial Confidence Jun | 13 | 11.5 | ||

| 9:00 | EUR | Eurozone Consumer Confidence Jun F | -3.3 | -3.3 | ||

| 9:00 | EUR | Eurozone Business Climate Jun | 1.5 | |||

| 12:00 | EUR | Germany CPI M/M Jun P | 0.40% | 0.50% | ||

| 12:00 | EUR | Germany CPI Y/Y Jun P | 2.30% | 2.50% | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Apr | 14.50% | 13.30% | ||

| 13:00 | USD | Housing Price Index M/M Apr | 1.80% | 1.40% | ||

| 14:00 | USD | Consumer Confidence Jun | 119.3 | 117.2 |