Dollar is maintaining much of this week’s gains as focus now turns to FOMC statement and economic projections. There is prospect of further rally for the greenback should some policymakers pull ahead their rate hike expectations. But the overall reactions would more depend on interaction with other markets like stocks and yield. As for the week so far, Yen is the worst performing one followed by Sterling and Aussie. Euro is the strongest, followed by Kiwi and then Dollar.

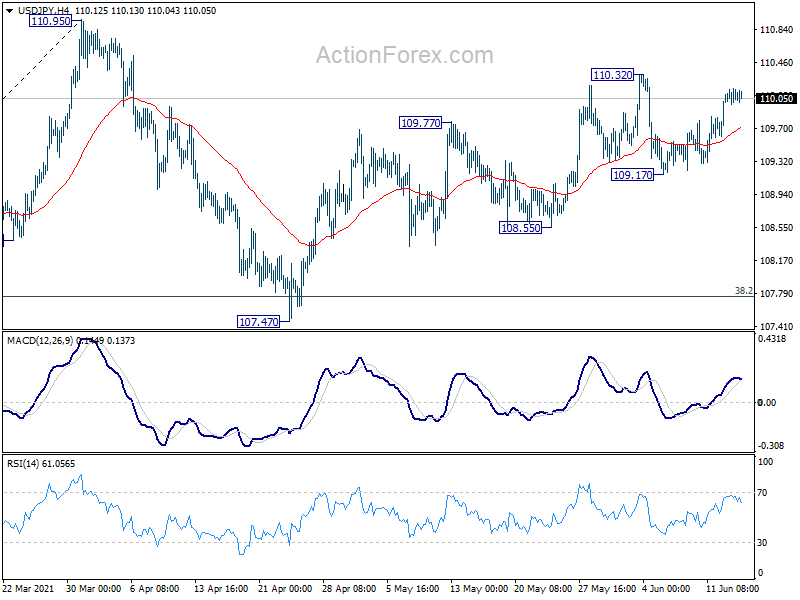

Technically, we’d maintain then some more upside breakouts in Dollar is needed to confirm its underlying strength. The levels include 1.1985 support in EUR/USD, 0.7644 support in AUD/USD, 0.9052 resistance in USD/CHF and 1.2201 resistance in USD/CAD. Or, at least, USD/JPY would have to break through 110.32 resistance to resume the whole rebound from 107.47.

In Asia, at the time of writing, Nikkei is down -0.39%. Hong Kong HSI is down -0.23%. China Shanghai SSE is down -0.77%. Singapore Strait Times is down -0.70%. Japan 10-year JGB yield is up 0.0054 at 0.054. Overnight, DOW dropped -0.27%. S&P 500 dropped -0.20%. NASDAQ dropped -0.71%. 10-year yield dropped -0.13%.

No tapering talks expected from Fed, some previews

Fed is widely expected to leave all monetary policy measures unchanged today. The Fed funds rate target will stay at 0-0.25%. The asset purchases program would also remain unchanged at USD 120B per month. It’s not expected to start talking about tapering yet, and could wait until the Jackson Hole Symposium to give a more solid indication.

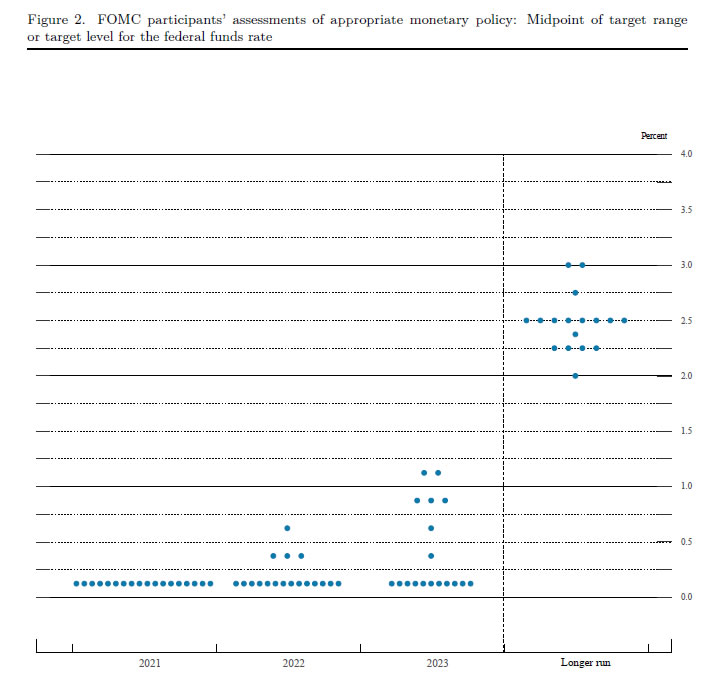

The main focuses would be on the updated economic projections, which would reflect Fed’s view on the path of inflation, as well as policy rates. Back in March, the dot plot indicated that the majority of policymakers forecast that the first hike would come in 2024. There were 4 members anticipating a rate hike next year and 7 by end -2023. While it might not be easy to push forward the forecast to 2023 (3 more members are needed), just 2 more could leave it balanced (9 vs 9) on whether it is 2023 or later.

{kind=link}

Some suggested previews here:

Japan exports rose 49.6% yoy in May, imports rose 27.9% yoy

Japan exports rose 49.6% yoy to JPY 6261B in May. That’s the largest rise since 1980. Imports rose 27.9% yoy to JPY 6448B. Trade surplus came in at JPY 187B, comparing with JPY 857B a year ago.

Looking at some details, exports to China rose 23.6% yoy to JPY 1393B. That was led by growth in chip production equipment, hybrid cars, and scrap copper. Exports to the US rose 87.9% yoy to JPY 1104B. Cars and auto parts led the growth to US-bound exports.

In seasonally adjusted terms, exports rose 0.0% mom to JPY 6860B. Imports rose 0.7% mom to JPY 6817B. Trade surplus narrowed to JPY 43B, down from JPY 84B.

Westpac: RBA unlikely to rate until 2025 to hike rates

Australia Westpac-MI leading index dropped eased from 2.86% to 1.47% in May. That’s the six-month annualized growth rate , which indicates the likely pace of economic activity relative to trend, three to nine months into the future. The index has moderated form just under 5% six months ago.

Westpac said that given the “improved pulse” of economic data as signalled by the leading index, “it seems unlikely that the Board would expect to have to wait until 2025 before it achieves the objectives necessary to justify the first cash rate increase since November 2010.” Also, it expects RBA to not extend the yield curve target from April 2024. RBA would decide to maintain the policy of AUD 5B of asset purchases per week, without setting a final target, to allow maximum flexibility.

Looking ahead

UK CPI, RPI and PPI will be released in European session. Canada will release CPI and wholesale sales later in the day. US will release housing starts and building permits, and import price index. But major focus is on FOMC.

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.98; (P) 110.08; (R1) 110.16; More…

USD/JPY is still bounded in range of 109.17/110.32 and intraday bias stays neutral at this point. On the upside, above 110.32 will resume the rise from 107.47. Intraday bias will be turned back to the upside for retesting 110.95 high. On the downside, below 109.17 will target 108.55 support, and then 107.47.

{kind=link}

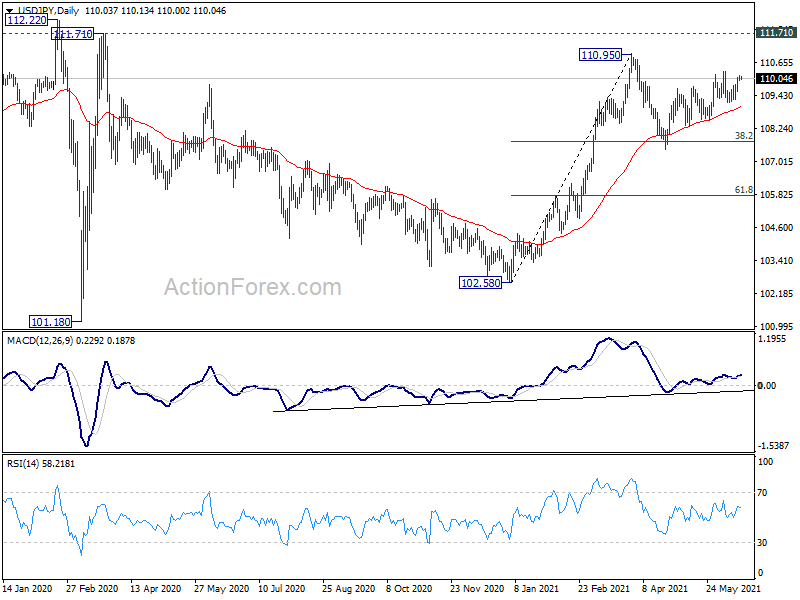

In the bigger picture, medium term outlook is staying neutral with 111.71 resistance intact. Though, as notable support was seen from 55 day EMA, rise from 102.58 is mildly in favor to extend higher. Decisive break of 111.71/112.22 resistance will suggest medium term bullish reversal. Rise from 101.18 could then target 118.65 resistance (Dec 2016) and above. However, sustained break of 55 day EMA would revive some medium term bearishness, and open up deep fall to 61.8% retracement of 102.58 to 110.95 at 105.77 and below.

{kind=link}

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Current Account (NZD) Q1 | -2.90B | -2.35B | -2.70B | -2.59B |

| 23:50 | JPY | Trade Balance (JPY) May | 0.04T | 0.24T | 0.07T | 0.08T |

| 23:50 | JPY | Machinery Orders M/M Apr | 0.60% | 2.70% | 3.70% | |

| 00:30 | AUD | Westpac Leading Index M/M May | -0.10% | 0.20% | ||

| 02:00 | CNY | Retail Sales Y/Y May | 14.00% | 17.70% | ||

| 02:00 | CNY | Industrial Production Y/Y May | 8.90% | 9.80% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y May | 16.80% | 19.90% | ||

| 06:00 | GBP | CPI M/M May | 0.60% | 0.60% | ||

| 06:00 | GBP | CPI Y/Y May | 1.80% | 1.50% | ||

| 06:00 | GBP | Core CPI Y/Y May | 1.30% | 1.30% | ||

| 06:00 | GBP | RPI M/M May | 0.20% | 1.40% | ||

| 06:00 | GBP | RPI Y/Y May | 2.40% | 2.90% | ||

| 06:00 | GBP | PPI – Input M/M May | 1.10% | 1.20% | ||

| 06:00 | GBP | PPI – Input Y/Y May | 9.00% | 9.90% | ||

| 06:00 | GBP | PPI – Output M/M May | 0.40% | 0.40% | ||

| 06:00 | GBP | PPI – Output Y/Y May | 4.50% | 3.90% | ||

| 06:00 | GBP | PPI Core Output M/M May | 0.20% | 0.50% | ||

| 06:00 | GBP | PPI Core Output Y/Y May | 2.90% | 2.50% | ||

| 12:30 | CAD | Wholesale Sales M/M Apr | -1.00% | 2.80% | ||

| 12:30 | CAD | CPI M/M May | 0.40% | 0.50% | ||

| 12:30 | CAD | CPI Y/Y May | 3.50% | 3.40% | ||

| 12:30 | CAD | CPI Common Y/Y May | 1.80% | 1.70% | ||

| 12:30 | CAD | CPI Median Y/Y May | 2.40% | 2.30% | ||

| 12:30 | CAD | CPI Trimmed Y/Y May | 2.40% | 2.30% | ||

| 12:30 | USD | Housing Starts May | 1.64M | 1.57M | ||

| 12:30 | USD | Building Permits May | 1.73M | 1.76M | ||

| 12:30 | USD | Import Price Index M/M May | 0.70% | 0.70% | ||

| 14:30 | USD | Crude Oil Inventories | -2.1M | -5.2M | ||

| 18:00 | USD | Fed Interest Rate Decision | 0.25% | 0.25% | ||

| 18:30 | USD | FOMC Press Conference |